Rental Property Insurance PA: What Every Landlord Should Know

Owning rental property in Pennsylvania comes with real financial responsibility. Many landlords discover they’re underprotected only after something goes wrong, which is why rental property insurance PA isn’t optional-it’s essential.

We at Eric L. Ash Insurance Agency help landlords understand what coverage actually protects their investment and income. This guide walks you through the policies you need and the mistakes to avoid.

What Landlord Insurance Actually Covers

Standard homeowners insurance explicitly excludes rental income and tenant-related liability, which means your homeowners policy becomes worthless the moment a tenant moves in. A homeowners policy protects owner-occupied properties where you live; it assumes you maintain the property and control who enters it. The moment you rent out that property, the underwriting assumptions change completely. Landlord insurance covers property damage, liability and loss of rent coverage to account for tenants, guest injuries, and income loss when the property becomes uninhabitable.

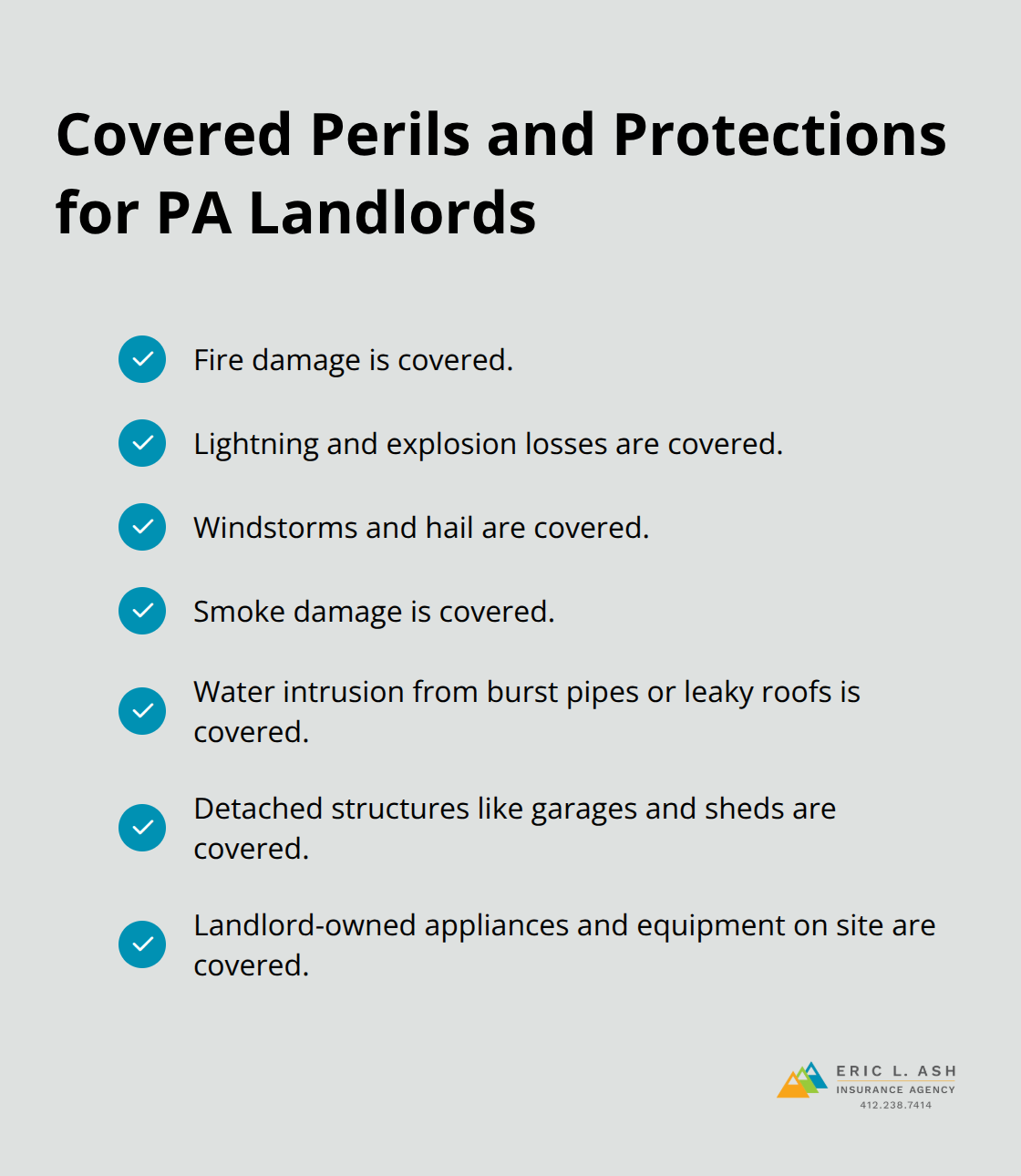

In Pennsylvania, where average rents in Philadelphia neighborhoods exceed $2,000 monthly for one to two bedroom units and Pittsburgh averages around $1,400, losing even one month of rental income creates a serious cash flow problem. Landlord policies cover fire, lightning, explosions, windstorms, hail, smoke, and water intrusion from burst pipes or leaky roofs-perils that matter in Pennsylvania’s climate.

They also cover detached structures like garages and sheds, plus landlord-owned appliances and equipment on site.

How Liability Coverage Protects You from Tenant and Guest Claims

