PA Young Driver Rates: Understand How Teen Auto Insurance Is Priced

Insuring a teenage driver in Pennsylvania comes with sticker shock for most parents. PA young driver rates are significantly higher than adult premiums, but understanding what drives these costs helps you find real savings.

We at Eric L. Ash Insurance Agency help families navigate teen insurance pricing every day. The good news is that several strategies can meaningfully reduce what you pay.

What Determines Your Teen’s Insurance Rate in Pennsylvania

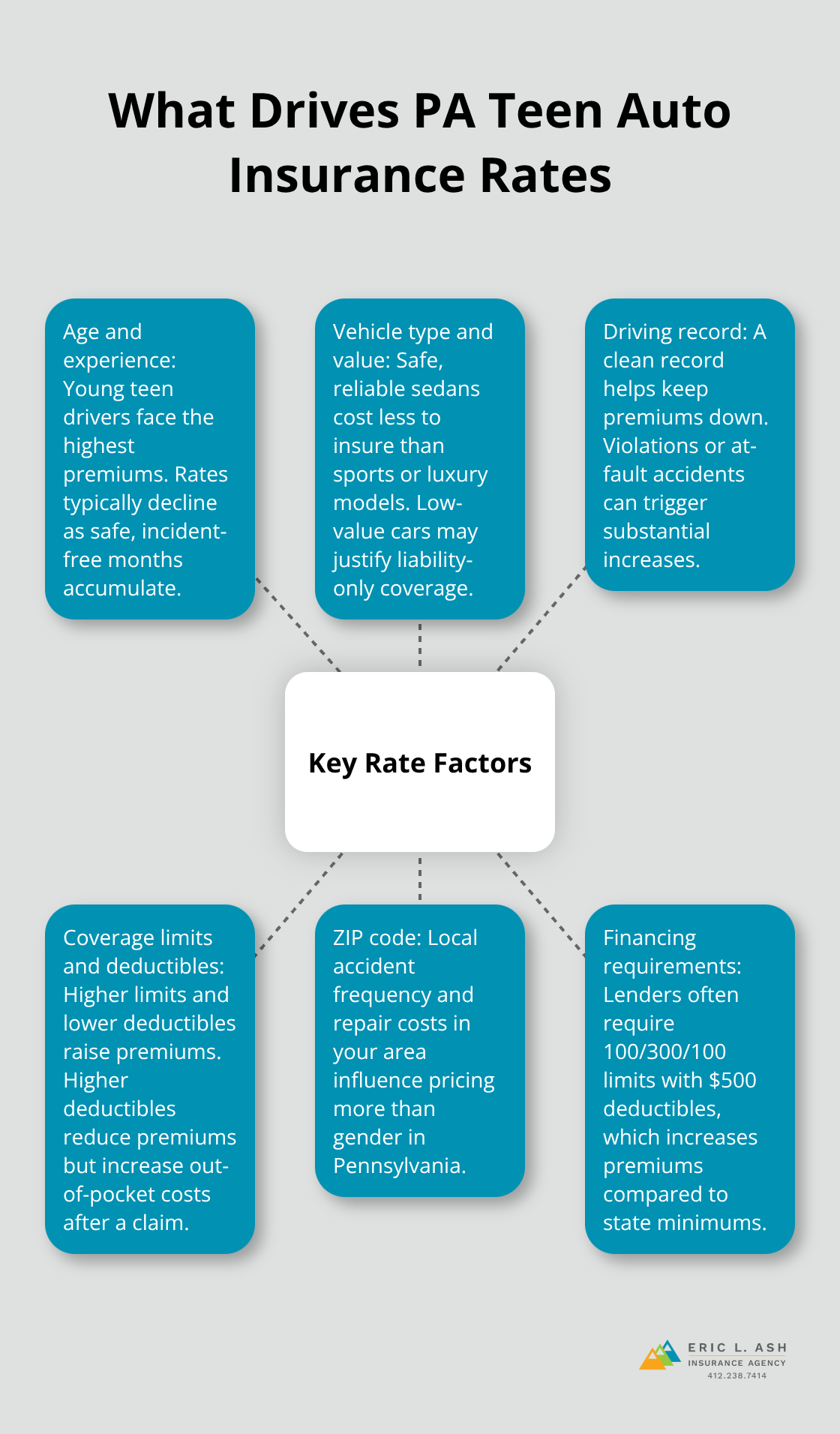

Age sits at the center of teen insurance pricing, and the numbers are stark. A 16-year-old in Pennsylvania pays an average of around $7,076 per year for full coverage, while a 19-year-old pays roughly $4,161 per year according to The Zebra’s analysis of over 32 million car insurance rates. That’s a 41% drop in just three years. Insurers charge more for younger drivers because crash risk per mile is about 3 times higher for teens aged 16-19 at night compared to adult drivers, and the fatal crash rate for teens is roughly three times higher than for drivers over 20. Inexperience, not just age itself, drives this premium. As your teen accumulates months behind the wheel without incidents, their rate should decline steadily.

How Vehicle Type Affects Your Premium

The vehicle your teen drives significantly impacts what you pay. A safe, reliable sedan costs substantially less to insure than a sports car or luxury vehicle. If your teen drives a low-value car worth under $4,000 that your family owns outright, you can drop collision and comprehensive coverage in favor of liability-only to reduce your annual premium by hundreds of dollars. This trade-off means you accept higher out-of-pocket costs after an accident, so weigh the savings against your financial comfort level.

Driving Record and Claims History

