Airbnb Rental Insurance: Protecting Your Short-Term Space

Your standard homeowners policy won’t cover your Airbnb income or protect you from guest-related accidents. That gap leaves you exposed to serious financial risk.

At Eric L. Ash Insurance Agency, we see hosts discover this problem too late. Airbnb rental insurance fills those gaps with coverage designed specifically for short-term rental operators.

Why Your Homeowners Policy Leaves You Exposed

Standard homeowners policies were written for owner-occupied homes, not businesses. The moment you list your property on Airbnb, you’ve crossed into commercial activity that most traditional policies explicitly exclude. Insurance companies know the difference between a family living in a home and a host running a vacation rental operation with constant guest turnover, and they price accordingly-or they don’t cover you at all.

Most homeowners policies contain a business exclusion clause that voids coverage for income-generating rental activity. This isn’t a gray area or a technicality. If you file a claim related to your Airbnb operation and your insurer discovers you were running a short-term rental, they can deny the entire claim. You lose not just the coverage you thought you had, but also the premium you’ve been paying.

The Income Problem Nobody Talks About

Your homeowners policy will not reimburse you for lost rental income. If a fire damages your property and you can’t accept guests for three months, your policy covers the structure and contents-but not the income you had to forgo. Short-term rental hosts depend on that income as a primary revenue stream for many properties.

A covered loss that makes your property uninhabitable means zero income during recovery, and your homeowners policy won’t replace a single dollar of that lost revenue. This gap forces many hosts to choose between reconstruction costs and survival, and it’s entirely preventable with the right coverage.

Liability Exposure Extends Beyond Your Walls

Standard homeowners liability coverage typically maxes out at $300,000 to $500,000 and assumes a family household, not a business with dozens of rotating guests annually. When a guest is injured on your property or claims damage from something they brought with them, the liability exposure multiplies.

A guest who slips on your deck and breaks their leg, a guest whose friend is injured using your hot tub, or a guest who causes property damage at a neighboring property while using your kayak-all of these scenarios create liability that extends far beyond what homeowners insurance contemplates. Airbnb’s Host Protection Insurance provides up to $1 million per occurrence for liability, but it has critical exclusions. It does not cover mold, pollution, certain water damage, or property damage to your own rental. Host Protection also does not cover lost income.

Relying solely on Airbnb’s program leaves significant gaps, particularly around property damage claims and business interruption. Your homeowners policy won’t fill those gaps because the business exclusion clause already removes your commercial operation from coverage entirely. This combination of gaps-income loss, property damage, and extended liability-is exactly what specialized Airbnb rental insurance addresses.

What Airbnb Rental Insurance Covers

Property Damage from Guests

Specialized Airbnb rental insurance replaces the gaps left by your homeowners policy with coverage designed for the realities of short-term hosting. Unlike traditional policies that exclude your rental operation entirely, these policies acknowledge that you run a business and build protection around the specific risks that come with it.

