Teenage Driver Car Insurance: A Practical Guide for Parents

Getting your teenager behind the wheel is a major milestone. It’s also when your insurance costs jump significantly and your coverage needs shift dramatically.

We at Eric L. Ash Insurance Agency know that teenage driver car insurance requires a different approach than standard policies. This guide walks you through the coverage options, cost-saving strategies, and practical steps to protect your family while keeping premiums manageable.

Why Teen Drivers Cost More to Insure

The Real Risk Behind Higher Premiums

Teen drivers represent a genuine insurance risk that justifies higher premiums. The CDC reports that drivers aged 16–19 are three times more likely to be in a fatal crash than drivers 20 and older. This isn’t theoretical risk-it translates directly into claim data that insurers use to set rates. When you add a 16-year-old to your policy, you’re adding someone whose crash rate is significantly higher than older drivers.

According to Investopedia, adding a teenage driver to your insurance policy typically costs about $250 per month on average. For a typical middle-aged adult paying around $726 for a six-month policy, adding a teen brings that six-month total to approximately $1,848. The national average annual premium for a 16-year-old is about $5,744, though this varies significantly by state, vehicle type, and driving record.

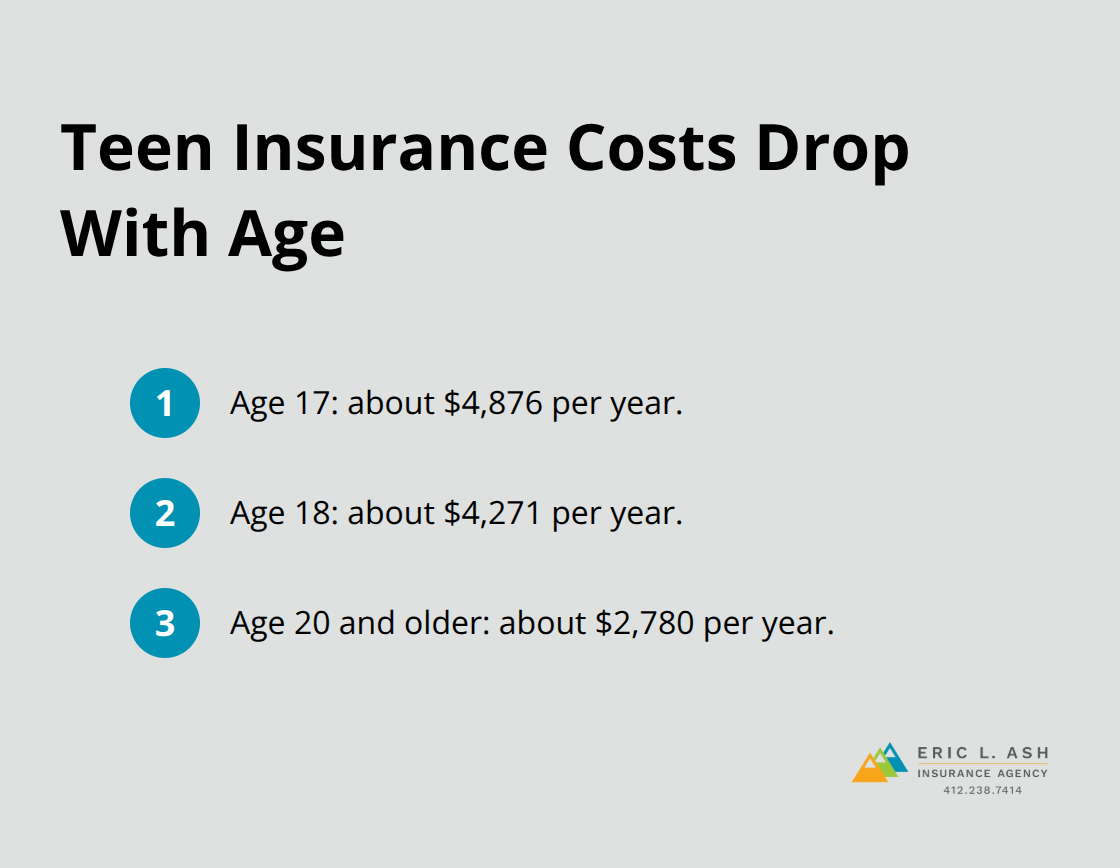

How Premiums Drop as Teens Age

Age matters significantly when it comes to insurance costs. A 17-year-old averages about $4,876 annually, while an 18-year-old drops to $4,271. The good news is that premiums decline sharply after age 20, falling to about $2,780 annually according to The Zebra’s rate data.

