Teen Driver Insurance Pennsylvania: What Teens Need to Know

Teen drivers in Pennsylvania face some of the highest insurance premiums in the country. The good news is that there are concrete steps you can take right now to lower those costs and build safer driving habits.

We at Eric L. Ash Insurance Agency help families navigate teen driver insurance Pennsylvania options every day. This guide walks you through exactly what affects your rates and how to reduce them.

What Your Teen’s Pennsylvania Insurance Premium Actually Costs

Pennsylvania teen drivers pay significantly more than adults, and the gap widens dramatically based on age. A 16-year-old pays roughly $8,003 per year according to The Zebra’s analysis of over 32 million insurance rates, compared to about $5,690 at age 19. That’s a $2,313 difference in just three years of driving experience. The state requires minimum liability coverage of $15,000 per person and $30,000 per accident for bodily injury, plus $5,000 for property damage. These minimums are non-negotiable if your teen drives legally in Pennsylvania, but they represent the bare floor. Many families need additional protection through collision and comprehensive coverage, especially if the vehicle is financed or leased. The real cost depends on what your teen drives, where they live within Pennsylvania, and their driving record from day one.

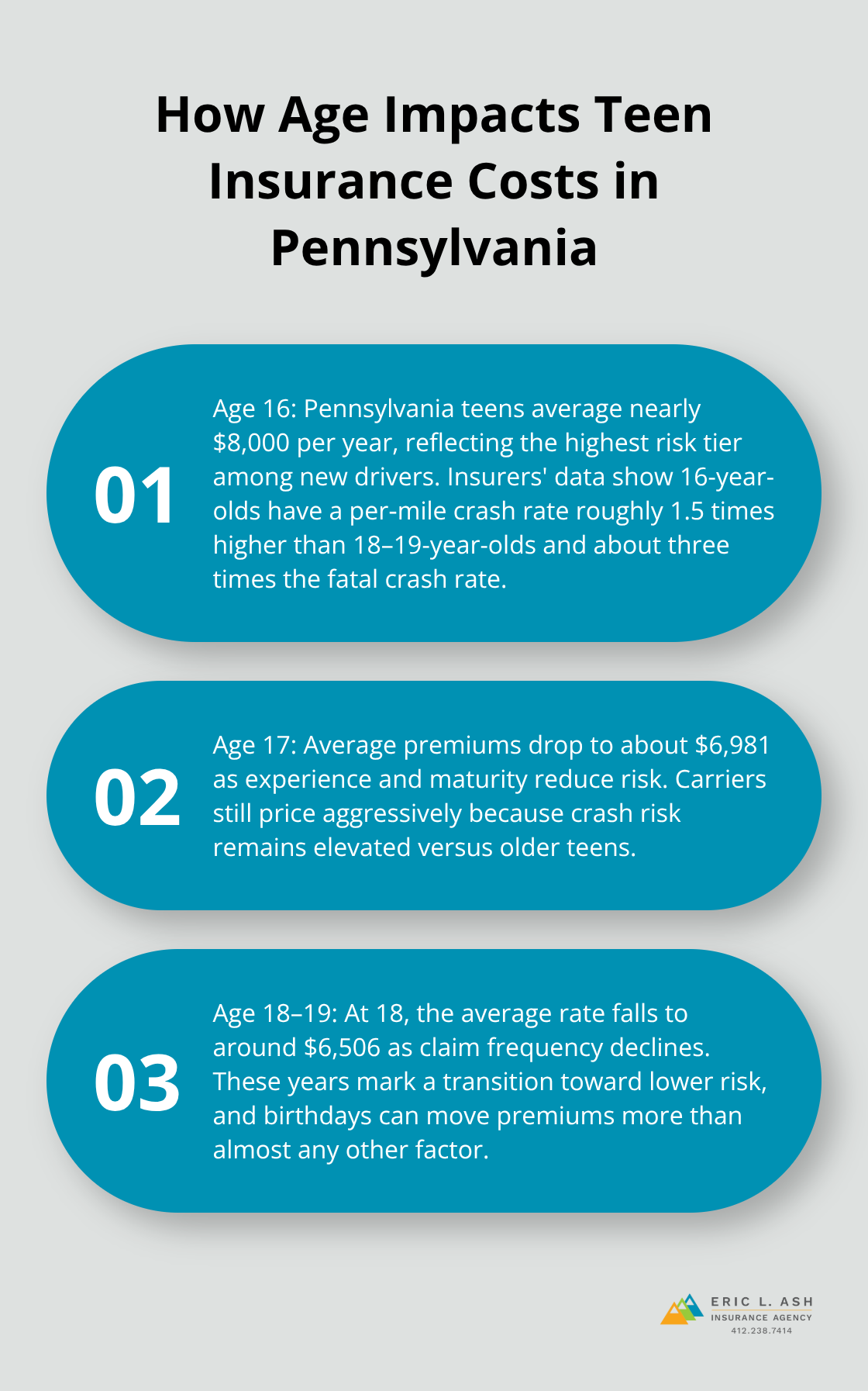

Age Makes an Enormous Difference

Pennsylvania doesn’t ban age-based pricing like California, Hawaii, and Massachusetts do, so insurers charge substantially more for younger drivers. The progression is steep: 16-year-olds average nearly $8,000 annually, 17-year-olds drop to about $6,981, and at 18 the rate falls to $6,506. This reflects insurers’ data showing that 16-year-olds have a per-mile crash rate roughly 1.5 times higher than 18 and 19-year-olds, and a fatal crash rate approximately three times higher according to the Insurance Institute for Highway Safety. Male teen drivers pay up to 9 percent more than females at age 16 due to documented higher-risk behaviors. These aren’t arbitrary charges; they’re rooted in actual crash statistics. Your teen’s birthday matters more to their insurance bill than almost any other factor during these early years.

