Independent Insurance Agencies: Why Working With Local Brokers Helps You Save

Most Pennsylvania residents don’t realize they’re overpaying for insurance. When you buy directly from major insurers, you’re locked into their rates and coverage options-nothing more.

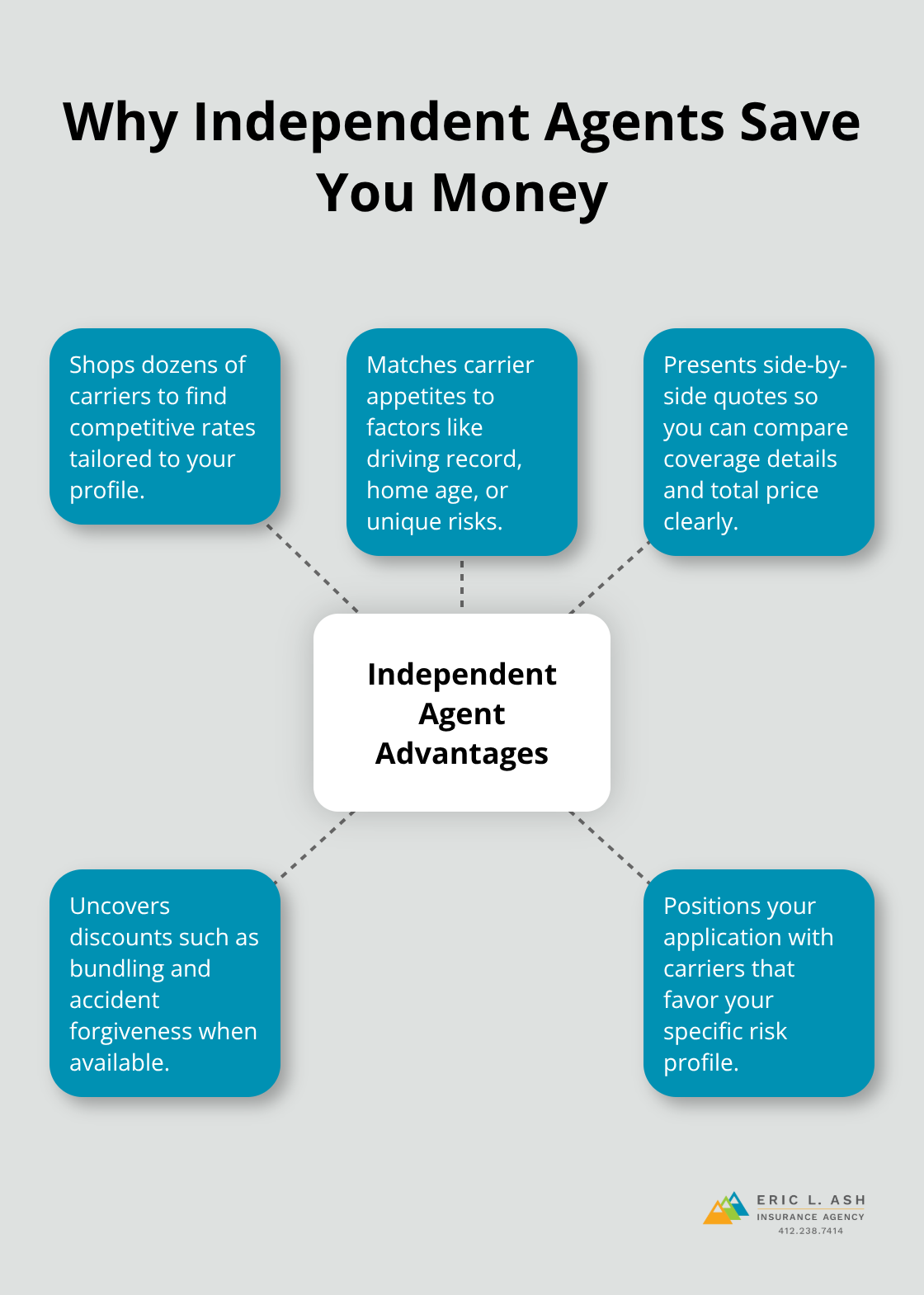

Independent insurance agencies work differently. We at Eric L. Ash Insurance Agency shop multiple carriers to find you better prices and customized coverage that actually fits your life. Local brokers know Pennsylvania’s specific requirements and handle your claims when problems arise.