Your teen’s driving record and claims history function as a reset button on rates. A clean record keeps premiums lower, but even minor violations or at-fault accidents trigger substantial increases. Pennsylvania’s minimum liability coverage is 15/30/5, but lenders typically require 100/300/100 with $500 deductibles if your teen finances or leases a vehicle. This higher coverage level directly increases premiums compared to minimum limits.

Coverage Limits and Deductible Choices

The coverage limits and deductible you select have immediate effects on your monthly bill. Choosing higher deductibles lowers your premium but raises what you pay out-of-pocket after a claim. Conversely, lower deductibles cost more upfront but protect your wallet better when accidents happen. Your ZIP code influences rates more than gender does, reflecting local accident frequencies and repair costs in your area.

Shopping Multiple Carriers Matters

Rates vary dramatically across carriers for the same profile. Travelers quotes around $2,658 per year for a 16-year-old with full coverage in Pennsylvania, while other carriers charge $4,000 to $7,000 for the same driver and vehicle. Gender shows minimal impact in Pennsylvania for teen rates, with 16-year-old males averaging $7,080 versus females at $7,071 according to The Zebra data. When your teen first earns their learner’s permit, inform your agent immediately. Adding them to your existing family policy costs an average of $1,461 per year (a 173% increase over a typical adult driver), but this remains cheaper than purchasing a separate policy. Understanding these pricing factors positions you to identify which discounts and coverage adjustments will save you the most money.

How to Cut Your Teen’s Insurance Costs

The gap between what you pay now and what you could pay with the right strategy is substantial. A 16-year-old driver in Pennsylvania might cost $7,076 annually, but targeted discounts and smart coverage choices can trim $1,500 to $2,500 off that figure.