Where You Live in Pennsylvania Changes Everything

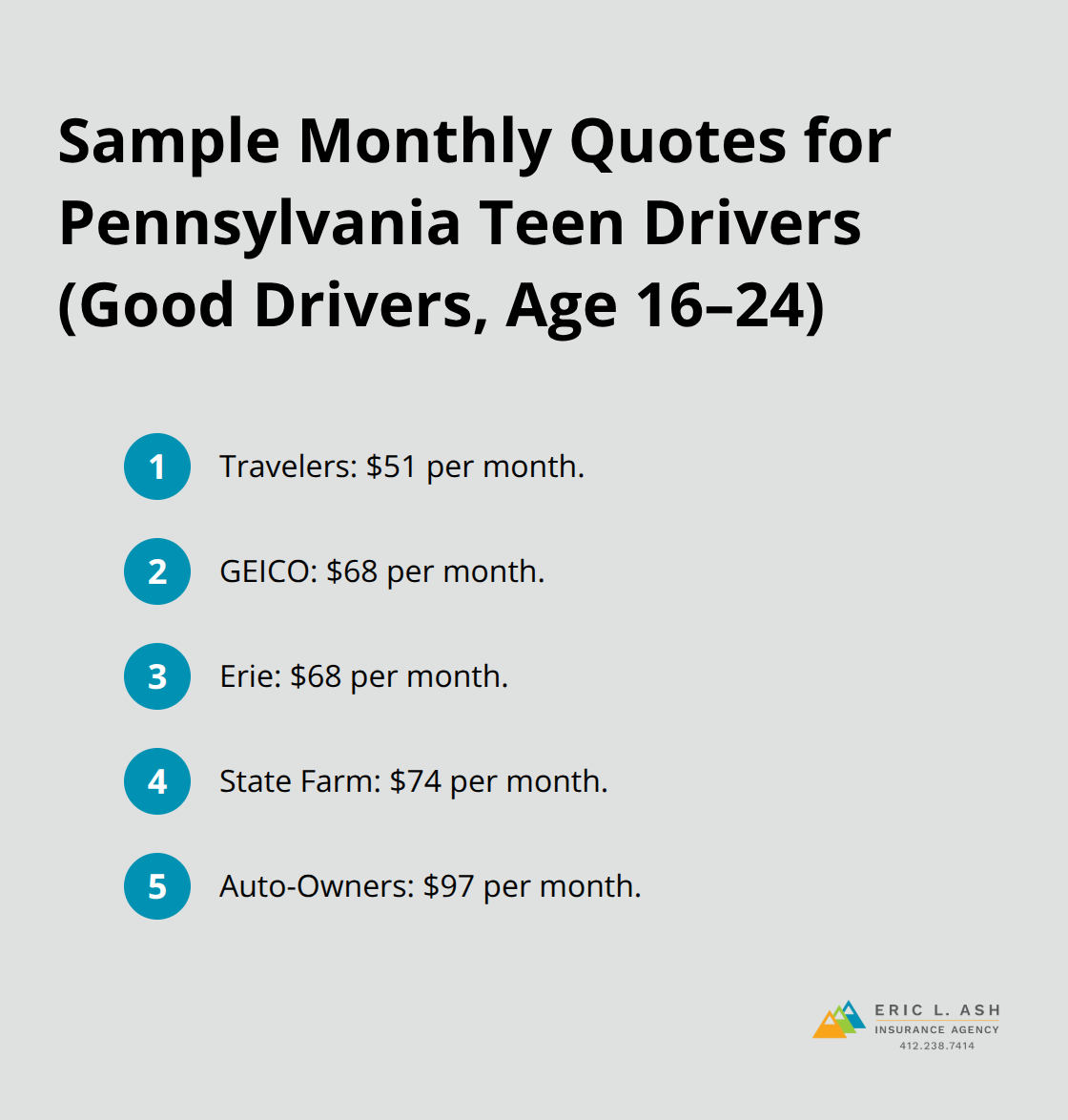

Pennsylvania’s rates vary wildly across location and surrounding ZIP codes. Some states exceed $10,000 annually for teen coverage, while North Carolina sits around $3,692 per year. Pennsylvania falls somewhere in the middle-to-higher range, but specific premiums depend heavily on urban versus rural areas, population density, and local claim history. You should shop around every six months after your teen turns 16 if you want competitive pricing. Representative quotes from major insurers in Pennsylvania show Travelers at $51 monthly, GEICO and Erie at $68, State Farm at $74, and Auto-Owners at $97 for good drivers aged 16 to 24. These variations prove that one company’s quote can be $46 cheaper per month than another’s, totaling over $550 annually.

As a veteran-owned, independent insurance agency in Pennsylvania, we leverage relationships with dozens of carriers specifically to help families find those competitive gaps rather than accept the first quote.

What Happens Next With Your Teen’s Rates

Your teen’s premium doesn’t stay frozen at age 16. Adding a teenage driver to your insurance policy can significantly increase your premiums due to their inexperience and higher risk factors, but each year of clean driving history lowers the cost, and most insurers reduce rates significantly until around age 25 (assuming no major violations or accidents). The vehicle itself also affects pricing-a low-value car under $4,000 costs less to insure than a high-performance vehicle, and you can cut costs further by dropping collision and comprehensive on older vehicles. Your teen’s driving record from the first day matters tremendously; even one ticket or minor accident can spike premiums or make it cheaper to move them to their own policy rather than keeping them on yours. The next section covers specific actions you can take right now to lower these costs before your teen even gets behind the wheel.

How to Cut Your Teen’s Insurance Costs Before They Get a License