How Independent Agencies Access Better Rates

When you call a direct insurer like Erie, State Farm, Farmers or Allstate, you get one company’s prices and one company’s coverage options. That’s it. Independent agencies work differently because we represent multiple insurers, not just one. This access to multiple insurers is the single biggest reason Pennsylvania residents save money with local brokers instead of going direct.

Pennsylvania Insurers Price Risk Differently

Pennsylvania insurers price risk differently. One carrier might charge you $1,200 a year for auto coverage while another charges $950 for nearly identical protection. When we shop your coverage across our network, we compare actual quotes from carriers that compete for your business. A Pennsylvania client working with a broker typically saves 10–30% on renewals just by moving to a better option when rates increase. That’s not theoretical savings; that’s what happens when someone actually compares prices instead of accepting the first quote.

Direct insurers have no incentive to offer you their best rate because you have nowhere else to go with them. We have every incentive to find you competitive pricing because you can choose any broker in Pennsylvania.

Coverage That Fits Your Actual Life

Direct insurers sell standard policies designed for average customers. Pennsylvania residents don’t fit into averages. Maybe you own a classic car, rent out a property, or run a small business from home. Standard policies either exclude these situations or charge you for coverage you don’t need. Independent agencies can access specialty carriers and custom policies that match your specific situation.

If you own a rental property in Pennsylvania, a local broker knows which carriers handle landlord policies efficiently and which ones create headaches during claims. If you’re a veteran, an agent understands the coverage gaps that matter to your household. This tailored approach costs less than buying a standard policy and then paying extra for riders and endorsements you shouldn’t need in the first place.