The Good Student Discount Delivers Immediate Savings

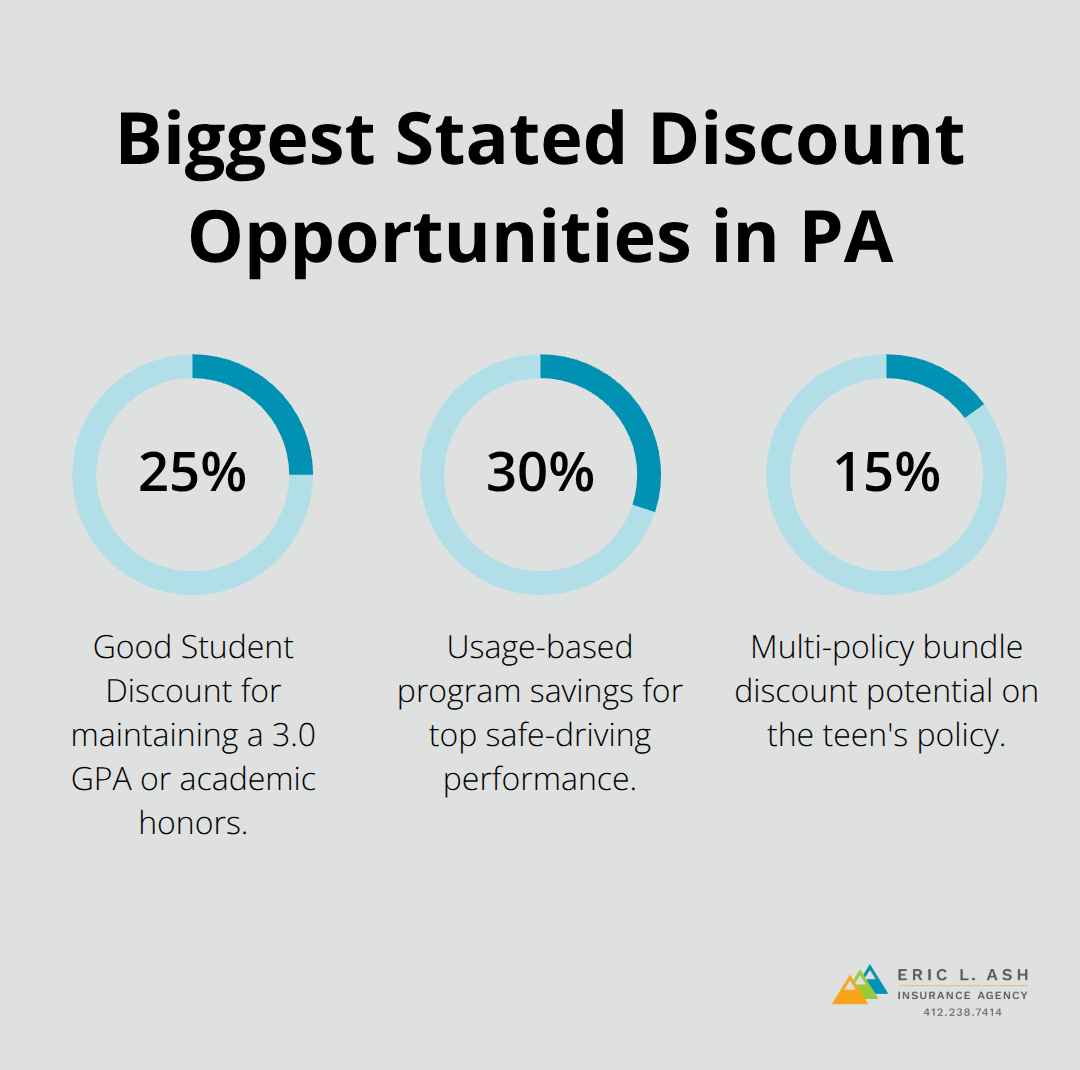

The Good Student Discount stands out as the easiest money on the table. If your teen maintains a 3.0 GPA or lands on the Dean’s List or Honor Roll, most Pennsylvania insurers will cut your premium by up to 25 percent. That discount typically continues until your teen turns 25, so a strong academic record pays dividends for years. Homeschooled students qualify by scoring well on national tests, so the path to savings exists regardless of school type. The math is straightforward: a $1,768 annual savings (25 percent of $7,076) far outweighs any tutoring costs if grades are borderline.

Driver Training Courses Reduce Risk and Premiums

Completing an approved driver training course unlocks the Driver Training Discount, which many carriers offer when all household operators under 21 finish the program. Beyond discounts, these courses genuinely reduce crash risk. Teens who complete formal driver education show measurably lower accident rates in their first year of driving compared to those who skip formal instruction.

