Teen Driver Coverage PA: Finding the Right Policy

Insuring a teenage driver in Pennsylvania comes with real financial challenges. Premiums can spike 50% to 100% higher than adult drivers, making teen driver coverage PA one of the biggest expenses for families.

We at Eric L. Ash Insurance Agency help parents navigate these costs without overpaying. This guide walks you through rate factors, coverage options, and proven strategies to cut your premiums.

What Actually Drives Teen Insurance Costs in Pennsylvania

Age Creates the Biggest Premium Jump

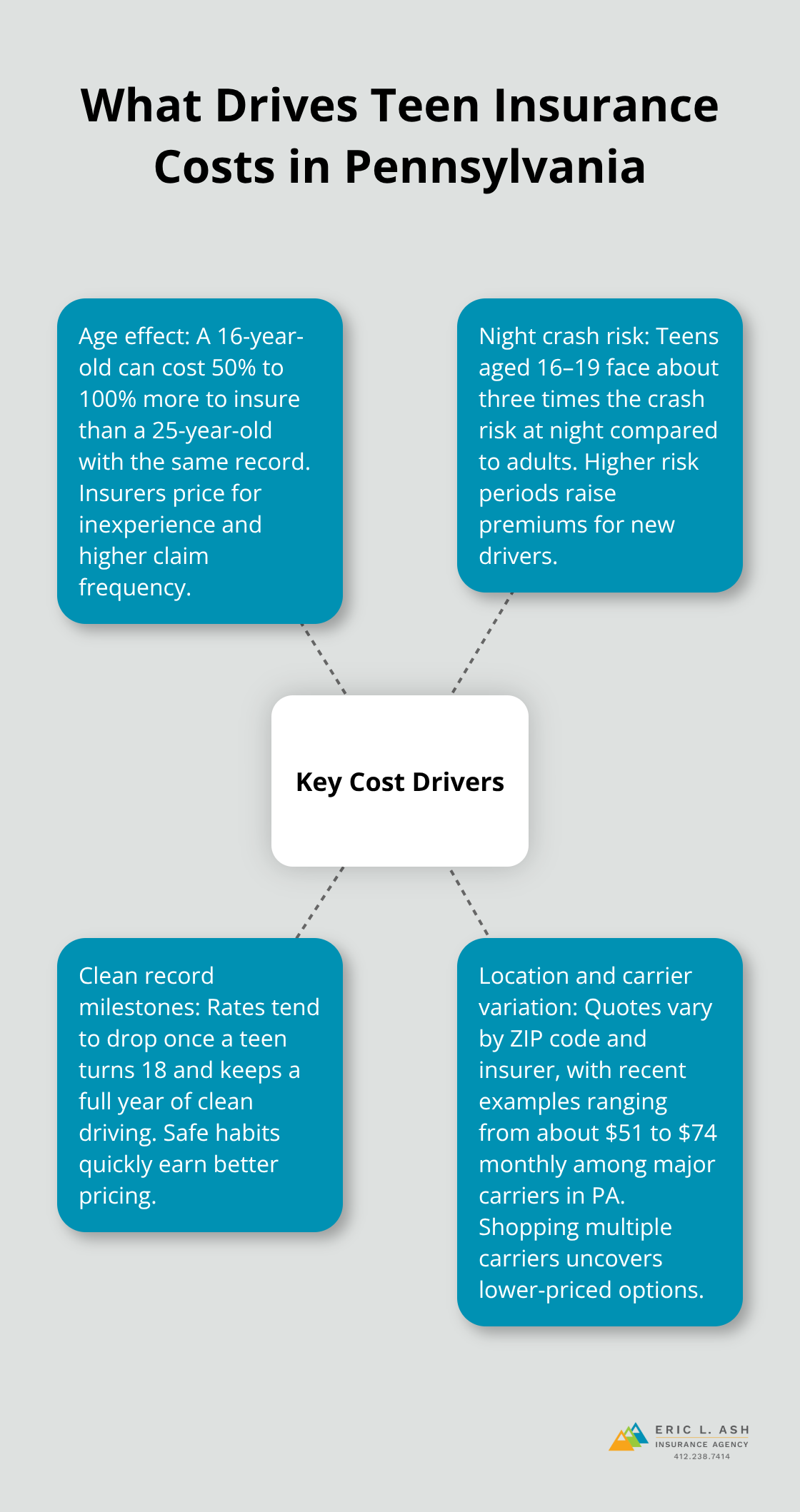

Age matters far more than most parents realize. A 16-year-old costs 50% to 100% more to insure than a 25-year-old with the same driving record, according to WalletHub data across major Pennsylvania insurers.