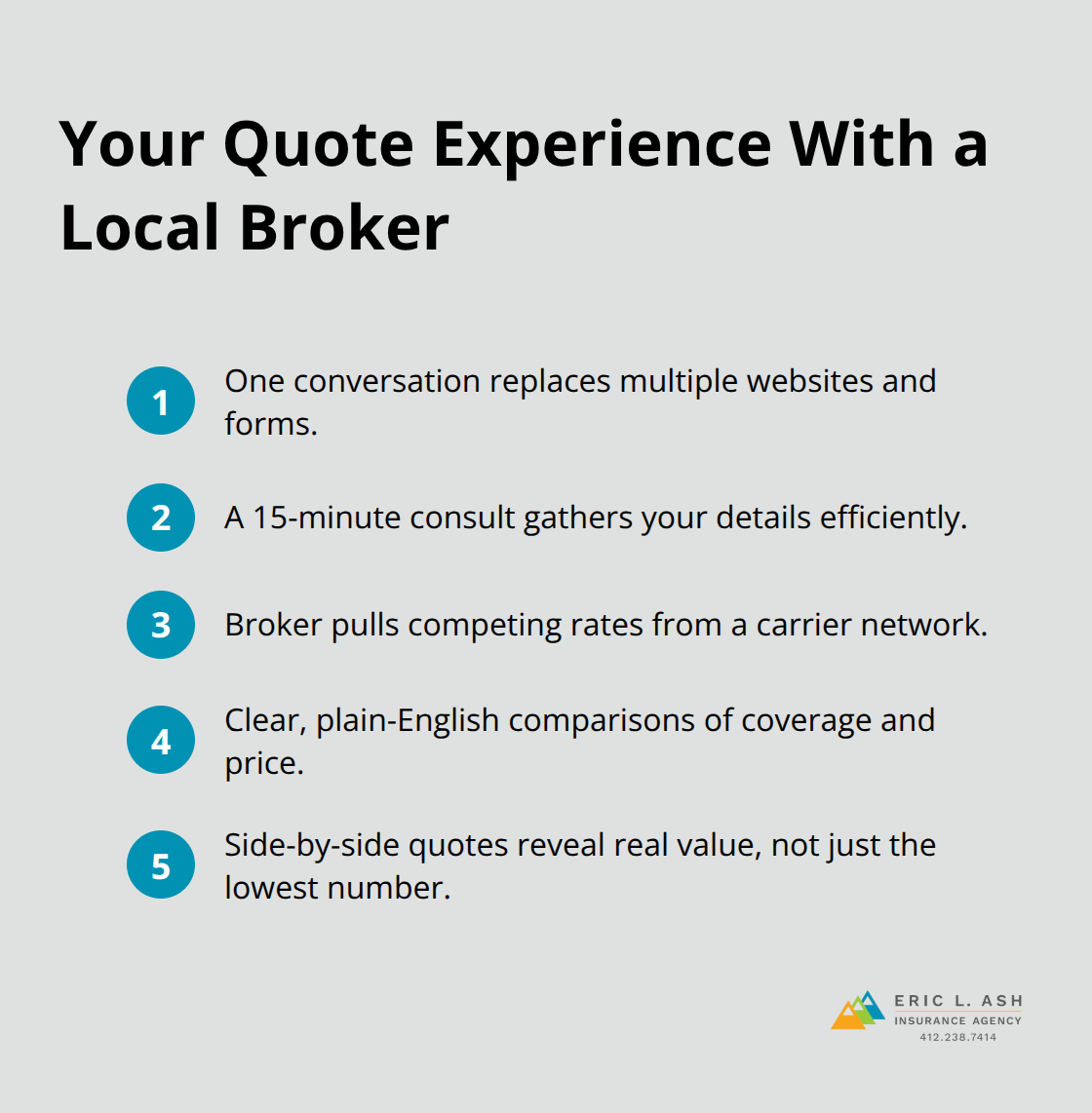

What You Actually See in the Quote Process

Getting quotes from direct insurers means visiting multiple websites, entering your information repeatedly, and waiting for callbacks. A local broker handles that work for you in one conversation. The process takes about 15 minutes for a consultation, then the broker pulls rates from the carrier network and presents you with plain-English explanations of what each option covers and costs. You see the actual differences between policies, not marketing language designed to confuse you.

Cheap premiums often hide weak coverage or higher deductibles. When you see quotes side-by-side, you make decisions based on real value, not just the lowest number. This transparency reveals what direct insurers don’t want you to know: their standard policies leave gaps that cost you money later. The next section shows how local brokers step in when claims happen and why that support matters more than you think.

Why Local Brokers Uncover Your Coverage Gaps Better Than You Do

A Pennsylvania homeowner calls their direct insurer to report a water damage claim from a burst pipe. The insurer denies it, citing coverage exclusions buried in policy documents. The homeowner never knew the exclusion existed because the insurer’s website didn’t highlight it during the online quote process. This happens constantly with direct insurers who sell one-size-fits-all policies without understanding your actual situation. Local brokers work the opposite way. We spend time learning about your home, your assets, your lifestyle, and your risk tolerance before recommending coverage. That conversation reveals gaps that generic policies miss entirely.

What Your Actual Situation Looks Like to a Local Broker

When you sit down with a broker, they ask questions that matter. Do you work from home? That changes your liability exposure and may require a home business rider. Do you have a trampoline or a pool? Standard homeowners policies often exclude or heavily restrict these. Do you have expensive jewelry, art, or collectibles? Standard policies cap coverage on these items far below their actual value. Are you renovating your kitchen or adding a deck? Construction costs in Pennsylvania have risen in recent years, meaning your replacement cost estimate might be dangerously outdated. A direct insurer doesn’t ask these questions because they’re not invested in whether you’re actually protected. A local broker asks because underinsurance creates real problems when claims happen. Annual policy reviews catch these gaps before they cost money. That’s not extra service; that’s the standard approach independent agencies use because your protection depends on it.