Usage-Based Programs Reward Safe Driving Habits

Usage-based insurance programs like Steer Clear and Drive Safe & Save represent the most aggressive way to cut costs if your teen drives safely. These programs monitor real driving behavior through a mobile app or plug-in device, rewarding smooth acceleration, gentle braking, and low nighttime miles with premium reductions of 10 to 30 percent depending on performance. The catch is that poor driving habits generate no savings, so these programs work only if your teen actually drives carefully.

Stacking Discounts Creates Substantial Savings

Families serious about slashing teen insurance costs should pursue all three strategies simultaneously. Combine the Good Student Discount with driver education completion and a usage-based program, and you could reduce your annual premium by 40 to 50 percent. That transformation takes effort upfront but delivers real, measurable savings month after month. Multi-policy discounts from bundling home and auto coverage can add another 15 to 25 percent savings, translating to $150 to $300 annually on your teen’s policy alone. Once you’ve locked in these discounts, the next step involves examining which coverage options actually fit your family’s financial situation and your teen’s driving patterns.

Mistakes That Cost Pennsylvania Families Thousands on Teen Insurance

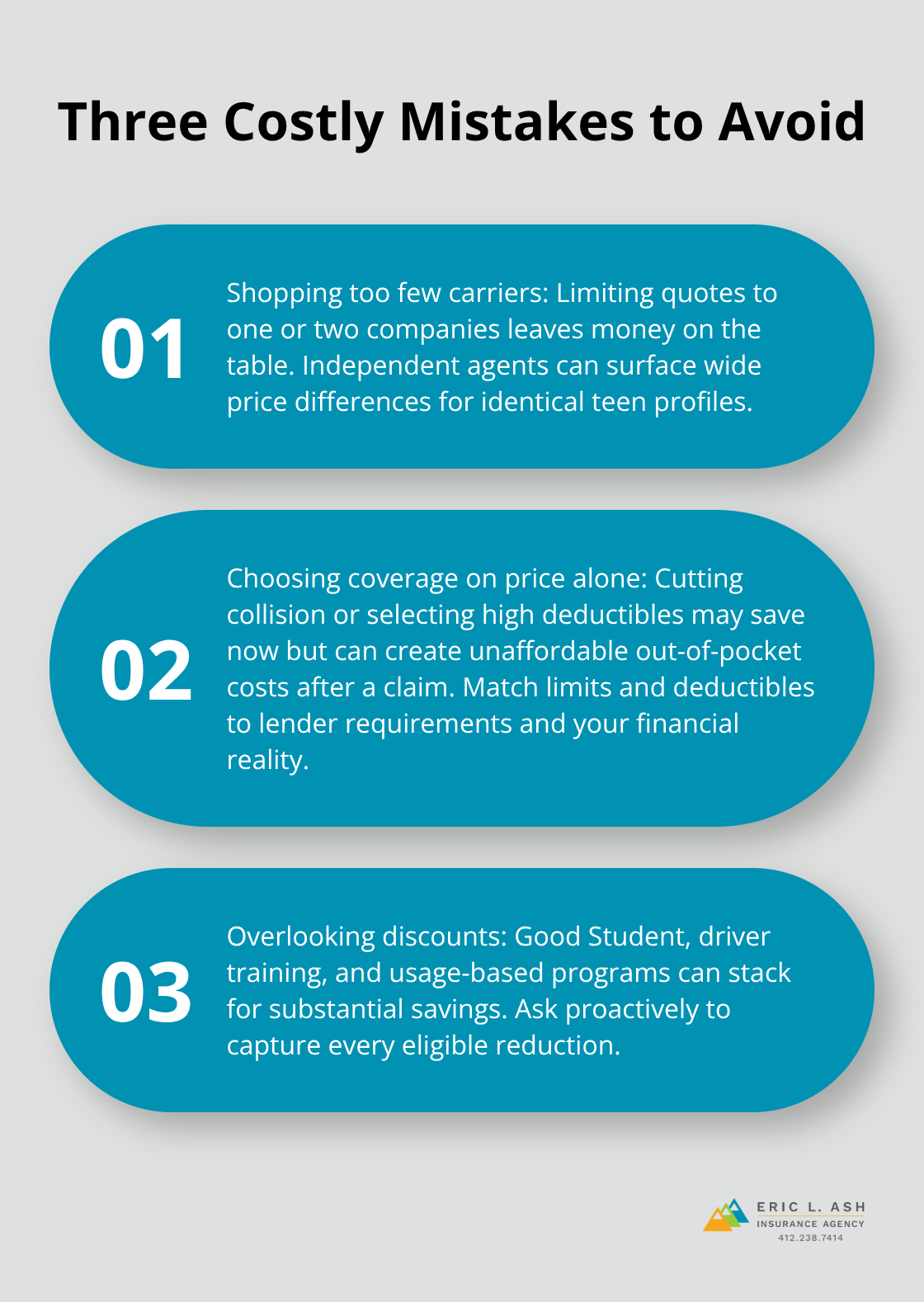

Shopping Only One or Two Carriers Leaves Money on the Table

Parents frequently make three costly errors when insuring teenage drivers: they accept the first quote without shopping competitors, they choose coverage levels based on price alone rather than actual protection needs, and they overlook discounts that directly reduce what they owe each month. The first mistake-failing to compare rates across carriers-costs families real money. Insuring a teen driver costs significantly more than insuring an adult, and shopping multiple carriers reveals substantial rate variations. Rate differences for identical driver profiles can be significant, with some carriers charging considerably more than others. That variation represents money left on the table if you stop after one or two quotes. Many parents assume all insurers price teen drivers similarly, but the data proves otherwise.

An independent insurance agency can access dozens of carriers simultaneously, eliminating the tedious process of calling each company individually and catching rate variations you’d otherwise miss.

Choosing Coverage Based on Price Alone Creates Financial Exposure