CDC research explains this gap: teens aged 16-19 face about 3 times the crash risk at night compared to adult drivers, primarily due to inexperience and underdeveloped hazard perception. The positive side is that premiums drop measurably once a teen reaches 18 and maintains a clean record for a full year.

Current quotes show the range across carriers. GEICO charges around $68 monthly for a Pennsylvania teen, while State Farm runs about $74 monthly for ages 16-24 with good driving history. These numbers shift significantly by ZIP code-rural areas often cost less than suburban or urban regions-so obtain quotes specific to your location rather than relying on statewide averages.

Your Teen’s Driving History Determines Rate Increases

Your teen’s driving history matters immediately. A single ticket or accident adds $200 to $400 annually to premiums, while a DUI suspension creates rates that stay elevated for years. This is why the Pennsylvania Graduated Driver Licensing program, which has been in place since 1999, actually helps your insurance costs. Teens who complete the full learner’s permit phase with 65 hours of supervised driving (including 10 hours at night) before moving to a junior license demonstrate lower crash risk to insurers, which translates to better rates than teens who skip this process.

Vehicle Choice Directly Impacts Monthly Costs

The type of car your teenager drives affects insurance costs significantly. A used Honda Civic costs far less to insure than a new Dodge Charger, not just because the Civic is cheaper to repair but because insurers view older, modest vehicles as less likely to encourage speeding or reckless driving. High-performance vehicles trigger automatic rate increases, sometimes adding $50 or more monthly. Try a reliable sedan or compact car with strong safety ratings, and you’ll see immediate savings.

Shopping Multiple Carriers Reveals Hidden Savings

When comparing insurers, don’t assume national carriers offer the best rates. Erie Insurance and Travelers frequently undercut GEICO and State Farm in Pennsylvania, with Erie averaging around $68 monthly and Travelers around $51 monthly according to WalletHub analysis. Shop at least three carriers before deciding, because the difference between the cheapest and most expensive option for your specific situation often exceeds $600 annually.

As an independent agency with relationships across dozens of carriers, we at Eric L. Ash Insurance Agency leverage these multiple markets to help you find competitive rates tailored to your teen’s profile. The next section covers the specific coverage options you’ll encounter when building a policy, so you understand what protection each type provides and which options make sense for your family’s situation.

