Business Auto Insurance Quotes: Finding Your Best Rate

Getting business auto insurance quotes shouldn’t feel overwhelming. The rates you receive depend on several factors-from your vehicle type to your driving history-and understanding these elements helps you find coverage that actually fits your budget.

At Eric L. Ash Insurance Agency, we’ve helped Pennsylvania business owners navigate this process countless times. This guide walks you through what affects your rates, how to compare quotes effectively, and the mistakes that cost businesses money.

What Really Drives Your Business Auto Insurance Rates

Vehicle Type Creates Major Cost Differences

Your vehicle type matters far more than most Pennsylvania business owners realize. A food truck costs 20–30% more to insure than a standard company car because of specialized equipment and higher loss exposure. Construction vehicles like pickup trucks and cargo vans also command higher premiums than sedans due to increased accident risk and the value of tools transported. A contractor operating multiple vehicles pays substantially more than a consulting firm with one car, not because of arbitrary pricing but because fleet size multiplies exposure.

How You Use Your Vehicle Affects Your Rate

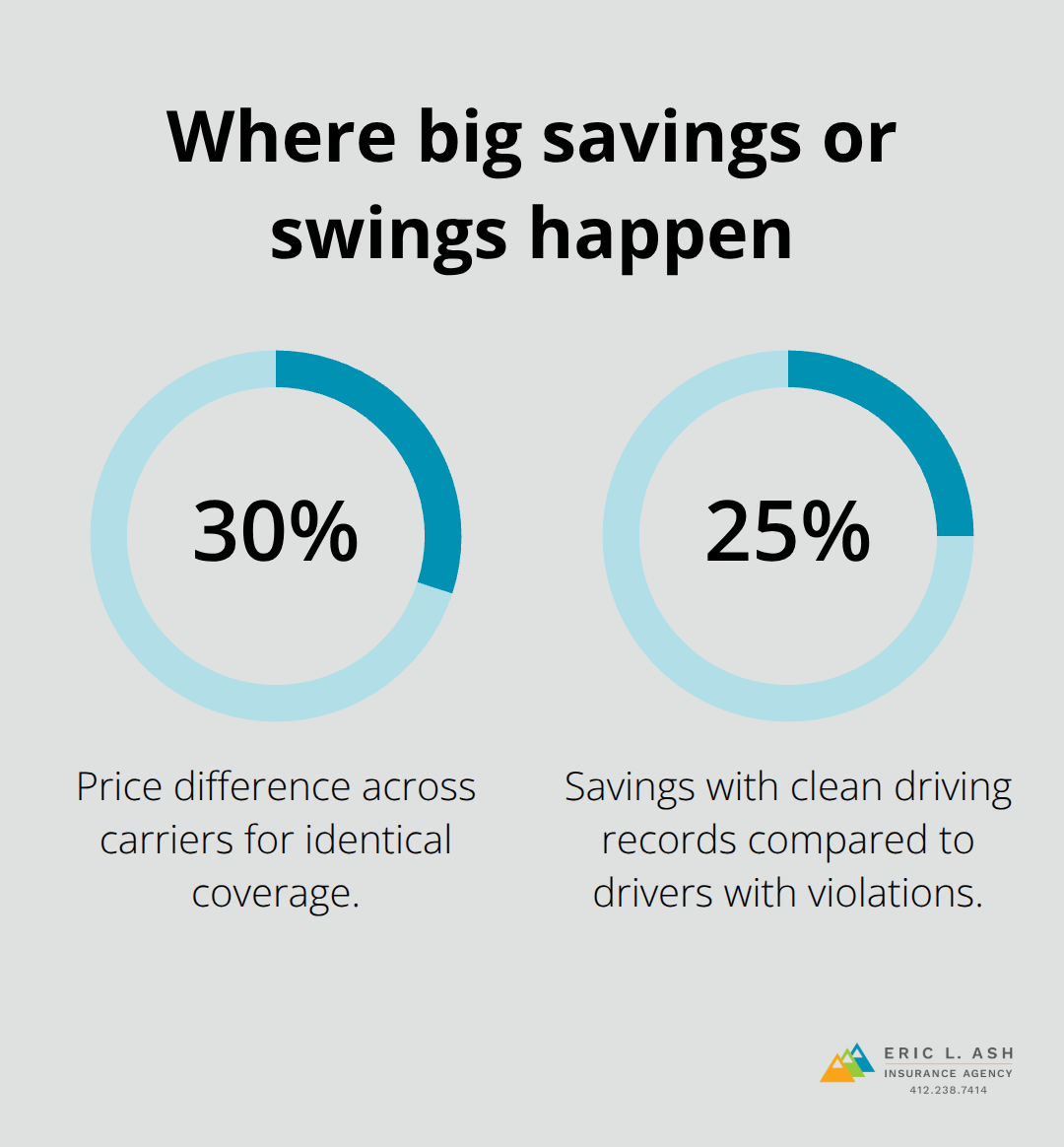

The way you use your vehicle matters just as much as what you drive. Local delivery within 100 miles of your base typically costs 10–15% less than long-haul or interstate travel. Your insurance company runs motor vehicle reports on all drivers listed on the policy, and this is where many Pennsylvania business owners see rate surprises. Clean driving records can save up to 25% compared to drivers with violations or accidents in the past three years.

Driver History Impacts Your Entire Fleet

A single at-fault accident can increase your premium significantly, which is why fleet safety directly impacts your bottom line. If your team has multiple drivers, one person’s poor record can raise rates across your entire policy. This reality means that investing in driver training and safety programs pays dividends through lower premiums over time.