The second mistake involves making coverage decisions purely on monthly cost without understanding the financial consequences. A parent might drop collision coverage to save $40 monthly, then face a $5,000 out-of-pocket repair bill after their teen causes a minor accident. Pennsylvania’s minimum liability coverage of 15/30/5 technically satisfies state law, but lenders require 100/300/100 limits if your teen finances or leases a vehicle, and even owner-financed cars often need collision and comprehensive protection. The real trap emerges when families choose $1,000 deductibles to cut premiums, then cannot afford the deductible after a claim occurs. Your coverage selections should match your financial reality and lender requirements rather than just your budget.

Overlooking Discounts Wastes Thousands in Potential Savings

The third mistake-overlooking available discounts-represents pure negligence. If your teen maintains a 3.0 GPA or higher, the Good Student Discount cuts premiums by a meaningful percentage, potentially saving hundreds annually. Completing an approved driver training course unlocks additional savings, and usage-based programs reward safe driving with 10 to 30 percent reductions. Families who pursue all three simultaneously cut their annual cost significantly, yet many parents never ask about these options because they don’t understand they exist. Shopping multiple carriers, selecting coverage that matches your financial reality and lender requirements, and actively pursuing every available discount separates families paying substantially different amounts for the same teenage driver.

Final Thoughts

PA young driver rates reflect real risk factors that insurers measure and price accordingly. Age dominates the calculation, but vehicle type, driving record, coverage limits, and deductibles all shape what you ultimately pay. A 16-year-old in Pennsylvania might face $7,076 annually, yet that same driver could cost $4,161 by age 19 as experience accumulates and risk declines.

Reducing your teen’s insurance costs requires action on multiple fronts simultaneously. The Good Student Discount delivers up to 25 percent savings for maintaining a 3.0 GPA, a benefit that extends until your teen turns 25. Driver training courses unlock additional discounts while genuinely lowering crash risk during those critical first months behind the wheel, and usage-based programs like Steer Clear reward safe driving habits with 10 to 30 percent reductions. Families who stack these strategies together cut annual premiums by 40 to 50 percent compared to baseline rates.

Shopping multiple carriers remains non-negotiable, as rate variations for identical driver profiles can exceed $2,000 annually. Coverage decisions should match your financial reality and lender requirements rather than chase the lowest monthly payment. Contact Eric L. Ash Insurance Agency to discuss your teen’s coverage and discover how much you could save on PA young driver rates.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.