Coverage Options for Teen Drivers in PA

Meeting Pennsylvania’s Minimum Requirements

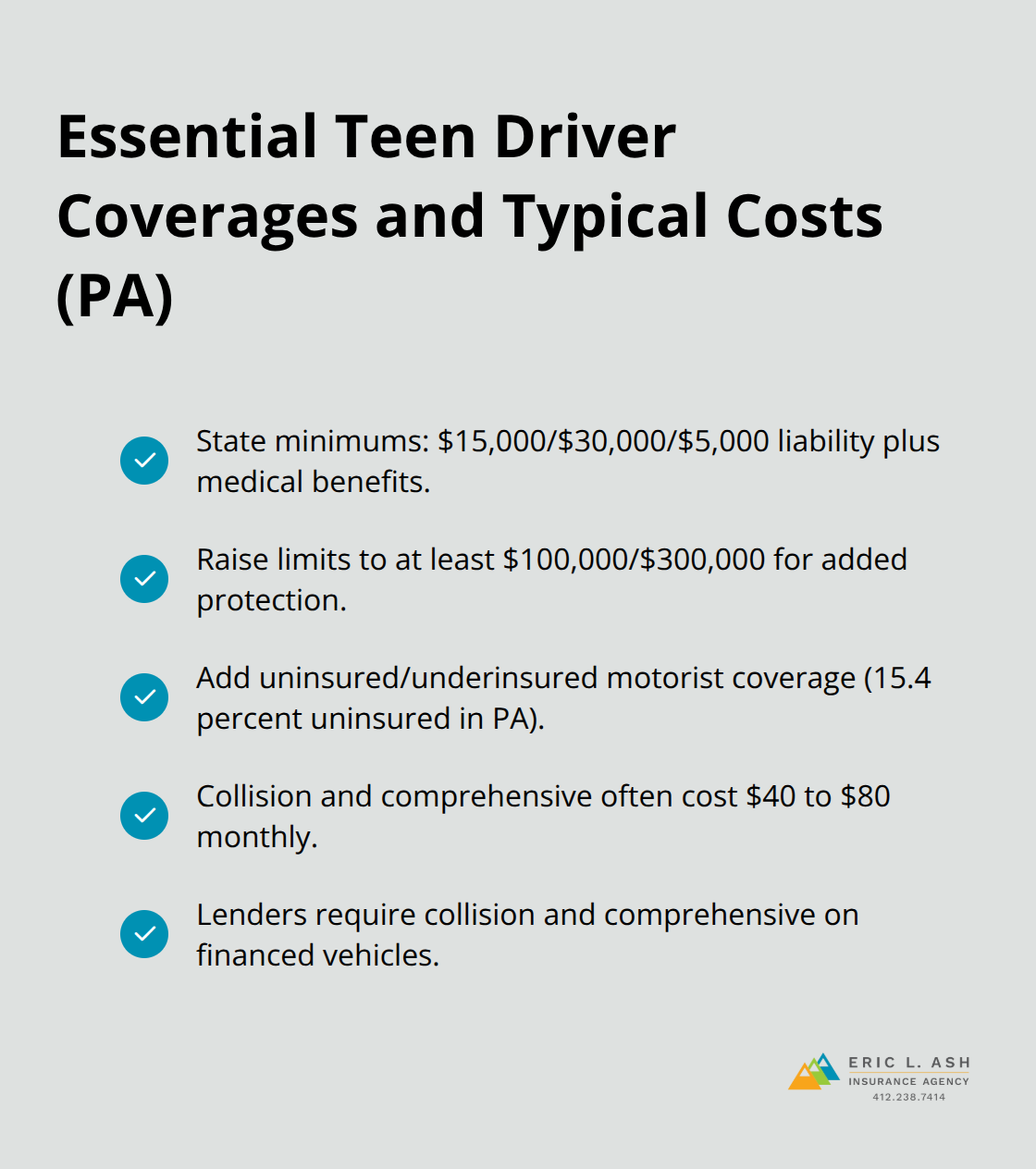

Pennsylvania mandates a minimum of $15,000 bodily injury liability per person, $30,000 per accident, and $5,000 property damage, plus medical benefits coverage. These minimums protect other people if your teen causes an accident, but they leave your teen’s own vehicle and medical costs unprotected. We at Eric L. Ash Insurance Agency strongly recommend increasing these minimums to at least $100,000 per person and $300,000 per accident, especially for teen drivers whose inexperience creates higher crash risk. The cost difference between state minimums and these higher limits runs roughly $10 to $20 monthly-a trivial amount compared to the financial exposure if your teen causes a serious accident.

Protecting Your Teen’s Vehicle with Collision and Comprehensive

Collision coverage pays to repair or replace your teen’s car after a crash with another vehicle, a pole, a pothole, or even an animal, and it applies regardless of who caused the damage. Comprehensive coverage handles non-collision damage like theft, vandalism, weather, and falling objects.

Together, these coverages cost around $40 to $80 monthly depending on your vehicle’s age and value, but they’re essential if your teen drives a car worth more than $5,000. If your teen financed the vehicle, the lender requires both collision and comprehensive, so you have no choice.