This decline reflects the reduced crash risk that comes with driving experience and maturity.

Standard Policies Leave Critical Coverage Gaps

Standard auto insurance policies written for adults often lack the protections teen drivers need. A basic liability-only policy covers damage your teen causes to others, but it doesn’t protect your family if your teen is hit by an uninsured driver or needs medical care after an accident. Collision and comprehensive coverage are optional on adult policies but become critical when a teen is driving.

Collision covers accidents with other vehicles or objects, while comprehensive handles theft, weather, and vandalism. Medical payments coverage fills another gap-it covers medical expenses for anyone injured in your teen’s vehicle, regardless of fault. Optional add-ons like roadside assistance become more valuable when a young driver is on the road (flat tires and dead batteries happen more often with inexperienced drivers).

Pennsylvania’s Minimum Coverage Isn’t Enough

The Insurance Institute for Highway Safety emphasizes that coverage decisions should account for the teen’s specific risk profile, vehicle type, and your family’s financial situation. Pennsylvania requires minimum liability coverage, but those minimums are often too low to protect your assets if your teen causes a serious accident. A serious crash can result in medical bills, property damage, and legal judgments that far exceed state minimums.

Reviewing your current policy limits and adding appropriate coverage layers before your teen starts driving prevents discovering gaps after an incident occurs. This proactive approach protects both your teen and your family’s financial security. Understanding what each coverage type actually does helps you make informed decisions about which protections matter most for your situation.