The fastest way to lower your teen’s insurance premium is to act before they turn 16. Most families wait until their teen passes the driving test, then scramble to find affordable coverage. That approach costs money. Insurers reward specific actions taken early, and the savings stack quickly.

Complete a Defensive Driving Course

A defensive driving course completed before licensure triggers discounts immediately. Many major insurers including Liberty Mutual and GEICO offer discounts for drivers under 21 who complete a qualified program, but the discount amount varies by carrier and state. Contact your insurer before enrollment to confirm which courses qualify and what savings apply in Pennsylvania. The course teaches your teen to anticipate hazards and react defensively, which directly reduces crash risk and signals to insurers that you prioritize safety.

Maintain Good Grades for Immediate Savings

Good grades translate directly to lower premiums. A good student discount requires your teen to maintain at least a B average, and this discount applies to full-time students under 25 at most major carriers. The discount typically ranges from 10 to 15 percent depending on the insurer. Your teen’s GPA directly translates to money in your pocket, which motivates many families once they understand the connection. This discount costs nothing to earn and requires no additional paperwork beyond providing proof of grades when you apply.

Enroll in a Telematics Program Early

Telematics and monitoring programs deliver the largest savings when your teen starts participation early. These apps track acceleration, braking, phone use, and nighttime driving, then provide feedback to help your teen understand exactly which behaviors spike crash risk. Safe drivers who participate in programs like Liberty Mutual’s RightTrack can see premium reductions up to 30 percent within months. The key is starting participation early in their driving journey when habits are still forming, not after they’ve already developed risky patterns. Insurers see participation as a signal that you’re serious about safety, and they price accordingly.

