Teen Driver Vehicle Coverage Essentials

Getting your teen behind the wheel is a major milestone. It’s also a major financial responsibility, and teen driver vehicle coverage isn’t something you can skip or minimize.

At Eric L. Ash Insurance Agency, we know that teen drivers face real risks on the road-and those risks come with real costs. This guide walks you through the coverage types that matter, the discounts available to you, and how to protect both your teen and your family’s finances.

Why Teen Drivers Cost More to Insure

The CDC Data on Teen Crash Risk

Teen drivers aged 16 to 19 have the highest motor vehicle crash risk of any age group, according to the CDC. Fatal crash rates at night among teen drivers are about 3 times as high as those of adult drivers. Inexperience, risk-taking behavior, and peer pressure combine to create a dangerous mix on the road. The Insurance Information Institute reports that adding a teen driver to your policy can increase your family’s auto insurance premium by 50 to 100 percent. This isn’t a minor adjustment-it’s a substantial financial impact that hits at renewal time, right when your teen earns their full license.

Pennsylvania’s Graduated Driver Licensing Advantage

Pennsylvania’s Graduated Driver Licensing program, which started in 1999 and was updated in 2011, reduces this risk through a step-by-step approach. During the learner’s permit phase, your teen practices under adult supervision for at least six months and 65 hours of driving time (including 10 hours at night and 5 hours in poor weather). Most insurers don’t charge extra during the permit stage, so this window offers you a chance to delay the premium spike.

The number 100% seems to be not appropriate for this chart. Please use a different chart type. Once your teen passes the road test and gets their junior license, the costs jump significantly because they now have independent driving privileges.

Disclosure Requirements and Policy Obligations

Pennsylvania requires liability coverage on every vehicle, and that requirement doesn’t change for teen drivers. Your teen must appear on your policy or face formal exclusion, and failing to disclose a licensed household member can trigger premium increases or claim denials. A single accident involving your teen can cost thousands in vehicle repairs, medical bills, and potential liability claims. If your teen causes a collision that injures another person, your liability coverage pays for their medical expenses and property damage-but only up to your policy limits.

The True Cost of Teen Accidents

Many families carry minimum limits to keep premiums down, which creates serious exposure when a teen is driving. Underinsured motorist coverage protects your family if the other driver lacks adequate insurance, and collision and comprehensive coverage protect your own vehicle from damage. Insurance companies track claims and violations, and a single accident can keep your teen’s rates elevated for years. The real cost of teen driver accidents extends far beyond the immediate repair bill.

Understanding these costs and risks sets the stage for selecting the right coverage types-the decision that actually protects your teen and your family’s financial security.

