Teen Driver Insurance Quotes: How to Shop Smart

Insuring a teen driver costs significantly more than insuring an adult-on average, adding a teen to a parent’s policy increases premiums by 50% to 100%. We at Eric L. Ash Insurance Agency know that finding affordable teen driver insurance quotes requires strategy, not just luck.

The good news is that rates aren’t fixed. Your choices about coverage, vehicle selection, and your teen’s driving habits directly impact what you’ll pay each month.

What Really Drives Teen Insurance Costs

Age matters far more than most parents realize, and the numbers are stark. An 18-year-old pays $599 per month for full coverage and will see that drop to roughly $390 by age 19 and $353 by age 20, according to insurance rate data. The jump is even sharper for 16-year-olds, who average around $709 monthly compared to 18-year-olds at $532. Insurers base these differences on actual crash statistics. Inexperience combined with age creates measurable risk, and that risk translates directly to your premium. Gender also plays a role where allowed by state law; 18-year-old males pay about $557 monthly for full coverage versus $508 for females, though some states including California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania ban gender-based pricing entirely.

The Vehicle Matters More Than You Think

The car your teen drives will either save you thousands or drain your wallet. A sports car or high-performance vehicle costs dramatically more to insure because crash data shows these vehicles experience higher loss rates. Choosing a safe, inexpensive sedan or compact SUV instead can cut insurance costs substantially. Insurers reward vehicles equipped with anti-lock brakes, airbags, and anti-theft devices with lower premiums. Location within your vehicle choice also counts-if your teen will be the primary driver, assign them to the cheapest family car rather than a newer or more expensive one. If they’re getting their own vehicle, prioritize affordability and safety features over anything else. Used vehicles in the two to five year old range typically offer the best balance of cost and safety ratings.