Pennsylvania-Specific Risks Most Homeowners Ignore

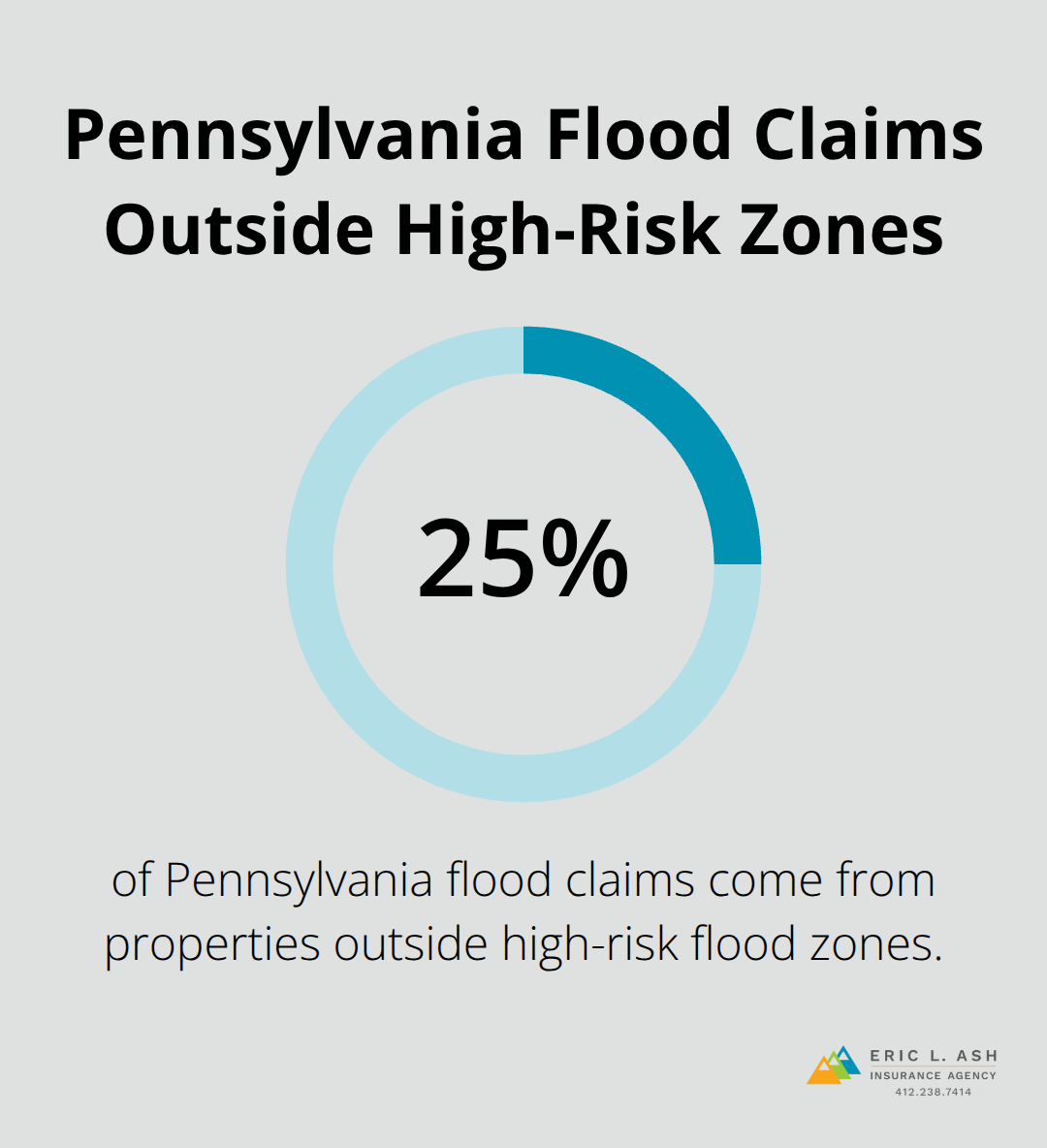

Pennsylvania’s geography creates specific insurance challenges that direct insurers treat as standard risk. Flood represents the biggest one. About 25% of Pennsylvania flood claims come from properties outside high-risk flood zones, meaning your home might face flood risk even if you’re not in an official flood area.

Direct insurers rarely mention this during the quote process. They simply don’t cover flood unless you purchase a separate policy, and many customers never know it exists. A local broker raises this immediately because we understand Pennsylvania’s water patterns and claims history. Flood insurance often costs less when you shop it properly, but only a broker with carrier relationships can find the right price. Winter claims present another Pennsylvania-specific issue. Ice dams, frozen pipes, and snow damage claims spike each year, and carriers adjust their underwriting accordingly. A broker familiar with Pennsylvania’s winter patterns knows which carriers handle these claims fairly and which ones create friction. Direct insurers have no incentive to explain these regional nuances because they sell nationally without local expertise.