How to Cut Your Teen Driver Insurance Costs

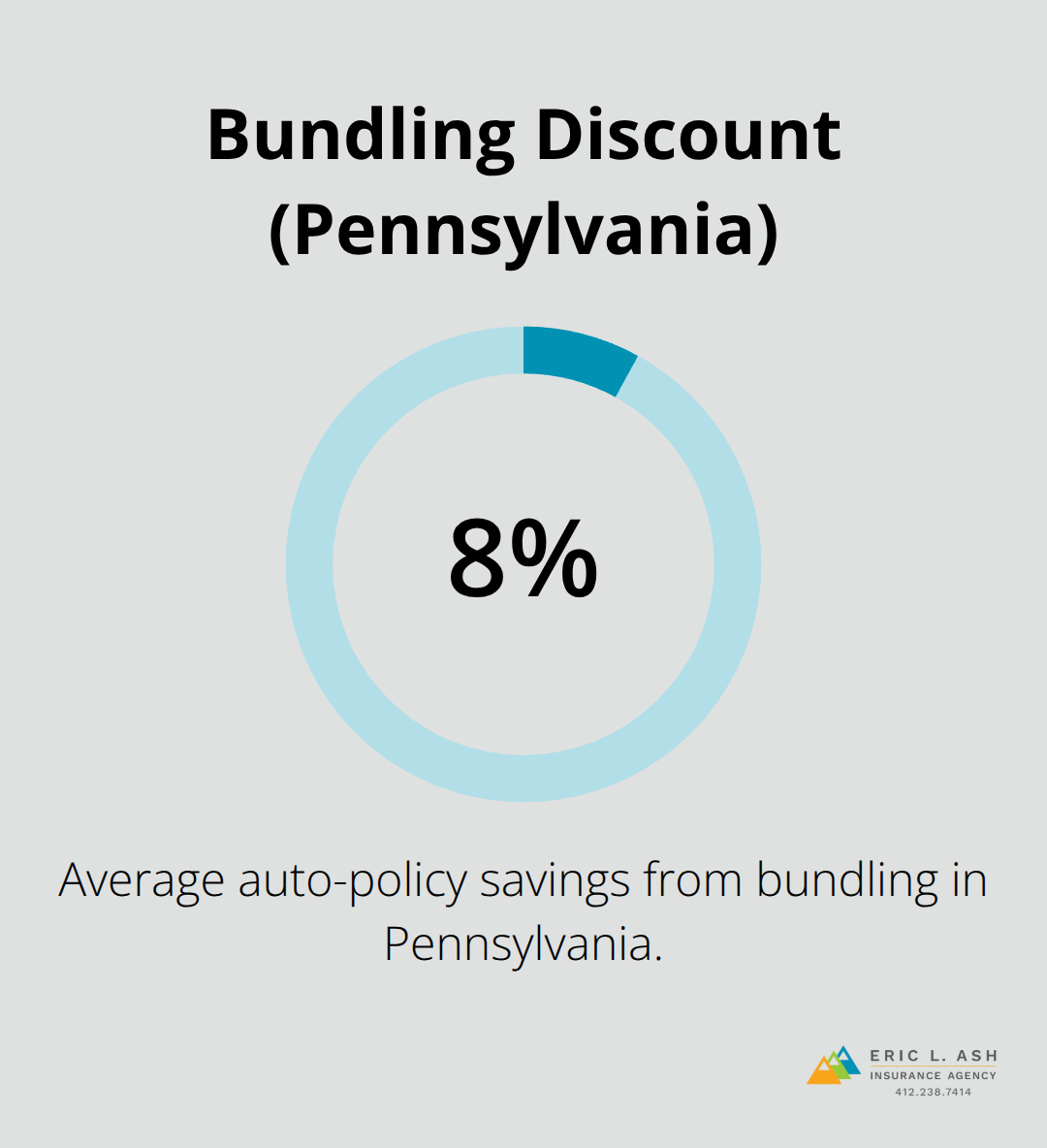

Bundle Your Auto and Home Policies for Immediate Savings

Bundling your teen’s auto coverage with your homeowners or renters policy delivers immediate savings that most families leave on the table. In Pennsylvania, bundling typically yields about 8% in savings on your auto policy alone, or roughly $460 on a $5,744 baseline annual premium for a 16-year-old. Getting a quote that includes both policies should be your first move before your teen starts driving.

Many families assume they’re already getting the best rate, but the math proves otherwise-bundling is one of the most straightforward ways to offset the cost increase a teen driver creates.

Good Grades Translate to Real Discounts

A B average or better qualifies your teen for a good student discount that averages about $283 in annual savings. This isn’t a token discount-it’s a meaningful reduction that recognizes responsible behavior outside the car. Most insurers require transcripts submitted twice yearly, so you’ll need to stay on top of documentation, but the savings justify the effort. Some carriers also offer additional discounts if your teen completes a defensive driving course, which stacks on top of the good grades discount. The combination of maintaining strong academics and taking a driver education course adds up to several hundred dollars in annual savings.

Telematics Programs Reward Safe Driving Behavior

Telematics programs track real driving behavior and reward safe drivers with discounts. These devices plug into your teen’s car and monitor speed, acceleration, braking, and time of day driven. Your teen sees exactly how their driving affects insurance costs, which creates genuine incentive to drive safely. This approach transforms insurance from a punishment for being a teen into a tool that rewards safety.

Vehicle Selection Has a Bigger Impact Than You Think

Buying your teen an older, safer car costs significantly less to insure than a newer performance vehicle. The largest year-over-year insurance decreases typically occur with 7- to 8-year-old models. These represent meaningful savings compared to high-performance or luxury vehicles that can double insurance costs. Avoid sports cars, high-horsepower models, and anything with luxury badging. Instead, prioritize reliability and safety ratings over style or performance. An economy sedan or practical hatchback from a reliable manufacturer gives your teen dependable transportation while keeping your insurance costs manageable.

Understanding Coverage Gaps Protects Your Family

Standard auto insurance policies written for adults often lack the protections teen drivers need. A basic liability-only policy covers damage your teen causes to others, but it doesn’t protect your family if your teen is hit by an uninsured driver or needs medical care after an accident. Collision and comprehensive coverage are optional on adult policies but become critical when a teen is driving. Medical payments coverage fills another gap-it covers medical expenses for anyone injured in your teen’s vehicle, regardless of fault. Optional add-ons like roadside assistance become more valuable when a young driver is on the road. Reviewing your current policy limits and adding appropriate coverage layers before your teen starts driving prevents discovering gaps after an incident occurs.