Addressing the Uninsured Driver Problem

Uninsured and underinsured motorist coverage protects your teen if hit by a driver who lacks insurance or insufficient coverage. Pennsylvania has 15.4 percent uninsured drivers on the road, making this coverage practically mandatory despite not being required by law. This protection covers medical expenses and vehicle damage when the at-fault driver cannot pay, which happens far more often than most families expect.

Maximizing Discounts That Stack Together

The good student discount typically requires a B average (3.0 GPA) and reduces premiums by 10% to 15%, saving $100 to $200 annually for a teen driver. Driver education course completion yields another 5% to 10% discount with most carriers, and these discounts stack. Telematics programs like Snapshot or Drive Safe and Save monitor actual driving behavior through a smartphone app or plug-in device, and safe drivers receive 10% to 30% discounts after 30 to 90 days of monitoring. These programs track hard braking, rapid acceleration, and nighttime driving, giving your teen real feedback on their habits.

Optimizing Your Teen’s Driver Status

Many families also qualify for discounts by designating the teen as an occasional driver, which costs less than making them the primary user of a vehicle. Shop annual quotes even after you’ve locked in a policy, because rate reductions accumulate over time and carriers adjust their teen driver pricing regularly. The strategies that work best combine multiple discounts with smart vehicle selection and monitoring-which brings us to the specific tactics that cut your premiums most effectively.