General liability coverage in a landlord policy protects you when a tenant or their guest gets injured on your property and sues. Pennsylvania negligence law makes landlords responsible for unsafe conditions, so liability coverage handles medical costs, legal fees, and settlements when claims arise. Without this protection, a single injury claim can drain your savings and force you to sell the property to cover the judgment.

Why Loss of Rent Coverage Matters More Than You Think

Loss of rental income coverage reimburses you when a covered event-a fire, hail damage, or water intrusion-makes the property uninhabitable and forces tenants to leave temporarily or permanently. Without this coverage, you absorb the full financial hit while still paying your mortgage, property taxes, and maintenance costs. If your property sits empty for three months after a covered loss, that’s three months of zero income stacked against ongoing expenses.

Loss of rent coverage is included in comprehensive landlord policies but isn’t automatic on all plans, so you must verify it’s included when you quote. This coverage exists specifically because rental properties generate income that homeowners policies never account for. Many Pennsylvania landlords skip this coverage to save $50 to $100 annually on premiums, then face tens of thousands in lost rent after a single incident. That’s a false economy.

What Happens When You Underestimate Your Coverage Needs

The gap between what landlords think they’re covered for and what their policies actually cover creates serious problems. Many landlords assume their standard homeowners policy extends to rental properties or that basic liability limits suffice for their situation. These assumptions lead to coverage gaps that surface only after a loss occurs, when it’s too late to add protection.

Understanding these coverage types sets the foundation for recognizing which mistakes landlords make most often-and how to avoid them.