Driving Record Determines Future Rates

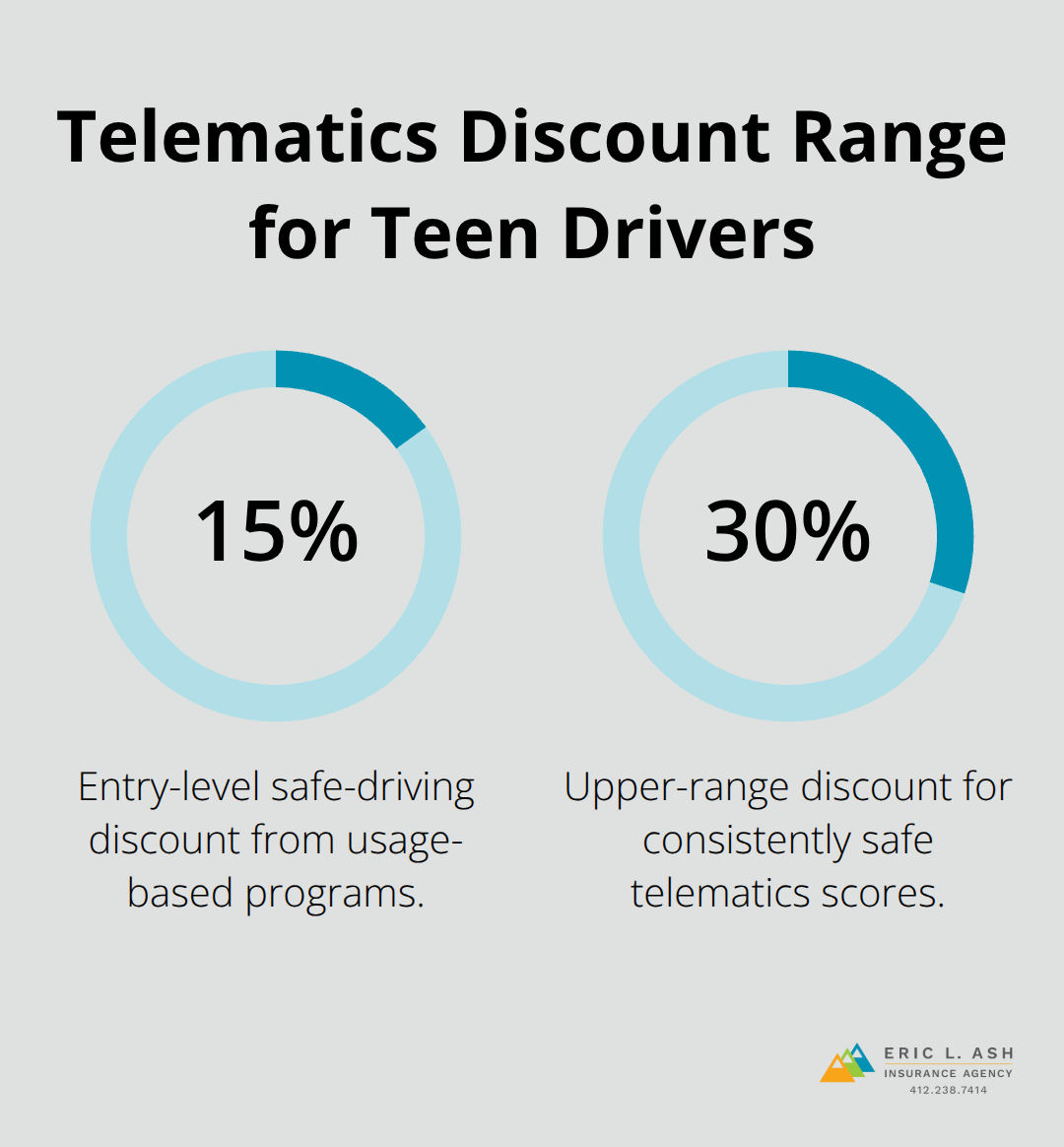

A clean driving record is your teen’s most valuable asset for keeping insurance affordable. One accident or moving violation can trigger surcharges that persist for years, even as your teen ages into lower-risk categories. However, some insurers offer Accident Forgiveness programs that can give you a cheaper auto insurance rate in the event of an accident by protecting you from another driver’s mistake. The harsh reality is that even with a perfect driving record, teen rates remain elevated for the first few years due to age and inexperience alone. This means your teen’s driving habits matter immediately-poor choices now lock in higher costs later. Usage-based or telematics programs that monitor actual driving behavior can reward safe habits with discounts ranging from 15% to 30%, giving your teen financial incentive to drive defensively from day one.

How Discounts and Programs Stack Up

Your teen’s grades can directly reduce what you pay each month. Good Student Discounts apply to students under 25 who maintain at least a B average, and these discounts often save hundreds annually. Defensive driving courses also yield monetary credits toward the policy premium and improve teen safety simultaneously. Telematics programs track real driving patterns and reward safe behavior, making them worth serious consideration when you shop quotes. These programs (which some insurers call safe-driver programs) create accountability while offering tangible savings for teens who drive responsibly. The combination of good grades, completed safety courses, and clean driving records can substantially lower your teen’s insurance costs compared to a teen with none of these advantages.

Understanding these cost drivers positions you to make smarter decisions when you compare quotes from multiple insurers-which is where the real savings opportunity lies.

Comparing Quotes Across Multiple Insurers

Why Quote Variation Matters

Quotes for the same teen driver vary by hundreds of dollars monthly depending on the insurer, and this variation makes shopping non-negotiable.

The problem is that the cheapest insurer in one state may be expensive in another-in some states, Erie ranks as the cheapest option while Nationwide ranks as the most expensive in those same states. This volatility means relying on a single quote leaves thousands of dollars on the table.

How to Gather Accurate Quotes

When you compare quotes from multiple carriers, list your teen on every application to receive accurate pricing and ensure proper coverage designation. A teen classified as an occasional driver rather than the primary driver will receive a lower quote, but misrepresenting their actual driving status can lead to claim denials later. Shop across national carriers like Geico, State Farm, and Progressive alongside regional options available in Pennsylvania. Comparing rates regularly typically yields better pricing, and the same principle applies to new teen drivers entering the market.