How Claims Support Actually Works When You Need It

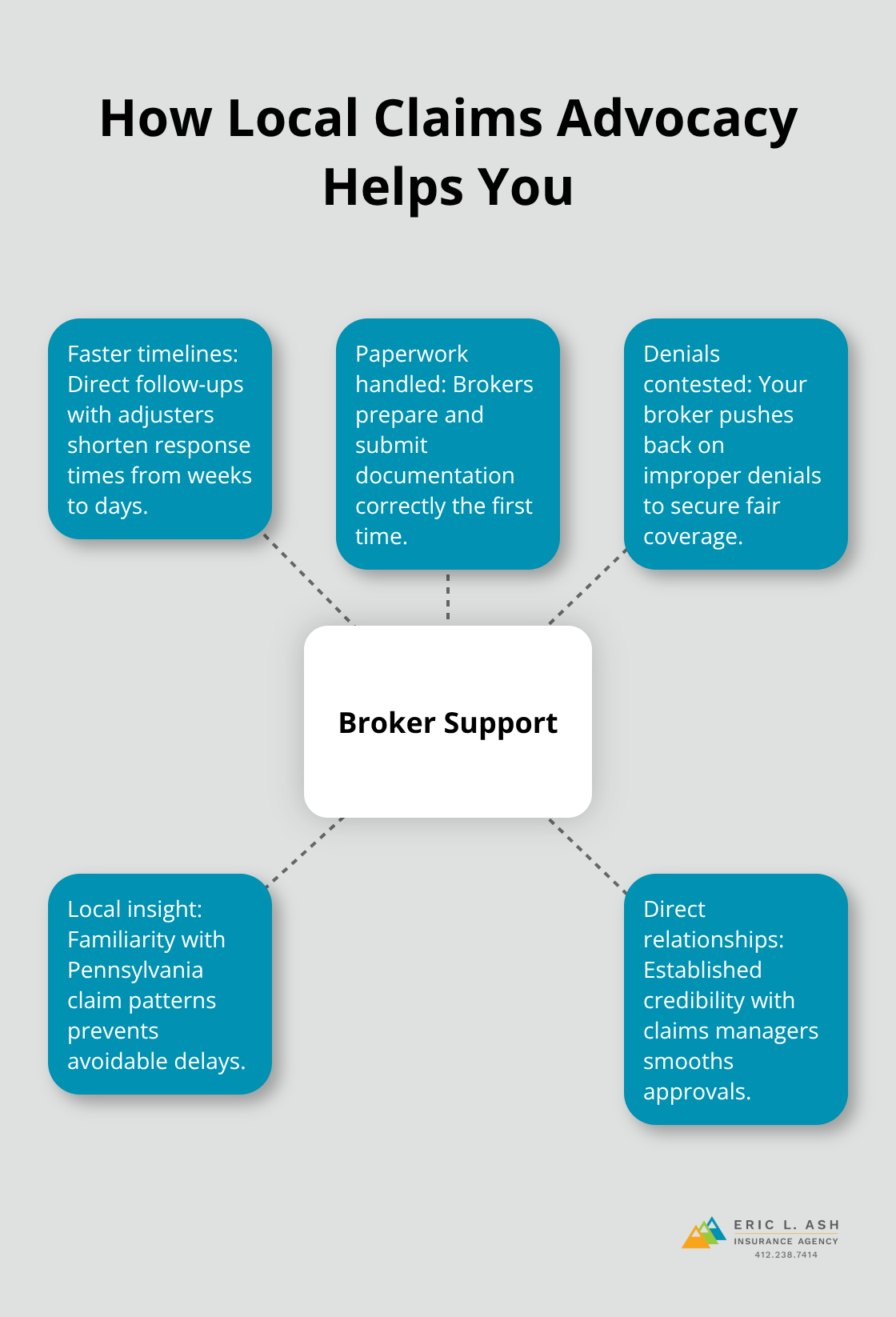

The moment you file a claim, the relationship with your insurance company either strengthens or reveals its weakness. Direct insurers handle claims through call centers and online portals. You submit documentation, wait for responses, and hope the process moves forward. Local brokers advocate on your behalf throughout the entire claims process. We file paperwork with carriers we’ve worked with for years, we follow up when responses lag, and we push back when an insurer denies something that should be covered. This advocacy matters most when the claim is complex or the insurer initially denies coverage. A broker who knows the adjuster and has established credibility resolves issues that customers stuck in a phone queue cannot. Pennsylvania’s weather creates frequent claims situations, and brokers who handle them regularly navigate carrier procedures faster than homeowners navigating the system alone. The difference isn’t theoretical; it’s the speed between filing a claim and getting paid, and the difference between acceptance and denial on borderline coverage questions. Direct insurers have no relationship with you beyond the transaction, so claims become purely transactional and often adversarial.