Types of Coverage Every Pennsylvania Landlord Should Have

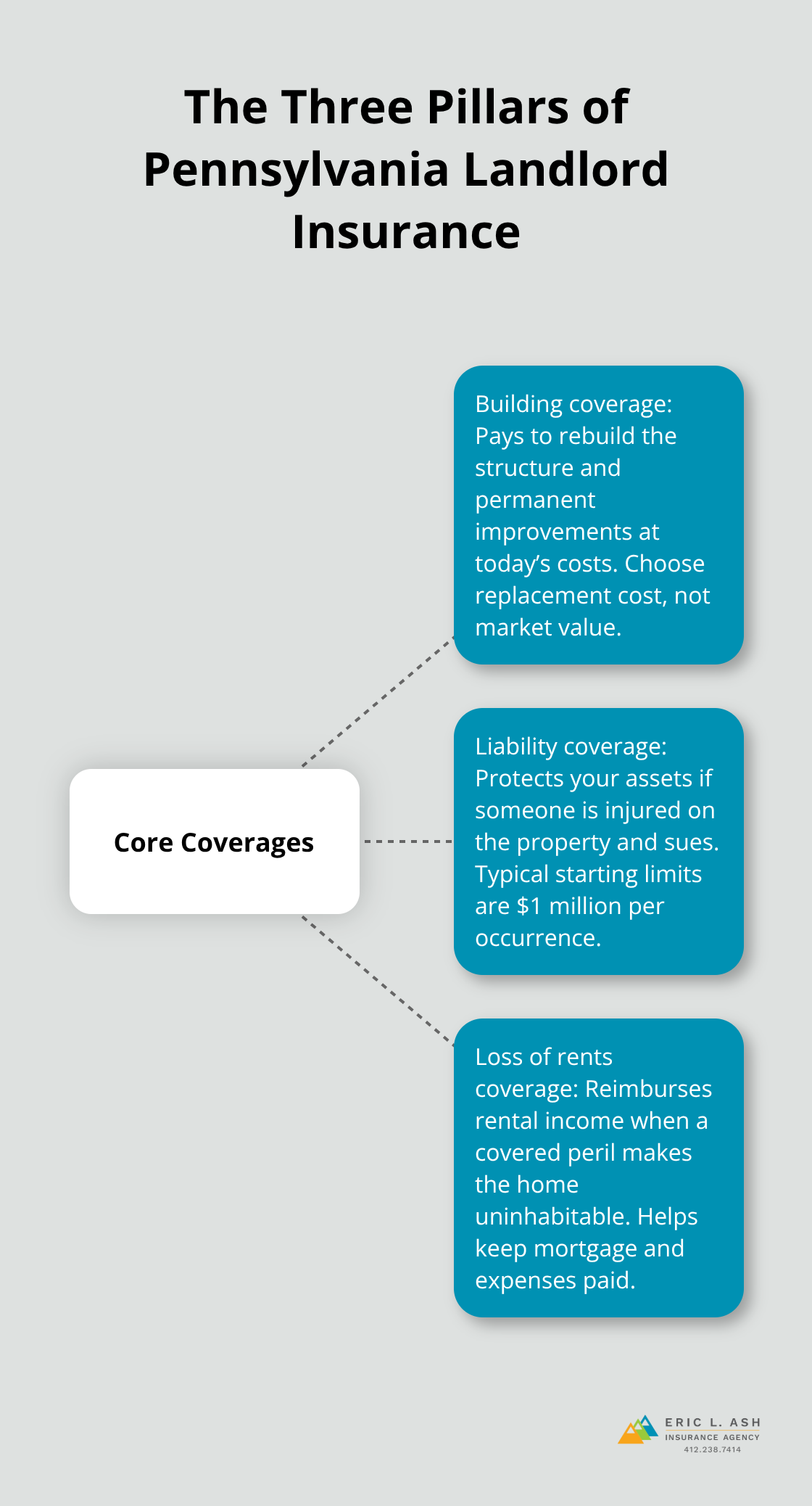

Your rental property faces three distinct financial threats: physical damage to the building itself, liability claims from injuries on the property, and lost rental income when the property becomes uninhabitable. A complete landlord insurance policy addresses all three, and skipping any one of them leaves you exposed to catastrophic losses. Building coverage protects the structure and permanent improvements you’ve invested in.

Liability coverage protects your personal assets when someone gets hurt on your property. Loss of rents coverage protects your cash flow when a covered event forces tenants out. These three elements work together, and they’re all equally important.

Building Coverage Protects Your Actual Investment

Your building coverage limit should equal the full replacement cost of rebuilding the structure from the ground up, not the property’s market value. This distinction matters enormously in Pennsylvania, where a rental property might sell for $250,000 but cost $350,000 to rebuild after a total loss due to labor and material costs. If you insure the property for $250,000, you’ll face a $100,000 shortfall when rebuilding is required. Replacement cost coverage pays what it actually costs to rebuild today, while actual cash value deducts depreciation and leaves you paying the difference yourself. Choose replacement cost coverage every single time, even though it costs more in premiums.