What Coverage Protects Your Teen Driver

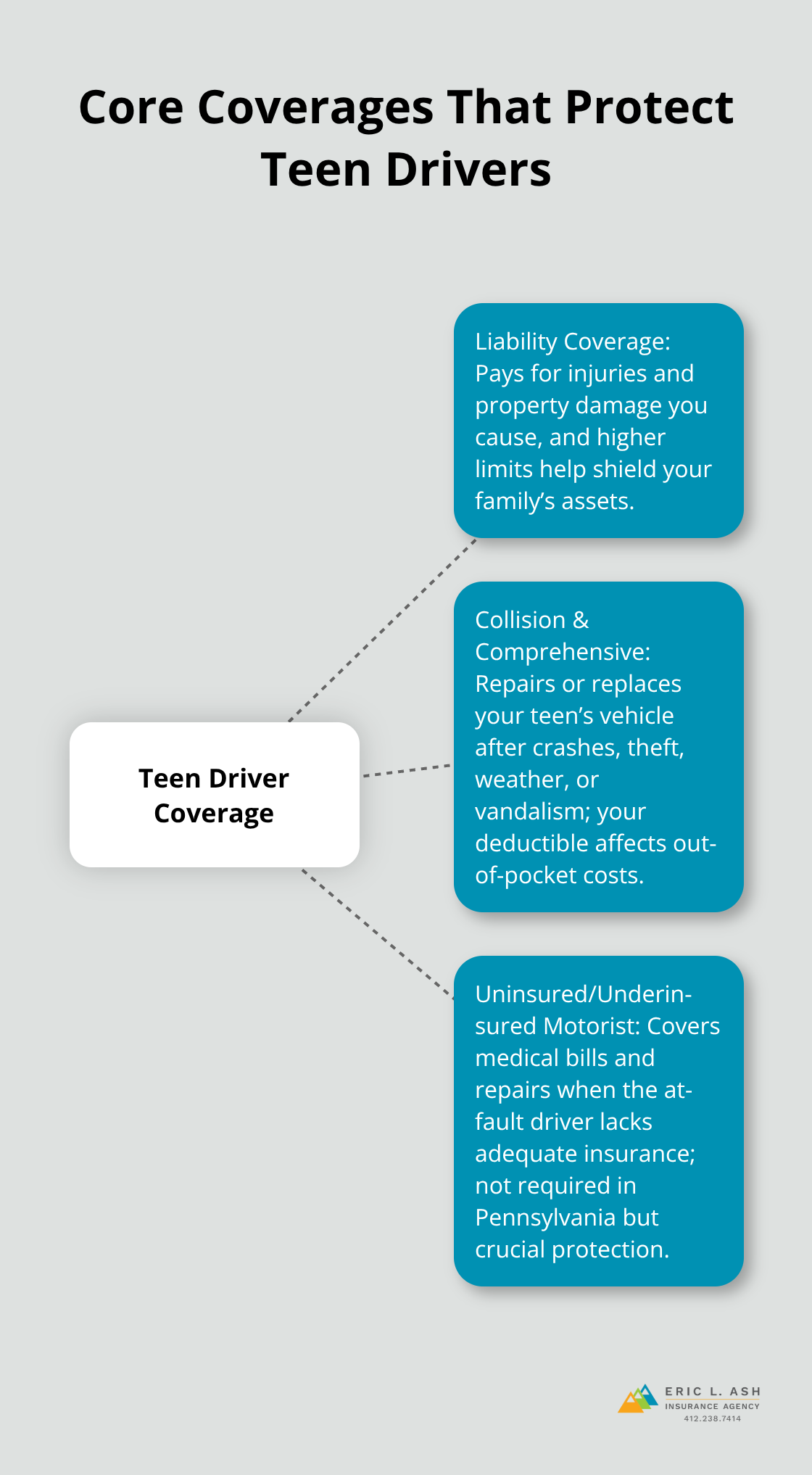

Liability Coverage: Your First Line of Defense

Liability coverage is your first line of defense, and Pennsylvania law requires it on every vehicle. The state’s minimum is $5,000 for property damage. Those limits sound adequate until your teen causes a serious accident. A single collision that injures multiple people or damages an expensive vehicle quickly exceeds these minimums, leaving your family responsible for the difference. We recommend carrying at least $100,000 per person and $300,000 per accident for bodily injury, especially when a teen drives your vehicle. Higher limits cost only slightly more at renewal but shield your family’s assets if a major accident occurs. Many families underestimate how fast medical bills and vehicle repair costs accumulate after a teen-caused collision.

Collision and Comprehensive Coverage: Protecting the Vehicle

Collision and comprehensive coverage protect your teen’s vehicle from damage whether they’re at fault or not. Collision covers accidents with other vehicles or objects, while comprehensive handles theft, weather, vandalism, and other non-collision damage. Your deductible matters here: a $500 deductible costs less upfront but means you pay more out-of-pocket after an accident, while a $1,000 deductible lowers your premium but increases your financial burden when claims happen. For teen drivers, a $500 deductible often makes sense because inexperienced drivers file more claims. This lower deductible reduces the financial shock when your teen needs to file a claim.

Uninsured and Underinsured Motorist Coverage: Filling the Gap

Uninsured and underinsured motorist coverage fills a critical gap that many families overlook. If another driver hits your teen and lacks adequate insurance, this coverage pays for your teen’s medical bills and vehicle repairs up to your policy limits. Pennsylvania doesn’t require this coverage, but statistics show roughly one in eight drivers on the road carries no insurance at all. Without uninsured motorist protection, your teen and family absorb those costs directly. This coverage protects your family from financial devastation when an uninsured or underinsured driver causes the accident.

Building a Foundation That Works

These three coverage types form the foundation of a teen driver policy that actually protects against real-world scenarios, not just legal minimums. The combination of adequate liability limits, collision and comprehensive protection, and uninsured motorist coverage creates a safety net that covers most situations your teen might face on Pennsylvania roads. With the right coverage in place, you’ve addressed the major financial risks-but your premium costs don’t have to stay high.

Discounts and smart choices can significantly reduce what you pay each month, and understanding those options helps you protect both your teen and your budget.

Cutting Teen Driver Premiums Without Cutting Coverage

The coverage foundation we outlined protects your teen, but the costs don’t have to drain your budget. Three practical strategies cut premiums substantially, and each one addresses real behaviors or achievements that insurance companies reward with measurable discounts. Good student discounts reward academic performance directly, driver education courses build measurable skills, and usage-based programs track actual driving behavior. Pennsylvania families who combine these approaches see premium reductions that compound over time.