Stack Your Discounts for Maximum Impact

The real savings come from combining all three strategies. A teen who completes a defensive driving course, maintains a B average, and enrolls in a telematics program qualifies for multiple discounts that compound across different coverage types. One insurer’s discounts may not apply to another’s, which is why shopping around matters. As a veteran-owned, independent insurance agency in Pennsylvania, we leverage relationships with dozens of carriers to identify which specific discounts your carrier offers and ensure your teen qualifies for every one available. The difference between acting now and waiting is often $500 to $1,500 annually-money that compounds year after year as your teen builds a clean driving record.

Your teen’s actual driving behavior on the road will determine whether these discounts stick around. The next section covers the specific mistakes that erase savings and spike premiums, and how to help your teen avoid them.

What One Mistake Costs Your Teen’s Insurance

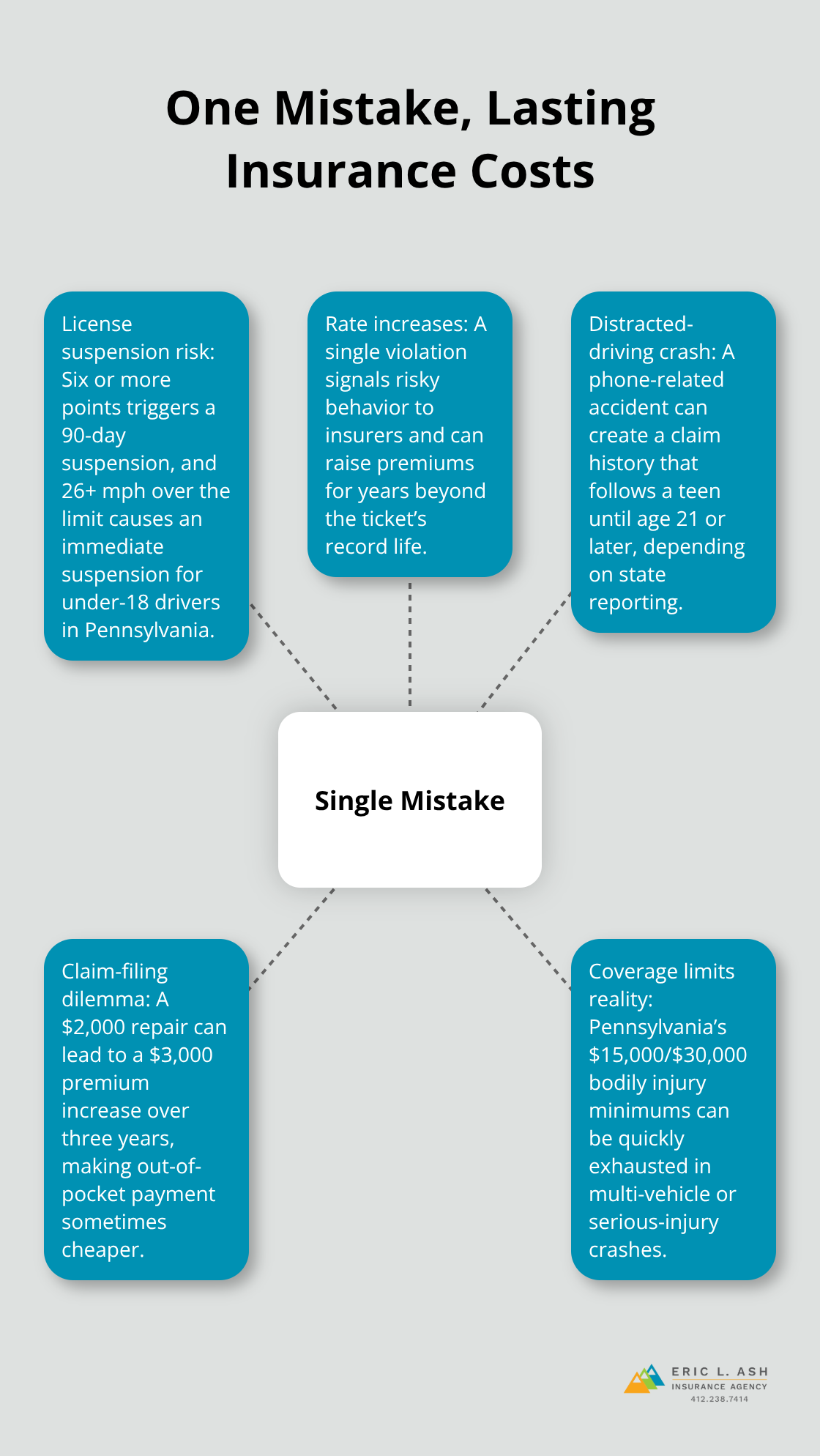

One speeding ticket at age 16 can lock your teen into higher premiums for years. Pennsylvania’s risk-based sanctions for under-18 drivers are severe: accumulating six or more points triggers a 90-day license suspension, and driving 26 mph or more over the limit results in an immediate suspension regardless of point count. The insurance consequence runs deeper than the suspension itself. A single violation signals to insurers that your teen engages in risky behavior, and that signal translates into rate increases that persist long after the ticket disappears from their driving record.

According to the Insurance Institute for Highway Safety, speeding and improper turning rank among the top contributing factors in teen crashes. Your teen’s first instinct after getting a ticket might be to hide it from you, but the insurer will find it during the next renewal. At that point, keeping them on your policy might actually cost more than moving them to their own separate policy.

How Distracted Driving Multiplies Your Costs

Distracted driving compounds this problem dramatically. The CDC documents that teen drivers have higher rates of distracted driving than older drivers, and a single accident caused by phone use doesn’t just spike your premium-it creates a claim history that follows your teen for years. If your teen causes an accident while texting at age 16, that claim will be visible to insurers until age 21 or later depending on your state’s reporting window. The accident itself matters less than what caused it; an insurer reviewing a distracted-driving claim will price your teen’s risk substantially higher than someone who had a single unavoidable collision.

The Claim-Filing Dilemma