Coverage limits and deductibles Shape Your Final Cost

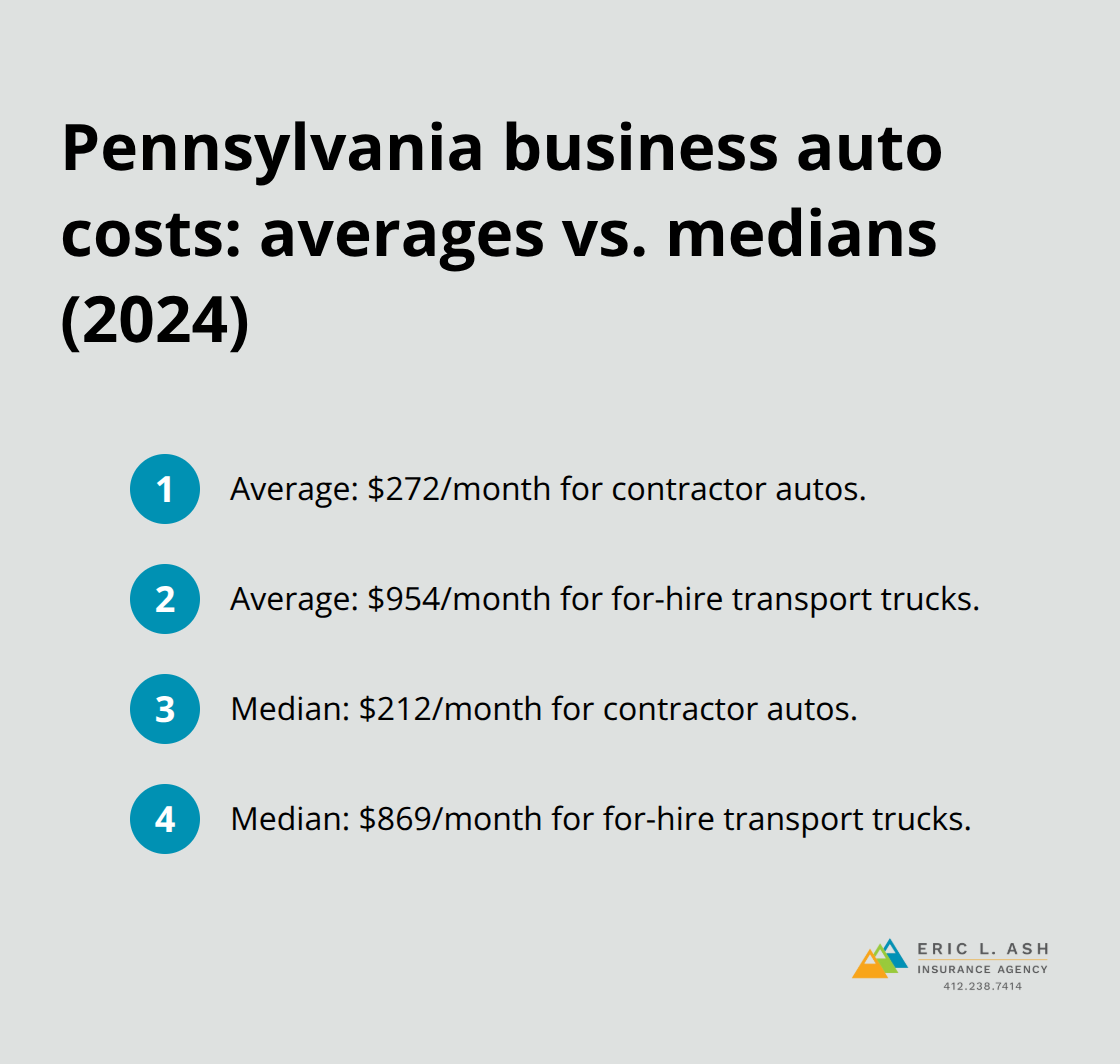

The coverage limits and deductibles you choose create the final piece of your rate puzzle. Moving from Pennsylvania’s state minimum liability limits of 15/30/5 to higher limits like 100/300/100 or 1,000,000 combined single limit substantially increases your premium, but inadequate limits expose your business to catastrophic out-of-pocket costs. Increasing your collision or comprehensive deductible from $500 to $1,000 typically reduces premiums by 10–20%, though you’ll pay more if you file a claim. Progressive reports that 2024 average monthly costs for Pennsylvania business auto insurance range from $272 for contractor autos to $954 for for-hire transport trucks, depending on these exact factors. The median costs are lower-$212 for contractors and $869 for transport trucks-which shows how much individual circumstances vary.

Your specific rate depends entirely on what vehicles you insure, who drives them, and what protection level you select. Understanding these rate drivers positions you to make smarter decisions when you start comparing quotes from different carriers.

How to Compare Business Auto Insurance Quotes Effectively

Gather Quotes from Multiple Carriers

Getting three or more quotes is non-negotiable if you want competitive rates. Differences of up to 30% can occur for identical coverage across carriers, which means skipping this step costs real money. Start by gathering quotes from at least three different insurers, and make sure each quote includes the same vehicle information, driver details, coverage limits, and deductibles. This apples-to-apples comparison prevents the frustration of comparing fundamentally different policies.

Many Pennsylvania business owners think they can judge rates by looking at a single number, but that number only matters when the underlying coverage matches. One carrier might quote you $400 monthly with a $1,000 deductible and 100/300/100 liability limits, while another quotes $350 with a $2,500 deductible and 15/30/5 limits. The cheaper option leaves your business exposed to massive out-of-pocket costs after an accident.

When you request quotes, provide exact information about how many miles your vehicles travel annually, whether drivers operate locally or regionally, and what goods or equipment they transport. Vague information produces vague quotes that won’t reflect your actual cost. Your actual rate depends entirely on what you’re comparing.

Review Coverage Options Side by Side

Once you have multiple quotes in hand, examine the specific coverages each carrier includes. Look at liability limits, physical damage protection, uninsured motorist coverage, and any specialty add-ons like garage keepers liability or motor truck cargo coverage. Different carriers structure these coverages differently, and what one insurer includes as standard another might offer only as an optional add-on.

Create a simple spreadsheet listing each carrier’s quote alongside their coverage details. This visual comparison makes it far easier to spot which carrier offers the best value for your specific needs. A lower premium with inadequate coverage creates false savings that vanish the moment you file a claim.

