Subcontractor Insurance PA: Protecting Your Joint Venture

Subcontractors in Pennsylvania face unique insurance challenges that general contractors often overlook. A single project mishap-damaged equipment, an injury on site, or a client dispute-can derail your business financially.

We at Eric L. Ash Insurance Agency know that standard coverage rarely cuts it for subcontractors. The right subcontractor insurance PA protects your income, your tools, and your reputation when things go wrong.

Why Subcontractors Need Specialized Insurance Coverage

Standard general liability policies sold to most small businesses leave subcontractors dangerously exposed. A typical commercial general liability policy covers bodily injury and property damage you cause to others, but it often excludes or severely limits coverage for tools, equipment left at job sites, and materials you’ve purchased but haven’t installed yet. Pennsylvania subcontractors regularly lose thousands when equipment gets stolen from a job site or damaged before installation because their basic GL policy doesn’t cover it. The Pennsylvania Department of Labor & Industry reports that subcontractor disputes over liability and coverage gaps rank among the top insurance complaints filed in the state. You need coverage that addresses what actually happens on your jobs, not what a one-size-fits-all policy assumes.

The Real Cost of Coverage Gaps

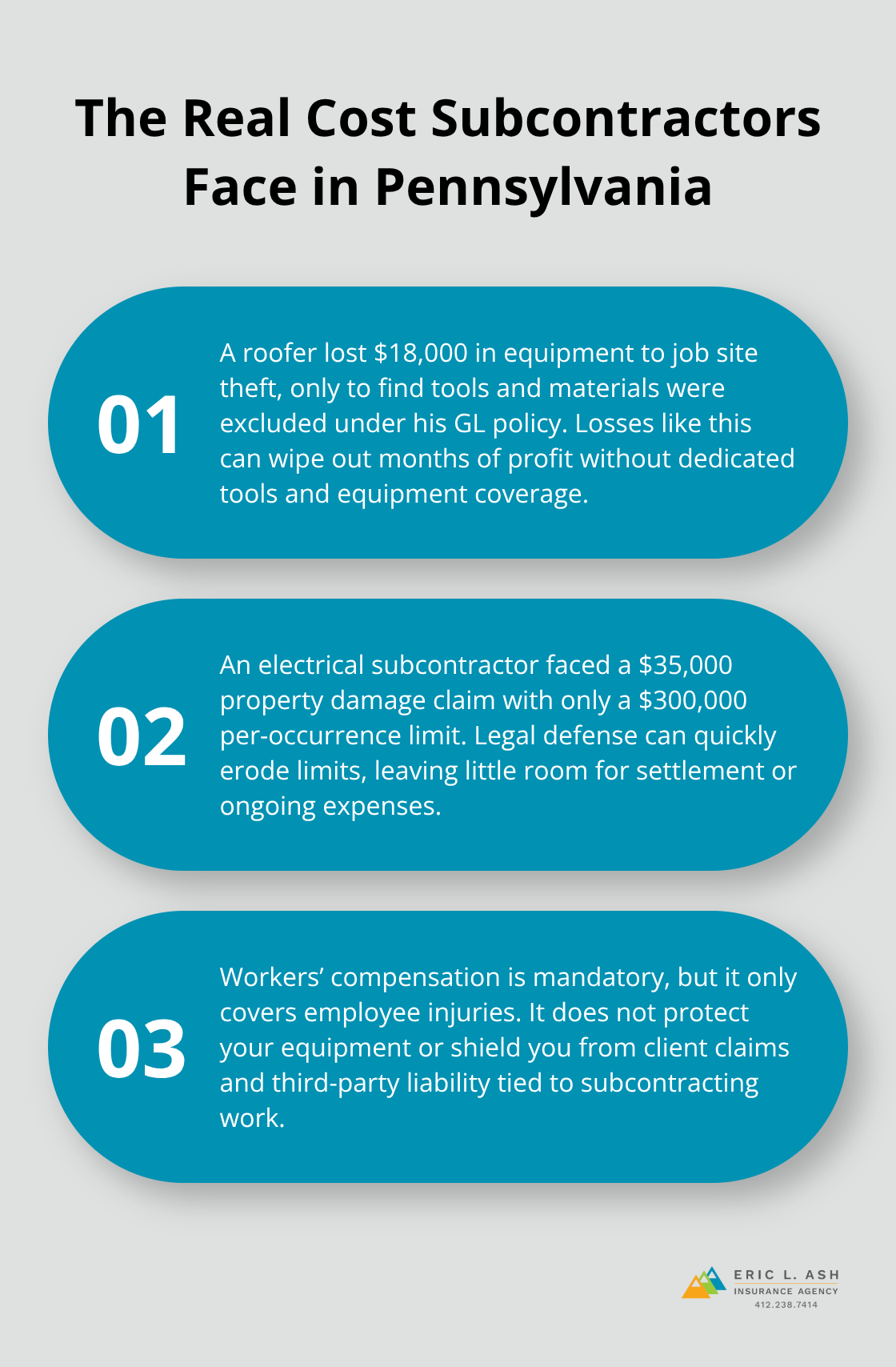

When you work as a subcontractor on someone else’s project, your exposure differs fundamentally from a general contractor’s. You don’t control the overall site safety, you don’t manage all the trades, and you’re often the last one blamed when something goes wrong. A roofer in Pittsburgh lost $18,000 worth of equipment to theft from a residential job site last year, only to discover his GL policy excluded tools and materials. An electrical subcontractor in Philadelphia faced a $35,000 liability claim after faulty wiring caused property damage, but his policy limits of $300,000 per occurrence left little cushion for legal defense costs. These aren’t hypothetical scenarios-they’re the situations that force subcontractors out of business. Your workers’ compensation coverage is mandatory in Pennsylvania, but it covers only employee injuries, not the property you bring to the job or the liability exposure unique to subcontracting work.

What Actually Protects Your Business