Why Direct Insurers Leave You Vulnerable

Direct insurers operate on volume and standardization. They price policies based on algorithms and broad risk categories, not on your specific circumstances. When you buy online, you answer a questionnaire designed to move you toward a sale, not to uncover your actual protection needs. The system works fine for customers who fit the standard profile. For everyone else-and that includes most Pennsylvania homeowners with unique situations, assets, or risks-direct insurers create dangerous gaps. A broker’s job is to identify those gaps and fill them before a claim exposes them. This is where the independent agency model delivers real value that goes far beyond finding a lower premium.

Why Direct Insurers Cost You More Than You Realize

Direct insurers like Erie, State Farm, Farmers or Allstate build their business model on standardized policies sold at scale. They don’t customize coverage because customization slows their sales process and complicates their underwriting. For Pennsylvania homeowners, this means you either accept their standard package or pay extra through riders and endorsements to patch gaps they should have addressed upfront. A homeowner with a finished basement that serves as a rental unit pays standard homeowners rates, then discovers the policy excludes rental income. Adding that coverage costs more than a broker would have charged for the right policy from the start.

Why Direct Insurers Never Shop Rates for You

Direct insurers have no incentive to offer competitive pricing because you have nowhere else to go with them. When you call Allstate, you receive Allstate’s price, not a comparison across carriers that compete for your business. One Pennsylvania homeowner paid $1,450 annually through a direct insurer for auto coverage. When we at Eric L. Ash Insurance Agency shopped that same driver across our carrier network, we found identical coverage for $980 a year through a different insurer. That $470 annual difference compounds to thousands over a decade. Direct insurers count on customers never knowing what they could have paid elsewhere. They also count on the friction of shopping multiple websites to prevent you from discovering better options.

How Direct Insurers Leave You Underinsured

Direct insurers don’t review your replacement cost estimates unless you specifically ask them to. Construction costs in Pennsylvania have risen significantly in recent years, and many homeowners still rely on outdated replacement cost estimates from their previous policies. This leaves thousands of dollars in underinsurance exposure that direct insurers never mention. About 25% of Pennsylvania flood claims occur outside official flood zones, yet direct insurers treat flood as optional coverage without emphasizing its importance during the quote process. They mention it exists, but they don’t explain why it matters for your specific property. A local broker raises this immediately because we understand Pennsylvania’s geography and claims history.

Why Claims Processing Delays Cost You Real Money

The claims experience with direct insurers reveals their true weakness most clearly. When you file a claim through an online portal or call center, you become one ticket in a queue managed by people who’ve never spoken to you before and have no relationship with the carrier’s underwriting or claims teams. Pennsylvania residents filing winter damage claims or flood claims often experience delays because call center staff follow scripts rather than understanding regional claim patterns or carrier procedures. Direct insurers process claims through centralized systems that may take weeks to respond to documentation requests. A local broker with established relationships can often resolve claims in days rather than weeks because we follow up directly with adjusters and push for faster responses. When your home floods or your car is totaled, that speed difference between a direct insurer’s call center and a broker’s direct carrier relationships determines how quickly you receive payment and move forward with repairs or replacement. A broker advocates directly with adjusters and claims managers, pushing back on denials and accelerating approvals in ways that phone queue customers cannot achieve.

Final Thoughts

Pennsylvania residents who work with independent insurance agencies save 10–30% on renewals by accessing multiple carriers instead of accepting a single insurer’s rates. That savings compounds over years and decades. Beyond price, local brokers catch coverage gaps that direct insurers never mention, handle claims faster through established carrier relationships, and adjust your protection as your life changes.

Independent insurance agencies deliver value that extends far beyond finding a lower premium. We at Eric L. Ash Insurance Agency work with dozens of carriers to match your coverage to your actual needs, not to a generic template. Whether you own a classic car, rent out a property, or simply want protection that reflects your Pennsylvania home’s true replacement cost, local brokers provide the expertise and relationships that direct insurers cannot match.

Contact Eric L. Ash Insurance Agency to see how local expertise and multiple carrier options can save you money while delivering the protection you actually need.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.