Commercial Automobile Insurance PA: A Practical Guide

Running a business in Pennsylvania means managing multiple risks, and your commercial vehicles are among the biggest. Commercial automobile insurance PA protects your fleet, your employees, and your bottom line when accidents happen.

We at Eric L. Ash Insurance Agency help business owners navigate coverage options that actually fit their operations. This guide walks you through what’s covered, how to choose the right protection, and where you can cut costs without cutting corners.

What Your Commercial Auto Policy Actually Covers

Pennsylvania state law requires every commercial vehicle to carry liability coverage, with minimums of $15,000 per person and $30,000 per accident for bodily injury, plus $5,000 for property damage. These minimums exist because accidents happen, and when they do, the other party’s medical bills and vehicle repairs become your financial responsibility. Liability coverage pays for injuries and damage your vehicle causes to someone else-not damage to your own vehicle or employees. Many Pennsylvania business owners mistakenly assume their personal auto policy covers work driving, but it doesn’t. Personal policies explicitly exclude business use, which means you’re driving uninsured from a legal standpoint if you use a personal vehicle for business operations.

State Minimums vs. What You Actually Need

If you operate heavier trucks, your liability requirements climb significantly. Property carriers with vehicles under 10,000 pounds need bodily injury coverage of at least $300,000 per accident, while those over 10,000 pounds must carry $750,000 per accident. Cargo coverage adds another layer-you need at least $5,000 minimum for loss or damage to cargo per accident if you transport goods. These aren’t suggestions; Pennsylvania Code sections 52 Pa. Code §32.11 and §32.13 govern them. Collision and comprehensive coverage protect your own vehicles rather than the other party. Collision covers accidents with other vehicles or objects, while comprehensive handles theft, weather, and vandalism. These coverages aren’t mandatory under Pennsylvania law, but if you financed or leased your vehicles, your lender requires them. The cost difference between a $500 deductible versus $1,000 can run $200 to $400 annually per vehicle, so the math matters when you manage a fleet.