Equipment coverage separate from your GL policy reimburses you when tools, ladders, compressors, or materials suffer damage, theft, or loss at a job site. Many carriers in Pennsylvania now offer equipment floaters that cover your property while it travels to the job and while it sits on-site, with coverage limits you control. Commercial auto insurance becomes critical if you transport equipment or materials regularly-a basic GL policy excludes vehicle-related incidents entirely. Completed operations coverage extends your protection after you finish a job, covering claims that arise from your work later on. Pennsylvania’s Statute of Repose allows homeowners to file claims for up to 12 years after project completion on certain defects, so completed operations coverage can save you from unexpected liability claims years after the job ends. Tools and equipment coverage typically costs $300 to $800 annually depending on your equipment value and trade, but it prevents the catastrophic losses that wipe out profits for months.

Why Subcontractors Face Unique Risks

Subcontractors operate in a liability environment that differs sharply from general contractors. You work on sites you don’t control, alongside trades you don’t supervise, and under contracts that often shift risk onto your shoulders. A general contractor may carry $1 million in GL coverage and pass liability down to you through indemnification clauses in your subcontract. That means you absorb the cost of defending claims and paying damages, even when another trade caused the problem. Pennsylvania joint ventures that rely on subcontractors experience more delays, rework, and cost overruns due to variable performance and inconsistent quality across trades. Your insurance must account for this reality-you need higher limits, broader coverage, and protection against claims that arise from work you didn’t directly cause but are contractually responsible for.

The Three Insurance Policies Subcontractors Cannot Skip

Workers’ compensation insurance is not optional in Pennsylvania-it’s the law. The Pennsylvania Department of Labor & Industry requires every subcontractor with employees to carry coverage, with penalties reaching $15,000 and personal liability for all claims if you don’t comply. Your workers’ comp policy covers employee medical bills and lost wages after a work injury, but here’s what most subcontractors misunderstand: it does not cover your own injuries if you’re a sole proprietor, and it does not protect you against liability claims from clients or third parties. Many subcontractors assume workers’ comp solves their insurance problem, then face financial disaster when a homeowner sues them for property damage or a client claims their work caused injury.