Ask About Available Discounts

Ask each insurer about their available discounts before finalizing your decision, because discounts can meaningfully reduce your final premium. Bundling commercial auto with property coverage typically saves money on your auto premium, while paying your policy in full can yield a discount. Some carriers offer prior auto insurance discounts or multi-product discounts that others don’t advertise prominently.

Don’t ask about discounts in passing; specifically request a list of every discount you qualify for and ask the representative to apply them to your quote. The difference between a quote with no discounts and one with three or four discounts can be substantial. If you operate a fleet with clean driving records across your team, mention this fact explicitly because some carriers offer accident-free discounts that require you to state your qualifications.

Your job is to make the insurer’s job easier by providing complete, accurate information upfront so they can quote you accurately and show you every savings opportunity available. We can assist you with assessing your insurance needs and leverage relationships with dozens of carriers to shop multiple markets and deliver competitive rates tailored to your specific business needs. This approach means you gain access to carriers and discounts you might not find on your own.

The mistakes you make during the quoting process often cost far more than any single rate difference, which is why the next section focuses on the decisions that drain your budget.

Common Mistakes That Cost Pennsylvania Business Owners Money

Price Alone Never Tells the Real Story

The biggest mistake Pennsylvania business owners make is treating price as the only decision factor. A quote that’s $100 monthly cheaper looks attractive until you file a claim and realize your coverage limits are inadequate or critical protections are missing. One business owner chose a policy based solely on the lowest premium, only to discover after an accident that their liability limits were state minimum liability limits in Pennsylvania, meaning they paid tens of thousands out of pocket for injuries exceeding those thresholds. That decision cost far more than the premium savings ever provided.

Your quote comparison should prioritize value, not just the monthly number. A policy costing $50 more monthly but with proper limits and comprehensive coverage protects your business far better than cutting corners on protection to save money. Progressive’s 2024 data shows average monthly costs ranging from $272 for contractor autos to $954 for transport trucks, but these averages obscure the reality that your actual cost depends entirely on the coverage you select. Choosing inadequate limits to hit a lower price point transforms insurance from protection into a liability.

Outdated Information Creates Coverage Gaps

Another critical error is failing to update your policy information when your business changes. If you add a new vehicle, hire additional drivers, expand your service radius from local to regional, or change how you use your fleet, your existing quote becomes obsolete. Many Pennsylvania business owners keep policies unchanged for years even though their operations have evolved significantly.

Insurance companies base rates on the information you provide at quote time, so outdated details mean you’re either overpaying for coverage you don’t need or underpaying and facing premium adjustments later. A company that started with one delivery vehicle and now operates five needs different coverage than their original policy provided. Skipping this review leaves your business exposed and your rates misaligned with your actual risk.

Annual Reviews Prevent Rate Misalignment

Schedule a policy review conversation at least annually to ensure your coverage evolves with your business needs. During these reviews, examine whether your coverage limits still match your business exposure, whether your deductibles align with your financial capacity, and whether you qualify for new discounts. This simple practice catches gaps before they create problems and identifies savings opportunities you may have missed.

Final Thoughts

Finding competitive business auto insurance quotes comes down to understanding what drives your rates, comparing coverage systematically, and avoiding shortcuts that expose your business to unnecessary risk. The vehicle you drive, who operates it, and the protection level you select determine your final cost far more than any single carrier’s pricing strategy. Pennsylvania business owners who invest time in gathering multiple quotes and reviewing coverage details consistently find better rates than those who accept the first offer they receive.

Collect quotes from at least three carriers using identical vehicle information, driver details, and coverage specifications. Create a simple spreadsheet comparing premiums alongside coverage options, then ask each insurer about every discount you qualify for. This process takes a few hours but typically saves hundreds of dollars annually, and once you’ve selected a policy, mark your calendar for an annual review to verify your coverage still matches your business operations.

An independent agent transforms this process from frustrating to manageable by leveraging relationships with multiple carriers to shop business auto insurance quotes on your behalf. Contact Eric L. Ash Insurance Agency to discuss your business auto insurance needs and discover how much you could save with responsive, local service backed by the market access that independent agencies provide.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.