Standardizing Coverage for True Comparison

Two insurers quoting the same teen with different deductibles will show different premiums, making direct comparison impossible. A higher deductible lowers your monthly payment but increases what you pay out-of-pocket after an accident. If your teen causes $1,000 in damage with a $300 deductible, the insurer pays $700 while you cover $300. Most parents should avoid reducing coverage limits just to save money on monthly premiums. Full coverage including collision and comprehensive protection makes sense for financed or leased vehicles and for most vehicles worth more than $5,000. Minimum liability coverage alone may work only for older vehicles worth less than $5,000, though this leaves your family exposed to substantial liability risk if your teen causes a serious accident. When you compare quotes, standardize the coverage across all insurers so you evaluate price differences rather than coverage differences.

Evaluating Service Quality and Claims History

An insurer’s claims handling speed and fairness matter as much as price because you will want responsive service when your teen needs it most. Check each insurer’s complaint history through the Texas Department of Insurance Consumer Help Line at 800-252-3439 before committing. A low price paired with slow claims processing or poor customer service creates frustration when accidents happen. We at Eric L. Ash Insurance Agency compare protection and prices across multiple insurance companies on your behalf, delivering competitive rates and tailored coverage backed by responsive, local customer service that national companies cannot match.

The quotes you’ve gathered now reveal which insurers offer the best value for your teen’s specific situation. The next step involves identifying which discounts and programs apply to your teen’s profile-and how to stack them for maximum savings.