Workers’ Compensation Costs Vary Sharply by Trade

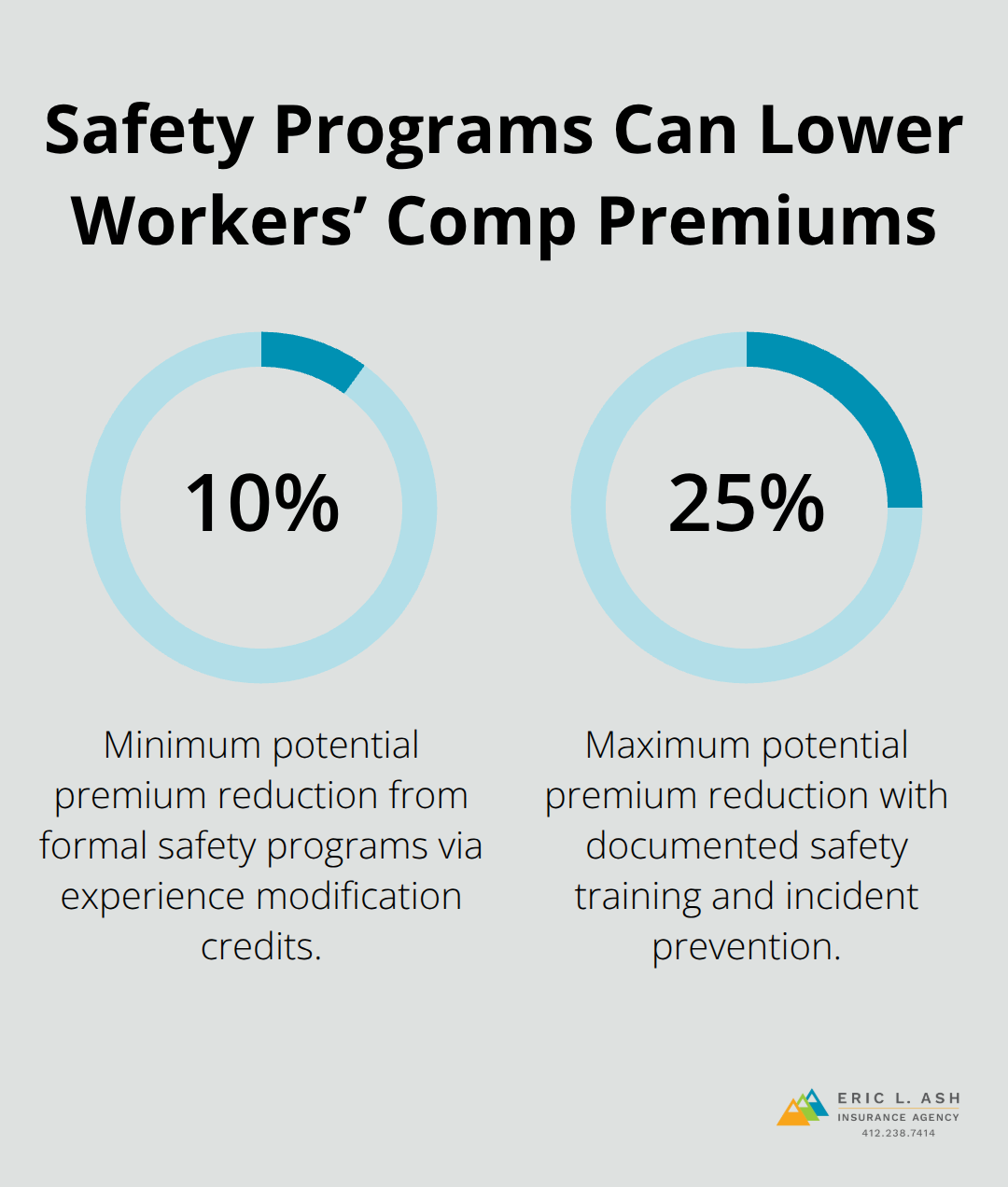

The cost varies significantly by trade in Pennsylvania. A general contractor pays about $3.92 per $100 of payroll annually, while a roofer pays $12.48 per $100-nearly three times higher. An electrician pays around $2.89 per $100, an HVAC technician about $3.45, and a plumber about $4.12. This means a roofer with one employee earning $50,000 annually pays roughly $6,240 in workers’ comp, while an electrician with the same payroll pays about $1,445. Formal safety programs reduce these costs by 10 to 25 percent through experience modification credits, so investing in documented safety training and incident prevention directly lowers your premiums.

General Liability Coverage Protects Against Client Claims

Commercial general liability insurance protects you when your work injures someone or damages their property. A $300,000 per-occurrence limit sounds reasonable until you’re defending a claim-legal defense costs alone can consume half that amount before settlement. We recommend subcontractors carry at least $1 million per occurrence and $2 million aggregate, which exceeds Pennsylvania’s Home Improvement Consumer Protection Act minimums of $50,000 but reflects real-world claim severity. A typical GL policy for a subcontractor in Pennsylvania costs $600 to $1,200 annually depending on your trade and claims history.