What Coverage Actually Protects Your Teen Driver

Liability Coverage: The Foundation That Isn’t Enough

Pennsylvania requires minimum liability coverage, but those minimums leave your family dangerously exposed. The state minimum of $15,000/$30,000 covers $15,000 per person and $30,000 per accident. A single injured person’s medical bills can reach $50,000 or more, and you become personally responsible for anything above your coverage limit. Most financial advisors recommend at least 100/300/100 coverage for families with teenage drivers, which costs only marginally more but protects your assets substantially better. The Insurance Institute for Highway Safety emphasizes that coverage decisions should account for the teen’s specific risk profile and your family’s financial situation, not just state minimums.

Liability coverage pays for damage your teen causes to other people and their property. This protection matters because a serious accident involving another vehicle, injuries, or property damage can easily exceed state minimums. Your personal assets face seizure if a judgment exceeds your policy limits, which makes adequate liability coverage a financial necessity rather than an optional upgrade.

Collision and Comprehensive: Protecting Your Teen’s Vehicle

Collision and comprehensive coverage protect your teen’s vehicle rather than liability to others. Collision covers damage from accidents with other vehicles or objects, while comprehensive handles theft, weather damage, and vandalism. These coverages become non-negotiable when a teen drives because inexperienced drivers have higher accident rates. If your teen’s car is financed or leased, your lender requires these coverages anyway.

Even if the car is paid off, skipping collision and comprehensive on a teen’s vehicle means paying out-of-pocket for repairs that could easily exceed the vehicle’s value. A single accident can total a vehicle, and without collision coverage, you absorb the entire cost. Comprehensive coverage protects against losses you can’t control, like hail damage or theft, which happen frequently in Pennsylvania.

Uninsured and Underinsured Motorist Protection

Uninsured and underinsured motorist protection covers your family if another driver causes an accident but lacks adequate insurance. This protection matters because many Pennsylvania drivers carry only minimum liability coverage or drive without insurance entirely. Your teen could suffer serious injuries through no fault of their own and face inadequate compensation from the at-fault driver’s policy. This coverage steps in to cover medical expenses, lost wages, and pain and suffering that the other driver’s insurance won’t pay.

Medical Payments and Roadside Assistance

Medical payments coverage pays for medical expenses for anyone injured in your teen’s vehicle regardless of fault. This protection covers hospital bills, doctor visits, and rehabilitation costs that your health insurance might not fully cover. The coverage applies to your teen, passengers, and even pedestrians struck by your teen’s vehicle. Optional roadside assistance becomes genuinely valuable with a teen driver since flat tires, dead batteries, and lockouts occur more frequently with inexperienced drivers. A stranded teen on the side of the road at night creates safety concerns that roadside assistance resolves quickly.