Practical Actions That Cut Teen Insurance Costs

Defensive Driving Courses Deliver Immediate Savings

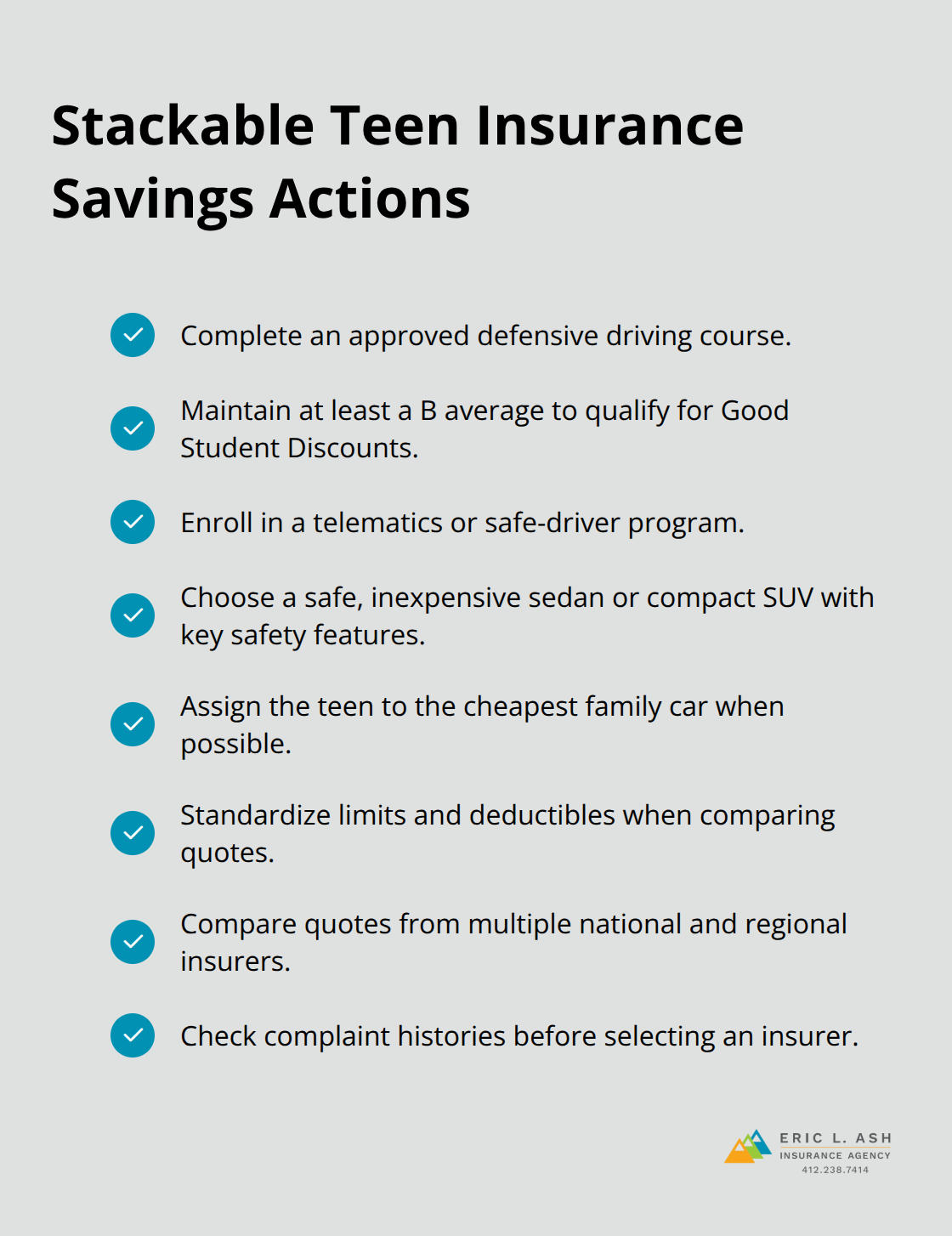

Defensive driving courses reduce your premium through concrete credits rather than vague promises. Many insurers offer monetary discounts specifically for approved driver education programs, and these courses teach teens skills that measurably reduce accident risk. Your teen completes the program, submits the certificate, and your insurer applies the discount to the next billing cycle. This isn’t theoretical savings-it’s an immediate rate reduction you can quantify before enrolling. Some insurers bundle this with telematics programs, so your teen receives rewards both for completing formal training and for demonstrating safe habits through real driving data.

Good Grades Translate to Lower Premiums

Good Student Discounts apply to students under 25 maintaining at least a B average, and these discounts often save hundreds annually according to insurance industry data. The logic is straightforward: students who maintain strong grades statistically show better judgment overall, including behind the wheel. This discount requires documentation, typically a report card or transcript, but the effort takes minutes. The discount amount varies by insurer, but savings of $300 to $600 per year are common for qualifying teens.

Vehicle Selection Determines Your Cost Ceiling

A safe, inexpensive sedan or compact SUV with anti-lock brakes, airbags, and anti-theft devices costs substantially less to insure than a sports car or luxury vehicle. If your teen is the primary driver, assign them to the cheapest family car rather than a newer model. If they’re getting their own vehicle, prioritize used models in the two to five year range from manufacturers with strong safety ratings-these typically cost less to insure than new sports cars while offering better protection than older vehicles. Anti-theft devices like GPS trackers or alarm systems trigger additional discounts at some carriers.

Stacking Discounts Multiplies Your Savings

The combination of these three actions-completing a defensive driving course, maintaining grades above the B threshold, and selecting a safe, affordable vehicle-can reduce your teen’s annual insurance cost compared to a teen without these advantages. Each discount stacks independently, meaning your teen qualifies for all three simultaneously rather than choosing between them. This multiplicative effect transforms individual savings into substantial annual reductions that compound year after year as your teen ages into lower-risk categories.

Final Thoughts

Shopping for teen driver insurance quotes requires comparing multiple carriers, understanding what drives costs, and stacking discounts strategically. An 18-year-old paying $599 monthly for full coverage can reduce that expense through vehicle selection, good grades, and defensive driving courses. Your teen’s age and driving record matter, but your choices about coverage and vehicle type matter equally.

Start by gathering quotes from at least three insurers and standardize coverage across all quotes so you compare apples to apples. Assign your teen to the cheapest family vehicle if possible, enroll them in a defensive driving course, and ensure they maintain grades above a B average to qualify for Good Student Discounts.

We at Eric L. Ash Insurance Agency shop multiple carriers on your behalf, comparing rates and coverage options tailored to your teen’s specific situation. Contact us today to get started with personalized teen driver insurance quotes and guidance that fits your family’s needs and budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.