However, standard GL policies exclude or severely limit coverage for tools, equipment, and materials-the very assets subcontractors lose most often. Tools and equipment coverage fills this gap with a separate floater policy that protects your property while traveling to jobs and while sitting on-site. Equipment theft from job sites happens regularly in Pennsylvania, and your GL policy will not reimburse you. A floater typically costs $300 to $800 annually based on your equipment inventory value and covers theft, damage, and loss.

Completed Operations Coverage Protects Your Long-Term Liability

Completed operations coverage extends protection after project completion, covering claims that emerge years later. Pennsylvania’s 12-year Statute of Repose on certain defects means a homeowner can file a claim a decade after you finish work, and completed operations coverage shields you from that long-tail liability. Most subcontractors skip this coverage and regret it when an old job surfaces a claim.

The typical Pennsylvania subcontractor insurance package-workers’ comp, GL, and equipment coverage-averages around $2,500 to $4,000 annually depending on your trade and payroll size. This investment protects your business from the kinds of losses that force subcontractors out of work. Understanding what each policy covers sets the foundation for protecting yourself, but selecting the right coverage limits and deductibles requires a closer look at your specific project risks and contract obligations.

Choosing Coverage Limits That Match Your Real Exposure

Start with Your Contract Obligations

Read your subcontract indemnification clause carefully-it often requires you to carry specific liability limits and name the general contractor as additional insured. A general contractor may demand $1 million per occurrence and $2 million aggregate, which means your policy must meet that threshold or you violate your contract. Pennsylvania joint ventures frequently require subcontractors to carry umbrella or excess liability policies that extend coverage, especially on large residential or commercial projects. Check your current contracts now: if three projects require $1 million limits and one requires $2 million, you need at least $2 million to stay compliant. Carrying less exposes you to contract breach and personal liability if a claim exceeds your policy limits.

Assess Your Actual Risk Beyond Contract Minimums

A roofer working on residential homes faces different exposure than an electrician installing systems in new construction. A roofing subcontractor in Pennsylvania typically carries $1 million per occurrence because fall hazards and weather-related damage create higher claim frequency. An HVAC technician might carry $500,000 to $1 million depending on whether they work on high-value commercial systems. Your deductible choice directly affects your premium: a $2,500 deductible costs roughly 15 to 25 percent less than a $1,000 deductible, but only if you can absorb that deductible from cash flow when a claim hits. A small plumbing subcontractor with limited reserves should choose a $1,000 deductible even if it costs more annually-a $5,000 water damage claim with a $2,500 deductible creates cash flow stress that $1,500 in annual premium savings doesn’t offset.

Calculate Equipment Coverage Based on Inventory Value

List every item you transport to job sites: power tools, ladders, compressors, diagnostic equipment, materials staged on-site. Total that value honestly. A roofing crew with ladders, nailers, compressors, and safety gear often carries $40,000 to $60,000 in equipment. An electrician with diagnostic tools, wire, conduit, and fixtures might have $25,000 to $40,000 exposed. Request quotes for equipment floaters at 80 percent and 100 percent of your inventory value-the premium difference is usually 10 to 15 percent, and 100 percent coverage eliminates painful partial-loss scenarios. Many Pennsylvania subcontractors undervalue their equipment inventory by 30 to 40 percent, then suffer when a claim reveals the actual loss. Photograph your equipment, document serial numbers, and update your inventory annually as you add tools.