Protection When Other Drivers Fall Short

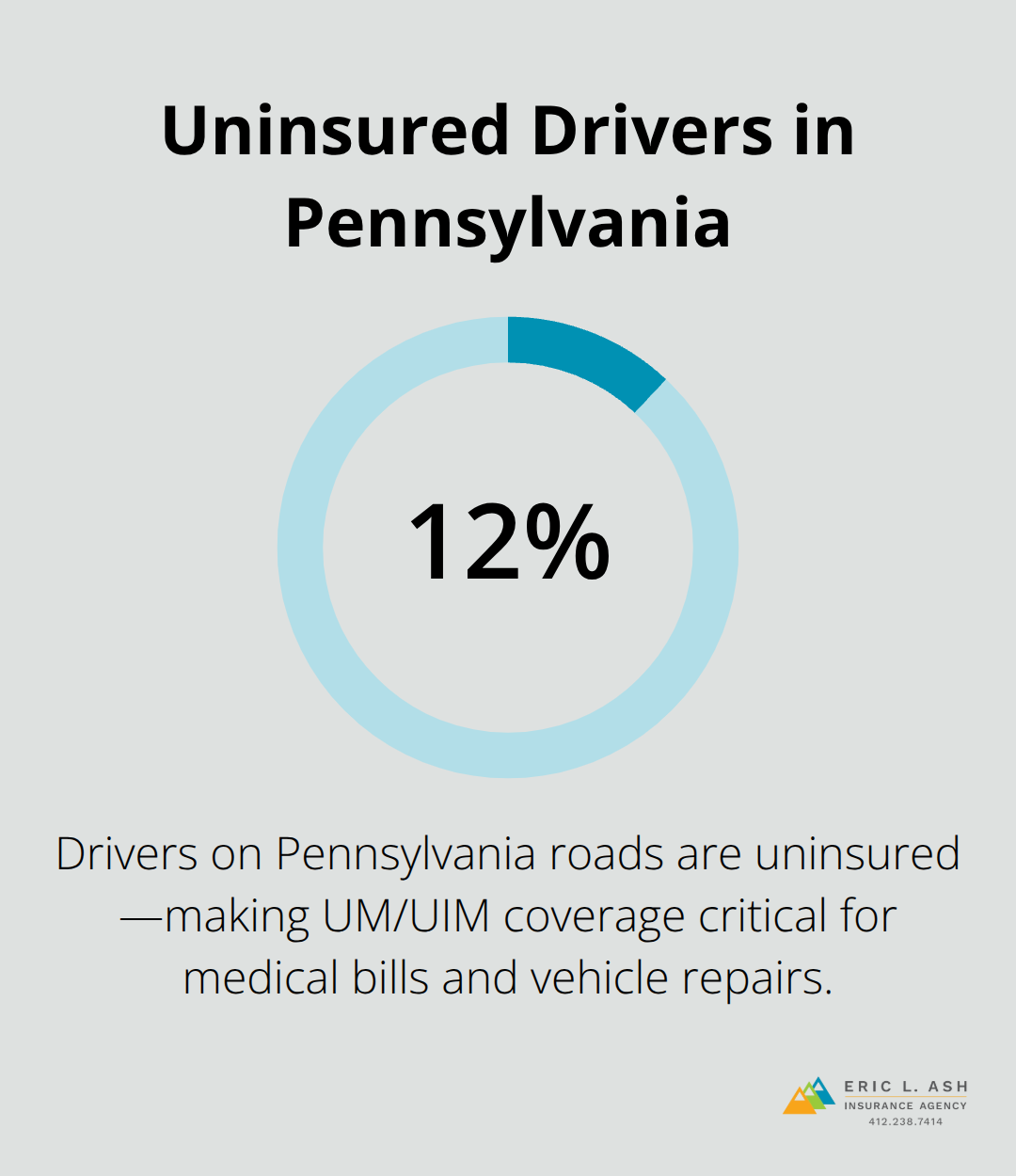

Uninsured and underinsured motorist coverage is where most Pennsylvania business owners cut corners and regret it later. If another driver hits your vehicle and carries no insurance or insufficient coverage, this protection covers your medical expenses and vehicle repairs up to your policy limit. Roughly 12% of drivers on Pennsylvania roads are uninsured according to industry data. Your employees ride in your vehicles, and if they suffer injuries in an accident caused by an uninsured driver, you face potential lawsuits without this protection.

Medical payments coverage works separately-it pays immediate medical expenses for you and your passengers regardless of fault. This coverage handles hospital visits, surgeries, and rehabilitation up to your selected limit.

Coverage for Vehicles You Don’t Own

Non-owned and hired auto liability protects your business when employees use personal vehicles for work or when you rent vehicles occasionally. This coverage protects your business when someone suffers injury while driving a vehicle you don’t own but are using for business purposes. It doesn’t repair the personal vehicle itself, but it covers your liability exposure, which is the real financial threat to your bottom line.

Now that you understand what commercial auto policies cover, the next step involves matching those coverages to your specific business needs and Pennsylvania’s regulatory landscape.

Matching Coverage to Your Fleet and Business Model

Start With What You Actually Operate

The gap between Pennsylvania’s minimum liability requirements and what actually protects your business depends almost entirely on what you operate and where you operate it. A single delivery van running local routes within Philadelphia faces different risks than a contractor with multiple box trucks servicing jobs across the state, and your coverage should reflect that difference. Start by cataloging exactly what you own: the number of vehicles, their weights, what they carry, and where your drivers spend most of their time.

Weight Classes and Pennsylvania’s Liability Tiers

A plumbing contractor with three service vans needs coverage according to Pennsylvania Code commercial vehicle liability requirements, but that same contractor hauling equipment across state lines into heavier-duty work may need higher coverage because vehicle weight triggers different requirements. The Pennsylvania Insurance Department’s guidance on commercial auto makes this clear-weight classes matter legally, not just for registration. If you transport cargo, the $5,000 minimum cargo coverage sounds reasonable until a load of merchandise worth $50,000 gets damaged in transit; most Pennsylvania business owners carrying goods should carry $25,000 to $50,000 in cargo coverage instead.