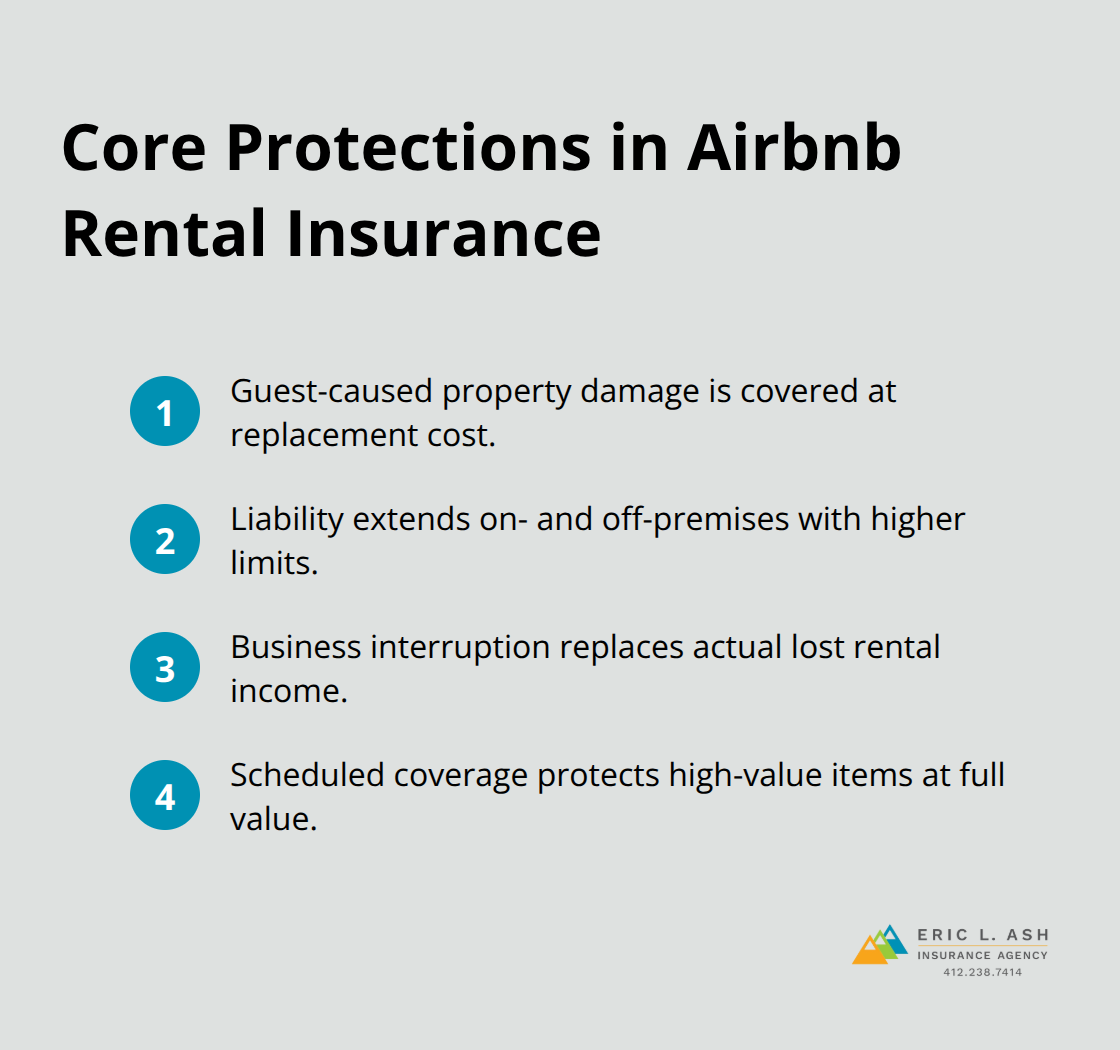

Property damage from guests tops the list. When a guest damages your furniture, breaks appliances, or causes structural damage, your homeowners policy won’t pay because the business exclusion clause already removed you from coverage. Airbnb rental insurance covers guest-caused damage to your building and contents using replacement cost valuation, which means you receive payment for what it costs to replace items new, not what they’re worth after depreciation.

Proper Insurance covers all-risk building and contents with no sub-limits on theft, vandalism, or water damage. This matters because a single incident involving intentional guest destruction or water damage could easily exceed $10,000, and you need coverage that doesn’t cap payouts for specific claim types.

Host Liability for Guest Injuries

Host liability for guest injuries represents your second major exposure, and it’s where platform protection falls dangerously short. While sites like Airbnb do offer some property protection for hosts against damage by a guest, it does not include liability insurance. Airbnb’s Host Protection Insurance caps liability at $1 million per occurrence, but it explicitly excludes mold, pollution, and certain water damage claims.

Real Airbnb rental insurance extends liability coverage to incidents both on and off your property. If a guest suffers injury using your kayak three miles away at a local lake, that coverage applies. If a guest experiences a bed bug infestation and files a liability claim, that coverage applies too, including extermination costs and lost revenue from canceled bookings. Commercial General Liability in specialized policies starts at $1 million per occurrence with options up to $2 million, addressing the expanded exposure that comes with rotating guests.