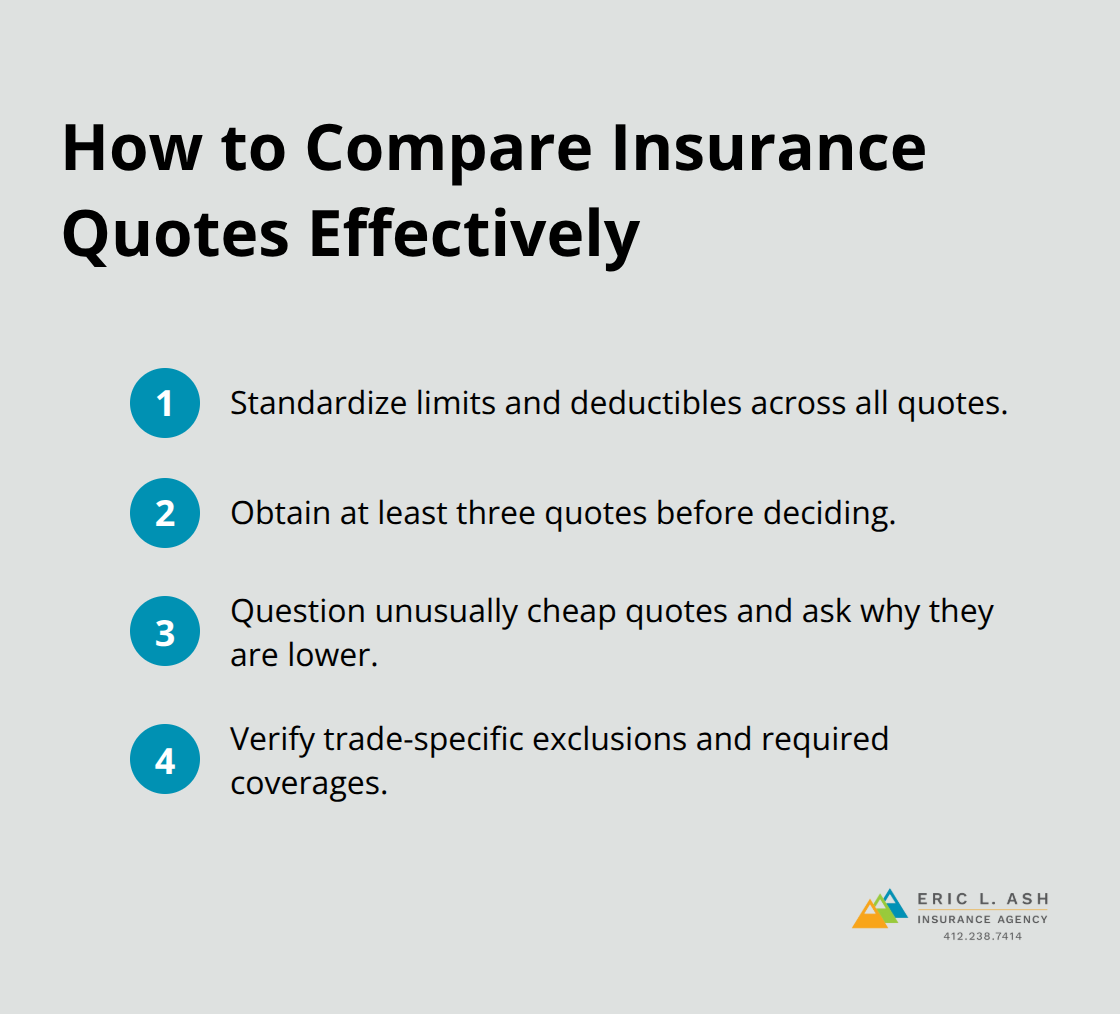

Compare Quotes Across Multiple Carriers

When comparing quotes from different carriers, request the same coverage limits and deductibles so premiums are truly comparable. A $1 million GL policy with a $1,000 deductible should cost roughly the same across carriers, though experience modification ratings and your claims history can shift pricing by 15 to 30 percent. If one carrier quotes $400 annually and another quotes $600 for identical coverage, the difference reflects their underwriting appetite or your risk profile-ask why before accepting the lower quote, because the cheapest option often comes with poor claims service or coverage restrictions.

Try obtaining at least three quotes before committing, and request that each carrier explain what their policy excludes for your specific trade. An HVAC subcontractor should confirm that refrigerant liability and equipment breakdown are covered or excluded; an electrical subcontractor should verify that design professional liability is available if you create custom installations. These trade-specific gaps often appear only when you read the exclusions carefully.

Final Thoughts

Subcontractor insurance PA protects your business from the financial devastation that follows a single mishap. Workers’ compensation, general liability, and equipment coverage work together to shield your income, your tools, and your reputation when claims arise. Standard policies leave gaps, and those gaps cost subcontractors thousands in uninsured losses every year.

Your contract obligations often demand specific coverage limits, so read your indemnification clauses before selecting a policy. Your actual risk profile-shaped by your trade, the projects you pursue, and the equipment you carry-should drive your coverage decisions, not just the lowest premium available. Request quotes from at least three carriers using identical coverage limits and deductibles so you can compare apples to apples.

Local Pennsylvania agents understand the state’s regulatory landscape and the real risks subcontractors face. We at Eric L. Ash Insurance Agency work with dozens of carriers to deliver competitive rates and tailored coverage backed by responsive, local customer service. Contact Eric L. Ash Insurance Agency to discuss your subcontractor insurance needs and get a quote that reflects your real business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.