How Your Industry Shapes Your Risk Profile

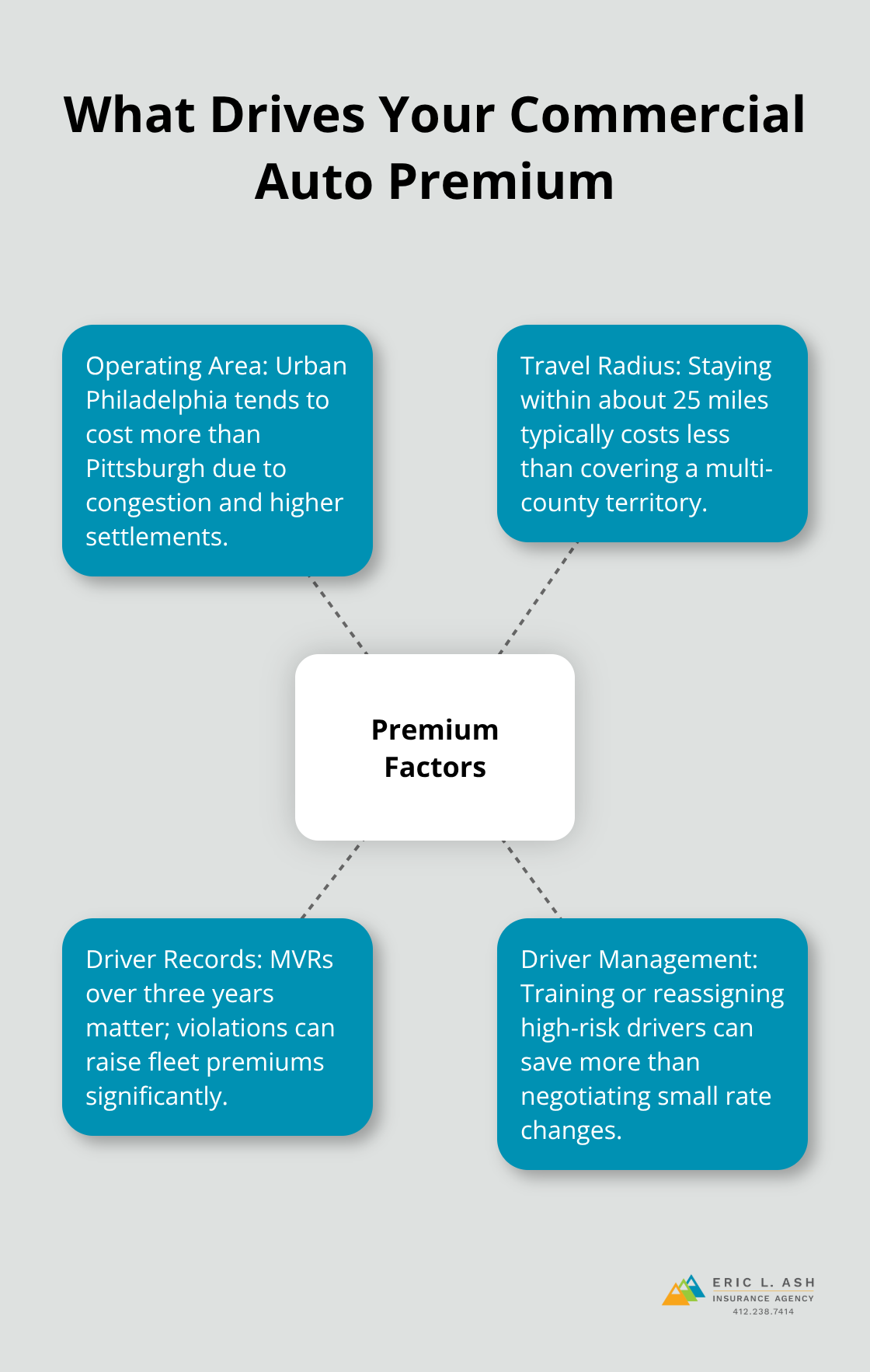

Your industry determines risk exposure more than almost anything else. A real estate agent using one sedan for client showings faces minimal exposure compared to a landscaper with a crew cab truck and trailer, where multiple employees operate equipment near roadways. Pizza delivery drivers represent higher accident frequency than office consultants using vehicles occasionally. Progressive, which insures over 2 million commercial vehicles nationally, structures rates heavily around your specific profession and operation type. When you work with an independent agency that represents multiple carriers, they can show you how different insurers price your exact business model-some specialize in contractors, others in service fleets, others in delivery operations. The cost difference between carriers for the same coverage can run 30 to 50 percent depending on how they view your industry risk.