Filing a claim early in your teen’s driving history creates a permanent record that underwriters reference forever. Many families face a genuine dilemma: their teen causes minor damage worth $2,000, but filing a claim triggers a $3,000 rate increase over three years. In that scenario, paying out of pocket and skipping the claim saves money overall. However, this calculation only works for minor damage; if your teen causes serious injury or major property damage, not filing a claim exposes your family to liability that far exceeds the premium increase. Pennsylvania’s minimum coverage of $15,000 per person and $30,000 per accident sounds adequate until an accident involves multiple vehicles or serious injury. One bad decision at age 16-speeding through a school zone, checking a text message at a red light, or filing a claim for preventable damage-can cost your family thousands in elevated premiums across multiple years.

Making Financial Consequences Visible

The solution isn’t lecturing your teen about safety; it’s making the financial consequences visible and specific. Show your teen the exact dollar amount their speeding ticket will add to your premium. Calculate what a distracted-driving accident would cost in rate increases over five years, then compare that number to the cost of a new phone mount or hands-free system. Use Pennsylvania’s Graduated Driver Licensing restrictions as a framework rather than a frustration-the nighttime driving ban from 11 PM to 5 AM and passenger limits exist specifically because these situations create crash risk. Your teen’s first six months of driving determine whether they build a clean record that qualifies for premium reductions or a violation history that locks them into higher rates. As a veteran-owned, independent insurance agency in Pennsylvania, we help families understand these specific tradeoffs before their teen makes a costly mistake.

Final Thoughts

Your teen’s first year of driving determines whether they build a clean record that qualifies for premium reductions or a violation history that locks them into higher rates for years. The actions you take now-before your teen turns 16-directly control whether they pay $8,000 annually or significantly less. Complete a defensive driving course, maintain good grades, and enroll them in a telematics program that tracks their actual driving behavior, and these three steps compound into savings that reach $500 to $1,500 per year.

One speeding ticket at age 16 spikes your premium by hundreds of dollars annually, and a distracted-driving accident creates a claim history that follows your teen until age 21 or beyond. Pennsylvania’s minimum liability coverage of $15,000 per person and $30,000 per accident protects you legally, but only if your teen avoids the mistakes that trigger rate increases. Show your teen the exact dollar cost of risky behavior-not as a lecture, but as a financial reality they can understand and avoid.

Teen driver insurance Pennsylvania costs more than most families expect, but the cost isn’t fixed. Shopping around every six months after your teen turns 16 reveals competitive gaps between carriers that can save $500 or more annually, and we at Eric L. Ash Insurance Agency leverage relationships with dozens of carriers to identify which specific discounts your teen qualifies for. Contact us at ericlashagency.com to get a competitive quote and discuss coverage options tailored to your family’s situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.