A Pennsylvania landlord with a 3-bedroom rental that generates $1,400 monthly rent should carry building coverage that reflects current construction costs, not 2010 values. Your insurance agent can help you calculate this through a detailed property inspection, measuring square footage, identifying structural systems, and accounting for local labor rates. Many landlords underestimate this figure because they haven’t renovated recently and don’t know current market pricing. Get quotes based on actual replacement cost, not guesswork.

Building coverage also extends to detached structures like garages, sheds, and fences on the property, plus landlord-owned equipment and appliances that you permanently install in the rental unit. If you own a furnished rental with appliances you provide, those items fall under building coverage too. Document what you own on the property because coverage limits apply separately to these items.

Liability Coverage Shields You from Judgment Claims

A tenant’s guest trips on a loose step and breaks their leg. They sue for $75,000 in medical costs and pain and suffering. Your homeowners policy denies the claim because the property is rented. Without landlord liability coverage, that $75,000 judgment comes directly from your bank account and could force you to sell the property to pay it.

General liability coverage in a landlord policy typically starts at $1 million per occurrence with $2 million aggregate limits, though you can request higher limits depending on your risk profile. Pennsylvania negligence law holds landlords responsible for maintaining safe premises, and injury claims happen more often than you’d think. A standard liability claim includes medical payments for the injured person, legal defense costs, and any settlement or judgment amount. The coverage applies whether the injury stems from a condition you knew about or should have known about, like inadequate lighting, loose railings, or unrepaired flooring.

If you operate a multi-unit building, higher liability limits make sense because more people move through common areas. A 4-unit building with 8 to 12 tenants and their guests creates significantly more exposure than a single-family rental. Try liability limits aligned with your property size and local rental rates. In Philadelphia, where monthly rents exceed $2,000, a tenant’s income loss from an injury claim carries higher damages. Request liability quotes at $1 million, $2 million, and $5 million limits to understand the cost difference and choose what fits your risk tolerance.

Loss of Rents Coverage Maintains Cash Flow During Crisis

This coverage reimburses you for lost rental income when a covered event makes the property uninhabitable. A kitchen fire forces tenants to vacate for two months while repairs happen. Without loss of rents coverage, you lose $2,800 in rent income while still paying your mortgage, property taxes, insurance, and maintenance costs. With coverage, the policy reimburses that $2,800 monthly amount for the repair period.

This protection exists specifically for rental properties because homeowners policies never address income loss. Loss of rents coverage typically reimburses for 12 months of lost rent, though the exact terms vary by policy. Some policies cap the monthly reimbursement amount, so verify the limit covers your actual monthly rent. If you charge $1,400 monthly but your policy caps reimbursement at $1,000, you absorb the $400 difference yourself. Request coverage limits that match your actual monthly rent when you quote.

This coverage applies only when a covered peril makes the dwelling uninhabitable, not when a tenant simply breaks their lease or you choose to evict. Verify what events trigger coverage and confirm the policy doesn’t exclude common Pennsylvania perils like windstorms or water damage from burst pipes. Many landlords skip this coverage to save premiums, treating it as optional. That’s a serious mistake. A single three-month vacancy after a covered loss costs far more than years of loss of rents premiums combined.

Understanding these three pillars reveals why many Pennsylvania landlords face serious gaps in their protection-and how common mistakes compound the problem.