Business Interruption Coverage

The third critical piece is business interruption coverage, which homeowners insurance explicitly won’t provide. If a covered event like fire or water damage makes your property uninhabitable, this coverage reimburses your actual lost rental income with no time limit on payouts.

For hosts earning $2,000 to $5,000 monthly from their property, three months of lost income while repairs happen represents $6,000 to $15,000 in unrecovered revenue. Specialized policies cover this gap entirely, protecting your cash flow when you need it most.

Scheduled Coverage for High-Value Items

High-value items deserve scheduled coverage. If you furnish your rental with expensive artwork, electronics, or designer pieces, standard coverage often applies sub-limits that leave you underprotected. Adding scheduled personal property coverage to your Airbnb rental insurance means each valuable item gets listed individually with its full replacement cost guaranteed, eliminating depreciation calculations and sub-limit surprises when you file a claim.

When you understand what specialized coverage actually protects, the next step involves comparing specific policies and providers to find the right fit for your property’s unique characteristics and occupancy patterns.

Selecting the Right Coverage for Your Rental Property

Calculate Your True Replacement Cost and Occupancy Rate

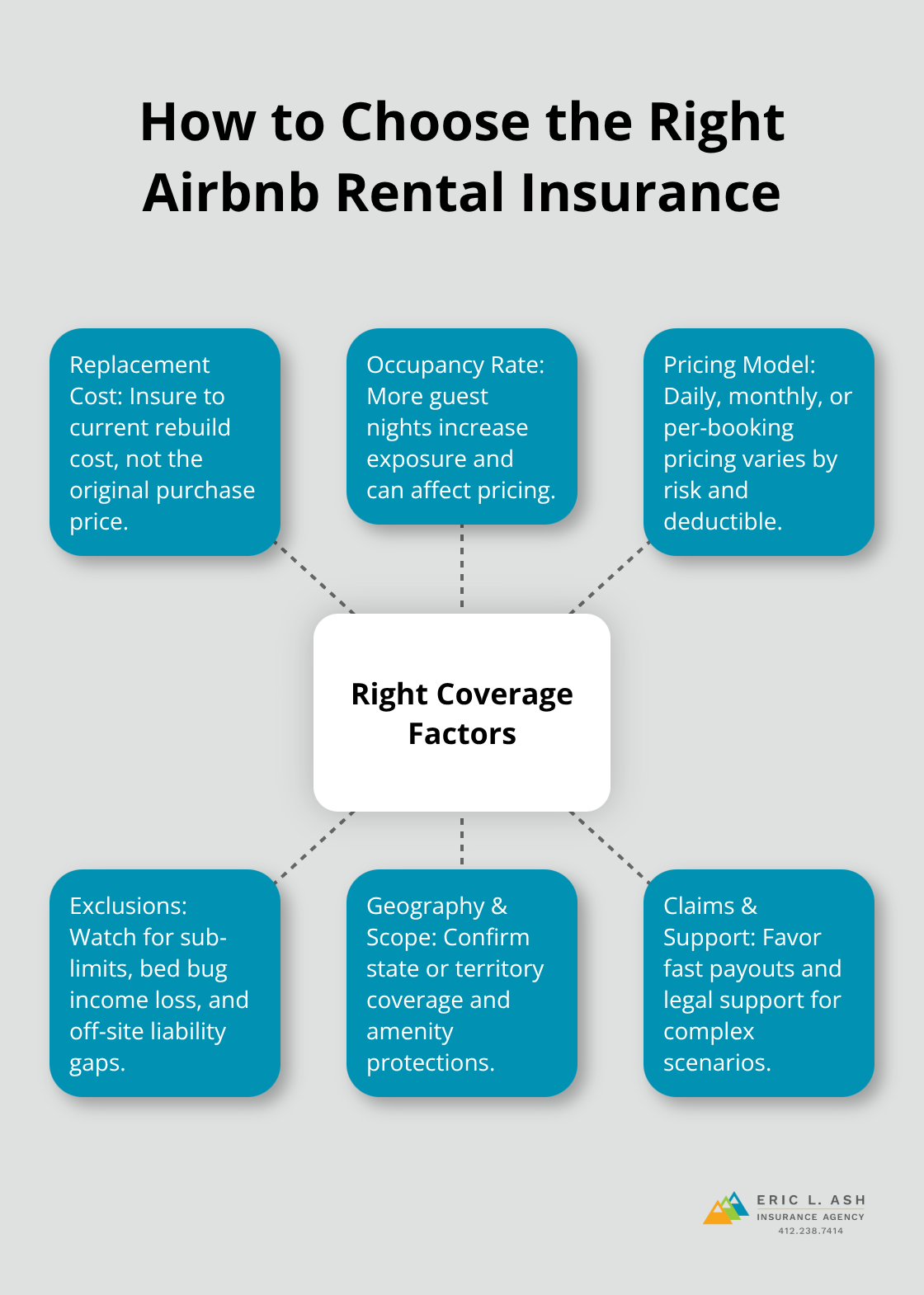

Start with your actual replacement cost, not your purchase price. Many hosts underestimate what it would cost to rebuild their property today, which leads to insufficient coverage limits. If your rental cost $300,000 to purchase but would cost $450,000 to rebuild with current labor and material prices, your coverage limit should reflect the higher figure.

Occupancy patterns matter equally. A property that hosts guests 200 nights annually faces different risk exposure than one occupied 100 nights yearly. Properties with higher turnover see more guest-caused damage, theft, and liability incidents. When you request quotes, provide accurate occupancy data because insurers price based on exposure frequency.

Compare Pricing Across Multiple Providers

CBIZ Vacation Rental Insurance and Safely both tailor quotes to specific occupancy rates. CBIZ reports plans ranging from about $3 per day to roughly $100 per month depending on property characteristics. Safely offers customized pricing based on stay length, number of properties, occupancy, and deductible selection, with 98% of claims paid within 4 to 5 days. This speed matters when you need cash flow restored quickly after a loss.