Location and Travel Patterns Impact Your Costs

Operating primarily in Pittsburgh costs less than the same fleet based in Philadelphia, where urban congestion and higher settlement values inflate claims costs. Your travel radius matters too-a local service business staying within a 25-mile radius pays less than one covering a six-county territory. Before you finalize any coverage decision, pull your drivers’ motor vehicle reports for the last three years. One driver with multiple violations can increase your entire fleet’s premium by 15 to 25 percent, which means sometimes investing in driver training or excluding high-risk drivers from certain routes saves more money than negotiating rates.

Moving From Assessment to Action

Once you understand your fleet composition, weight classifications, cargo needs, and industry risk profile, you can move forward with selecting specific coverage limits that match your actual exposure rather than just meeting Pennsylvania’s minimums. The next step involves identifying which cost-saving strategies work best for your operation without leaving gaps in protection.

How to Actually Reduce Your Commercial Auto Costs

Stack Your Policies for Real Savings

Bundling your commercial auto policy with property, general liability, or workers compensation coverage can deliver meaningful savings, though the exact discount varies by insurer. The key is comparing apples to apples across carriers-some insurers price bundled packages aggressively while others don’t, so you need quotes from multiple companies to see where you actually save money. The real savings come when you find an insurer that wants your entire book of business, not just your auto policy. Before bundling, calculate what you currently pay for each separate policy, then compare the bundled quote to that total. If the bundled price isn’t at least 10 to 12 percent lower, the discount isn’t worth changing carriers for better auto rates elsewhere.

Lower Claims Through Safety and Driver Management

Driver training programs and fleet safety initiatives reduce accident frequency, which directly lowers your premiums over time-insurers track your claims history closely, and three years without accidents qualifies you for safe-fleet discounts that run 5 to 15 percent depending on the carrier. Telematics devices that monitor driving behavior, hard braking, and speeding patterns can earn you additional discounts of 10 to 20 percent if your drivers maintain safe habits, though this requires your team’s buy-in since they’ll know they’re monitored. Anti-theft devices, GPS tracking, and alarm systems on your vehicles reduce theft risk and can lower comprehensive coverage costs. Your drivers’ motor vehicle records matter enormously; one driver with multiple violations can spike your entire fleet’s rate by 15 to 25 percent, so sometimes removing that driver from certain routes or investing in remedial training costs less than absorbing the premium increase.

Adjust Your Deductible Strategically

Increasing your deductible from $500 to $1,000 per claim cuts your premium roughly $200 to $400 annually per vehicle, but only if you can afford to pay that deductible out-of-pocket when a claim happens-don’t raise your deductible just to lower premiums if an accident would strain your cash flow. This strategy works best for fleets with strong safety records and adequate cash reserves to cover unexpected out-of-pocket costs.

Keep Your Coverage Current

Review your policy annually with your agent, especially when your fleet changes, your service area expands, or you add new drivers, because outdated information means you’re either overpaying or carrying inadequate limits for your current operations. As your business evolves, your coverage needs shift, and staying aligned with your actual risk profile prevents costly gaps or unnecessary expenses.

Final Thoughts

Commercial automobile insurance PA shifts as your business grows, your fleet changes, and your routes expand. The Pennsylvania minimums of $15,000 per person and $30,000 per accident for bodily injury meet legal requirements, but they rarely protect your business financially. Most Pennsylvania business owners operating beyond basic local delivery or service work need higher limits that match their actual exposure.

Three decisions drive your protection strategy. Match your liability limits to your vehicle weights and cargo operations rather than defaulting to state minimums, implement driver training and safety programs that reduce claims and qualify you for discounts worth thousands annually, and review your policy yearly to adjust coverage when your operations change. Getting quotes from multiple carriers reveals how dramatically rates vary for identical coverage, and an independent agency that represents dozens of insurers can show you options you’d never find shopping individual company websites.

Start by gathering information about your current fleet, your drivers’ records, and your typical routes, then reach out to get quotes that reflect your actual business model. The difference between adequate coverage and inadequate coverage often costs less than you’d expect, and the difference between paying too much and paying fairly can run hundreds of dollars monthly across your fleet. Contact Eric L. Ash Insurance Agency to discuss your commercial automobile insurance needs and get quotes tailored to your Pennsylvania business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.