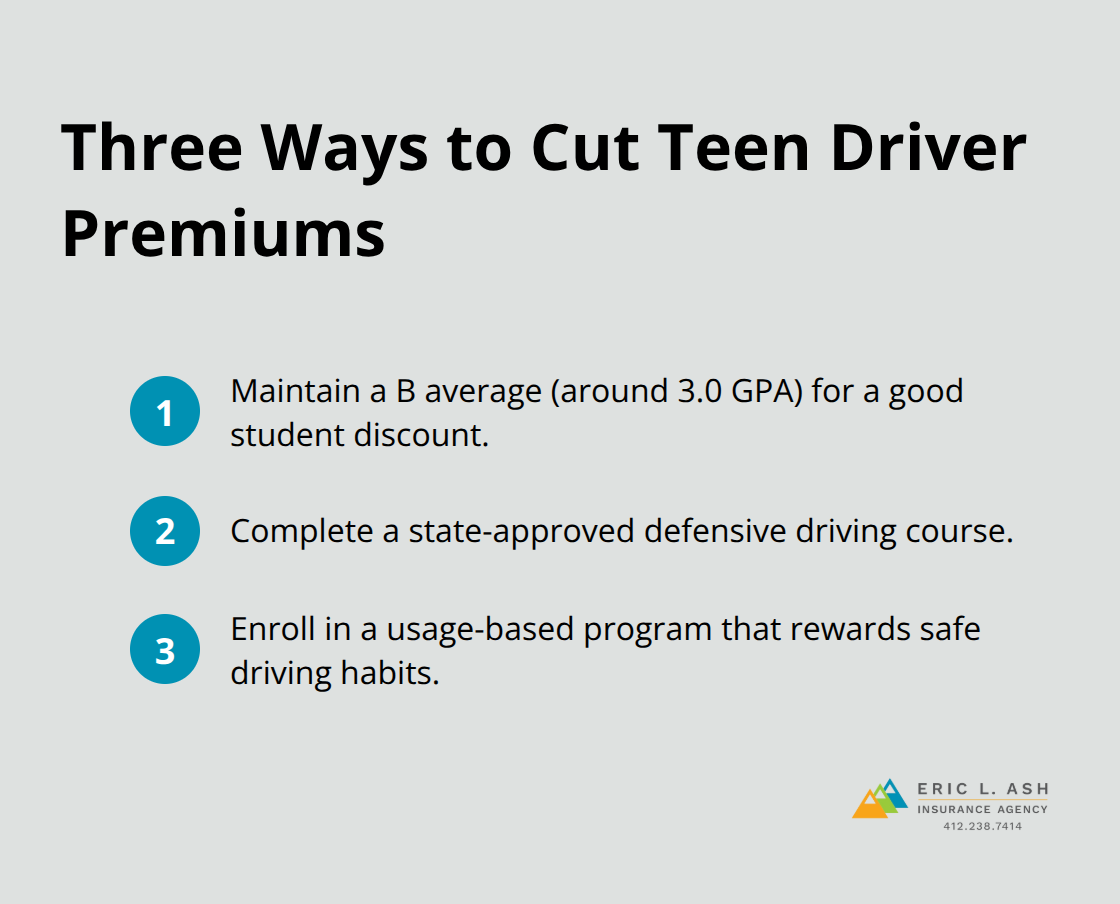

Good Student Discounts: Reward Academic Achievement

Good student discounts apply when your teen maintains a B average or higher, typically a 3.0 GPA or above, and many insurers offer discounts ranging from 10 to 15 percent just for maintaining grades. This discount costs nothing except the academic effort your teen already invests, making it the easiest win available. Your teen’s report card directly translates into lower insurance costs, creating a tangible financial incentive for academic success.

Defensive Driving Courses: Build Real Skills

Enroll your teen in a defensive driving course before they earn their license, and you unlock another discount that typically ranges from 5 to 10 percent. These courses teach hazard recognition and emergency maneuvers that actually reduce crash frequency, so insurers price them as genuine risk reduction. The course takes a few hours online or in-person and qualifies your teen for discounts that persist for years. Your teen learns to anticipate dangerous situations and react appropriately, skills that matter far more than the discount itself.

Usage-Based Programs: Monitor and Reward Safe Driving

Usage-based insurance programs typically use a smartphone app to measure the amount of driving and risky behaviors like hard braking and handheld phone use. These programs create transparency: your teen sees how their habits affect their rate, which creates accountability. Families with teens who use these programs report that the monitoring effect itself improves driving behavior, turning the discount into genuine safety improvement.

Stacking Discounts for Maximum Savings

Combine all three approaches, and you’re looking at cumulative savings that reduce that 50 to 100 percent premium increase substantially. A teen with a 3.0 GPA, a completed defensive driving course, and safe driving behavior tracked through a usage-based program could see total discounts exceeding 30 percent. That’s not theoretical savings-that’s real money staying in your account every month for years. When you stack these discounts, the financial impact shifts from a burden to a manageable expense that rewards your teen’s responsible choices.

Final Thoughts

Teen driver vehicle coverage protects your teen on Pennsylvania roads and shields your family’s assets when accidents happen. The coverage types we’ve outlined-liability, collision, comprehensive, and uninsured motorist protection-form a complete safety net that prevents financial devastation after a crash. Pennsylvania’s minimum liability limits leave you dangerously exposed, especially when a teen drives your vehicle, so carrying adequate limits costs only slightly more but protects everything you’ve built.

The premium increase that comes with adding a teen driver feels steep, but multiple discount opportunities bring those costs down substantially. A good student discount, a completed defensive driving course, and enrollment in a usage-based program create real savings that compound over time. These discounts aren’t theoretical-families who stack them see reductions exceeding 30 percent, and your teen’s academic performance, willingness to take a safety course, and demonstrated safe driving habits directly lower what you pay each month.

An independent insurance agent can review your household, your teen’s vehicle, and available discounts to build a policy that balances protection and cost. Contact Eric L. Ash Insurance Agency to work with multiple carriers and find competitive rates tailored to your family’s needs. The right teen driver vehicle coverage protects your teen and your family’s financial security for years to come.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.