Proper Insurance covers all 50 states plus Washington, D.C., and includes squatter protection with legal support and lost revenue coverage if a guest refuses to vacate, plus bed bug and flea protection covering extermination costs and booking cancellations. Truvi offers global coverage outside travel-advisory countries with payouts in 3 to 5 days and pricing starting around £13.80 per booking.

Evaluate Coverage Details Beyond Premium Amounts

Compare what each provider actually covers rather than focusing solely on premium. CBIZ covers all 50 states plus Puerto Rico, Washington, D.C., and the U.S. Virgin Islands, with $2 million general liability and legal expense coverage for squatter situations. Allstate HostAdvantage provides guest-damaged personal property protection up to about $10,000 per rental period in select states.

The exclusions matter more than the coverage limits. Ask specifically whether the policy covers water damage without sub-limits, whether bed bug claims include lost revenue, and whether liability extends to guests using amenities off-site (kayaks, bikes, pools). These details separate adequate protection from policies with hidden gaps that emerge only when you file a claim.

Final Thoughts

Your standard homeowners policy excludes your rental operation entirely, and that exclusion removes coverage the moment you accept your first guest. Airbnb rental insurance fills this gap with replacement cost protection for guest-caused damage, liability coverage that extends beyond your property boundaries, and business interruption protection that replaces lost income during recovery. Providers like Proper Insurance, CBIZ, and Safely have built policies specifically around the operational realities of short-term hosting, including protections for bed bugs, squatters, and amenity-related incidents that traditional insurers either exclude or severely limit.

The right coverage depends on your specific property, occupancy rate, and the amenities you offer. Comparing quotes across multiple providers reveals significant differences in what you actually get for your premium-a policy that costs $50 monthly might exclude water damage sub-limits or cap bed bug coverage, while another at a similar price includes unlimited protection for those same risks. The details matter far more than the headline premium.

We at Eric L. Ash Insurance Agency work with hosts across Pennsylvania to find Airbnb rental insurance that matches their operations without leaving dangerous gaps. As an independent agency, we shop multiple carriers to deliver competitive rates and tailored protection backed by responsive local service. Contact us to review your current coverage and explore specialized options that actually protect your investment and income.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.