Common Mistakes Pennsylvania Landlords Make with Insurance

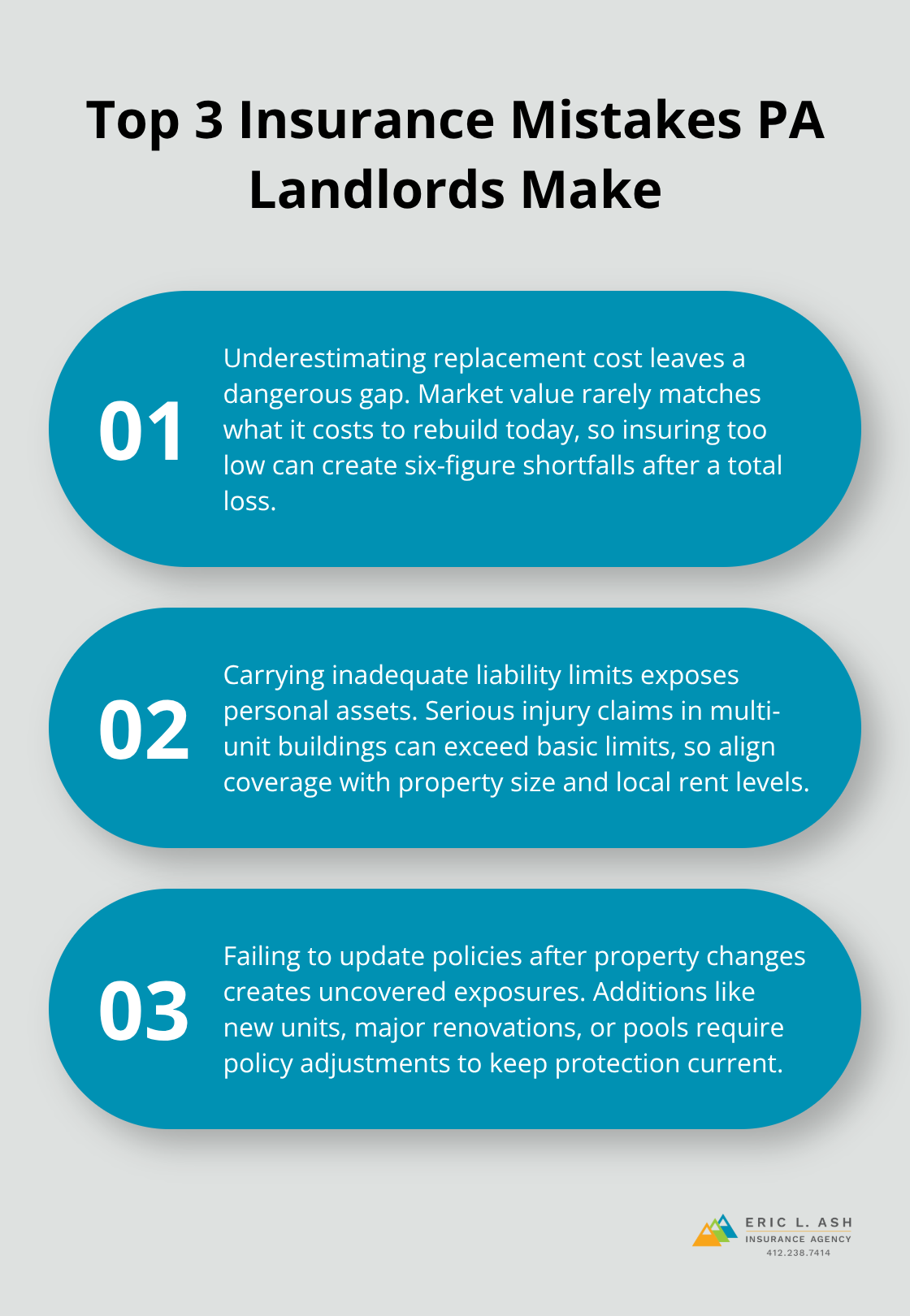

Underestimating Replacement Cost Creates Massive Gaps

Pennsylvania landlords consistently calculate building coverage based on what the property would sell for rather than what it costs to rebuild from scratch. A rental property worth $280,000 on the market might cost $420,000 to rebuild after a total loss because construction costs in Pennsylvania have increased significantly since many older buildings were originally built. If you insure for market value, you’ll face a $140,000 shortfall when the contractor presents the actual rebuild bill.