How to Stack Discounts and Cut Your Teen’s Premium in Half

Bundling Policies Delivers Immediate Savings

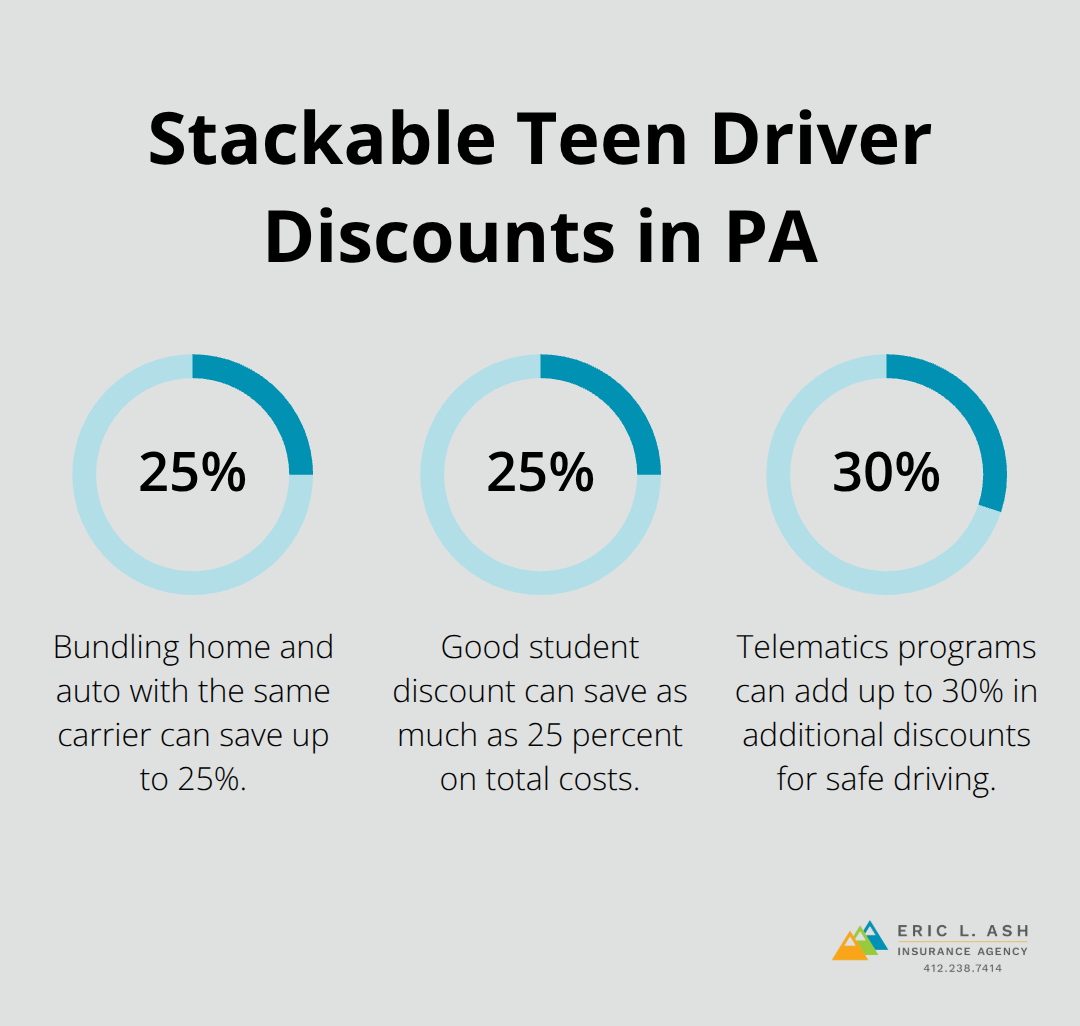

Bundling your home and auto policies remains one of the fastest ways to reduce what you pay for teen driver coverage. Most carriers offer 15% to 25% discounts when you insure your home and vehicles with the same company, which translates to $150 to $300 annually on a teen’s policy alone. The math works because insurers reward customer loyalty and reduce their administrative costs when handling multiple policies. State Farm, GEICO, and Erie all advertise bundling discounts prominently, but the actual savings vary by location and your current coverage.

Contact three carriers with your home and auto details to see which bundling discount applies to your specific situation, then compare the total household cost rather than just the teen’s premium. This approach often reveals that switching your entire household to a carrier offering a stronger bundling discount costs less than staying with your current insurer for auto only.

Good Student Discounts Require Minimal Effort

The good student discount deserves more attention than most parents give it because it requires only maintaining a 3.0 GPA or better, which many teens already achieve. This discount can save as much as 25 percent on total insurance costs and stacks directly on top of bundling discounts and other savings. Provide your insurer with a copy of the most recent report card or transcript when adding your teen to the policy, then update it annually since carriers audit these discounts.

Driver education course completion adds another 5% to 10% discount with most Pennsylvania carriers. Complete a reputable course before your teen obtains their license to apply this discount immediately when you add them to your policy.

Telematics Programs Track Real Driving Behavior

Telematics programs like Snapshot, Drive Safe and Save, or similar apps offered by your carrier monitor actual driving behavior for 30 to 90 days, then reward safe drivers with 10% to 30% additional discounts based on real data. These programs track hard braking, rapid acceleration, and nighttime driving patterns, giving your teen concrete feedback on risky habits while you capture measurable savings.

The combination of bundling, good student discount, driver education, and telematics can reduce your teen’s premium by 40% to 50% compared to a standalone policy with no discounts. This difference translates to $750 annually instead of $1,500, making the effort to stack these discounts worthwhile for your family’s budget.

Final Thoughts

Finding affordable teen driver coverage PA requires combining multiple strategies rather than relying on a single tactic. Start by gathering your teen’s driver’s license, current driving record, and school transcripts showing their GPA, then contact at least three insurers to obtain quotes that reflect bundling discounts, good student savings, and driver education completion. Compare the total household cost rather than just the teen’s premium, since bundling your home and auto policies often produces the largest savings, and request quotes for both adding your teen to your existing policy and purchasing a separate teen policy.

Once you’ve selected a carrier, enroll your teen in their telematics program immediately after the policy starts (this monitoring typically runs 30 to 90 days and generates additional discounts based on actual driving behavior). Review your policy annually to confirm all discounts remain applied and to shop rates again, since carriers adjust teen pricing regularly and small rate reductions compound over time. The combination of stacking discounts, selecting an appropriate vehicle, and shopping multiple carriers can reduce your annual costs by 40 to 50 percent compared to a standalone policy without discounts.

We at Eric L. Ash Insurance Agency help Pennsylvania families navigate these decisions by shopping multiple markets and identifying the coverage and discounts that fit your budget and risk profile. Contact us today to discuss your teen driver coverage options and receive personalized quotes tailored to your family’s situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.