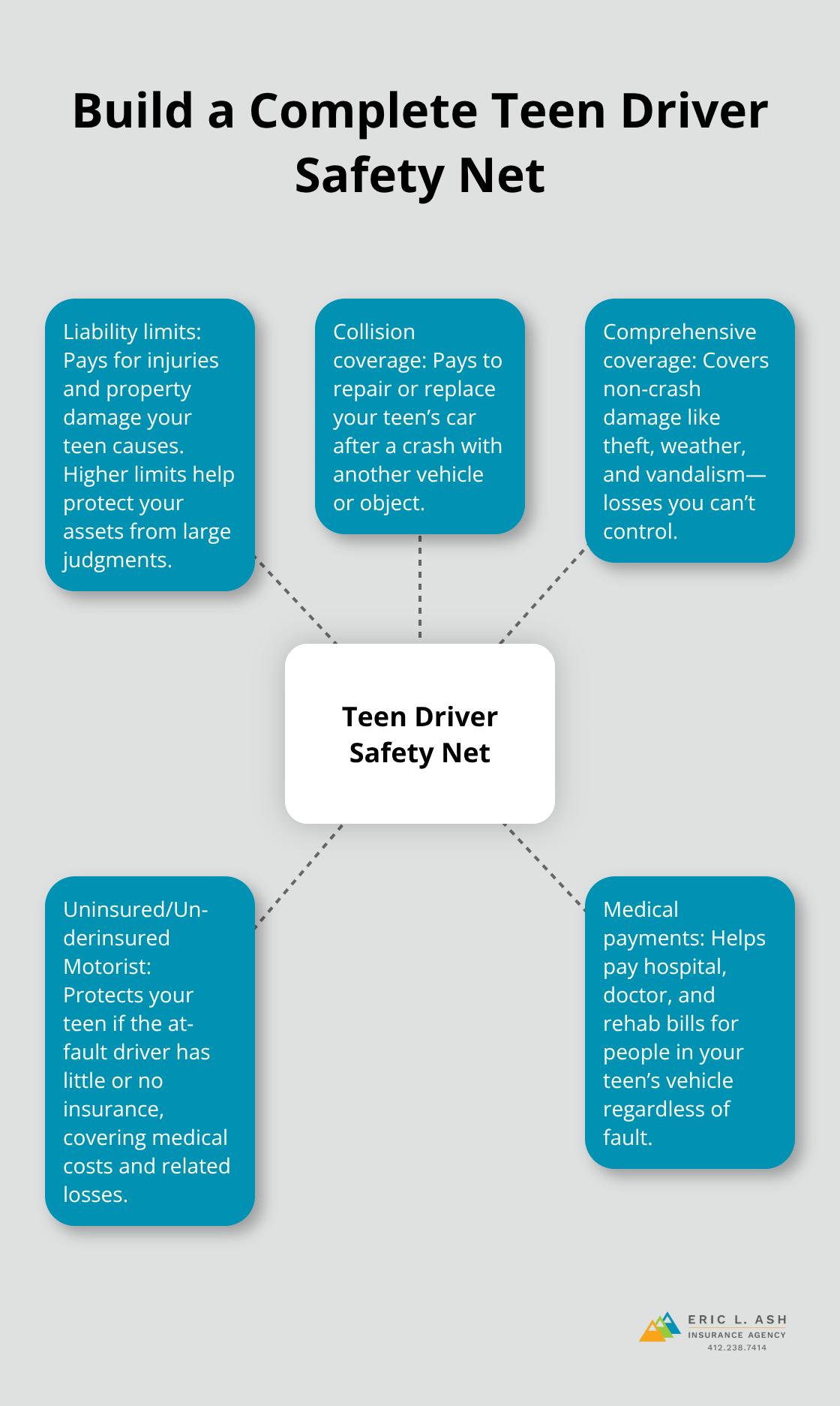

Building a Complete Safety Net

The combination of adequate liability limits, collision, comprehensive, uninsured motorist protection, and medical payments coverage creates a complete safety net that standard policies simply don’t provide. Each coverage type addresses a specific gap that leaves families vulnerable. Reviewing your current policy limits and adding appropriate coverage layers before your teen starts driving prevents discovering gaps after an incident occurs.

This proactive approach protects both your teen and your family’s financial security.

Final Thoughts

Teenage driver car insurance requires you to balance protection with affordability, and the strategies outlined in this guide work best when combined rather than used individually. Start by bundling your auto and home policies, which delivers immediate savings of roughly $460 annually on a teen’s coverage. Layer in good student discounts, telematics programs, and smart vehicle selection to reduce costs further, and these steps compound to create meaningful financial relief while strengthening your family’s protection.

The coverage decisions you make before your teen starts driving determine whether you’re adequately protected or dangerously exposed. Pennsylvania’s minimum liability limits leave your family vulnerable to judgments that exceed your coverage, making higher limits a financial necessity rather than an upgrade. Adding collision, comprehensive, uninsured motorist protection, and medical payments coverage creates the safety net that standard policies simply don’t provide, and each coverage type addresses a specific gap that could otherwise cost your family thousands of dollars.

Your teen’s driving record, vehicle choice, and academic performance all influence insurance costs, giving you concrete levers to control expenses. An independent insurance agent transforms the shopping process from overwhelming to manageable by shopping multiple carriers simultaneously rather than forcing you to contact each company individually. Contact Eric L. Ash Insurance Agency to get quotes that compare your options and identify savings you’re currently leaving on the table.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.