Landlords who haven’t completed recent renovations don’t realize how much construction costs have climbed. Get a replacement cost estimate from your agent, not a rough guess based on property taxes or recent appraisals. For a typical 3-bedroom rental in Pittsburgh averaging $1,400 monthly rent, underestimating replacement cost by even $50,000 creates a serious problem when you need to rebuild. Replacement cost coverage pays what it actually costs to rebuild today, while actual cash value deducts depreciation and leaves you paying the difference yourself.

Carrying Inadequate Liability Limits Exposes Your Assets

The second critical mistake involves treating liability coverage as optional or carrying limits that don’t match your property size and local rental rates. A single slip-and-fall claim in a multi-unit building can easily exceed $250,000 when medical costs, lost income, and pain-and-suffering damages combine. If your policy carries only $300,000 in liability limits and a judgment reaches $400,000, that $100,000 gap comes directly from your personal assets.

Pennsylvania negligence law holds landlords accountable for premises conditions, meaning injury claims happen more frequently than many landlords expect. Philadelphia properties generating $2,000 monthly rent justify higher liability limits because tenant income loss damages increase the claim value. Request quotes at $1 million, $2 million, and $5 million in liability coverage to understand the cost difference, then choose limits that reflect your actual exposure rather than picking the cheapest option. General liability coverage in a landlord policy typically starts at $1 million per occurrence with $2 million aggregate limits, though you can request higher limits depending on your risk profile.

Failing to Update Policies When Property Changes Occur

The third mistake involves failing to update policies when property circumstances change. A landlord who adds a second rental unit, converts a single-family home to a duplex, renovates the kitchen and bathrooms, or installs a pool creates new exposures that existing policies may not cover adequately. Your policy from three years ago likely reflects the property as it existed then, not as it exists now.

Many landlords assume their coverage automatically adjusts when they make improvements, but it doesn’t. You must notify your agent about structural changes, unit count increases, amenities additions, or tenant situation changes so coverage adjusts accordingly. If you fail to report that you’ve added a second unit and a guest gets injured in the new unit, your insurer might deny the claim because the property changed materially since the policy issued. Similarly, if you install a swimming pool and someone drowns, that exposure may be excluded unless you specifically add pool liability coverage.

Schedule a conversation with your agent each time you complete renovations, add units, or change your tenant mix so coverage stays aligned with your actual property. These three mistakes aren’t theoretical concerns-they create real financial consequences that landlords face after losses occur, when it’s too late to add missing protection.

Final Thoughts

Protecting your Pennsylvania rental property requires three specific coverage types working together: building coverage at full replacement cost, liability limits that match your property size and local rental rates, and loss of rents protection for income continuity. Verify that building coverage reflects actual reconstruction costs in today’s market, not property sale value, and confirm liability limits start at $1 million per occurrence with consideration for higher limits if you operate multi-unit buildings or properties in high-rent markets like Philadelphia. Check that loss of rents coverage reimburses your actual monthly rent for at least 12 months, and review your rental property insurance PA policy annually when property circumstances change.

The practical next step involves getting quotes from multiple carriers because coverage options and pricing vary significantly across insurers. Pennsylvania landlords benefit from working with an independent agency that shops multiple markets rather than accepting a single insurer’s offer, and an independent agent can identify coverage gaps, explain the difference between replacement cost and actual cash value, and ensure your policy reflects your specific property and income situation. They can also help you understand what events trigger loss of rents coverage and confirm that Pennsylvania-specific perils like windstorms and water damage from burst pipes are covered.

We at Eric L. Ash Insurance Agency work with landlords across Pennsylvania to build policies that actually protect their investments and income. Contact us today to discuss your rental property insurance needs and get quotes that reflect your actual exposure, whether you own a single-family rental in Pittsburgh or a multi-unit building in Philadelphia.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.