Commercial Vehicle Insurance Rates: What Affects the Premiums

Running a business with commercial vehicles means managing costs carefully. Commercial vehicle insurance rates can vary dramatically based on factors you might not expect, and understanding what drives those premiums is the first step toward smarter spending.

At Eric L. Ash Insurance Agency, we’ve helped countless Pennsylvania business owners find coverage that fits their needs and budget. This guide walks you through the real factors that shape your rates and shows you concrete ways to reduce what you pay.

What Drives Your Commercial Vehicle Insurance Premiums

Vehicle Type and Weight Matter Most

The vehicle sitting in your lot shapes your insurance costs more than almost any other factor. A box truck costs substantially more to insure than a sedan, and a tractor-trailer can run $3,000 to $5,000 or more annually per vehicle depending on risk factors, compared to $1,200 to $2,500 for lighter vehicles. Heavier vehicles cause more damage in accidents, which means higher repair bills and greater liability exposure for insurers. Vehicle type directly shapes your premium because the physics of a collision involving a 30,000-pound truck differs dramatically from one involving a 4,000-pound car.

How You Use Your Vehicle Affects Your Rate

How you operate that vehicle matters equally. A contractor running a pickup locally faces different rates than one hauling materials across state lines daily. Annual mileage and distance traveled multiply your accident risk, so a delivery service clocking 50,000 miles yearly will pay more than a consulting firm with a single sedan driven 5,000 miles annually. Urban routes in Philadelphia or Pittsburgh also cost more to insure than rural operations due to higher traffic density, theft risk, and accident frequency in those areas.

Driver Records Drive Premium Costs

Your drivers are the single biggest factor insurers evaluate, and their records directly determine what you pay. A clean driving history lowers premiums significantly, while accidents, violations, or DUIs spike costs immediately. Bodily injury loss costs rose 9.2 percent from 2023 to 2024, driven partly by more uninsured motorists and medical cost inflation. Speeding alone accounts for 28 percent of traffic fatalities, and among speeding-related fatal crashes, 52 percent of drivers weren’t wearing seatbelts, increasing crash severity and claim amounts.

Inexperienced drivers have higher rates of preventable crashes, which is why the commercial driver shortage pushing more inexperienced operators behind the wheel directly raises fleet insurance costs.

Safety Technology Reduces Your Premiums

Safety technology and features cut through the noise here. Telematics systems, collision avoidance technology, and anti-theft devices demonstrate reduced risk to insurers and often qualify you for measurable discounts. A fleet investing in formal safety programs and driver training shows insurers you take risk seriously, and that commitment translates to lower premiums over time. These investments signal to carriers that you manage your operation with care, which opens the door to better rates and more favorable terms when you shop for coverage.

How Your Industry Shapes What You Pay

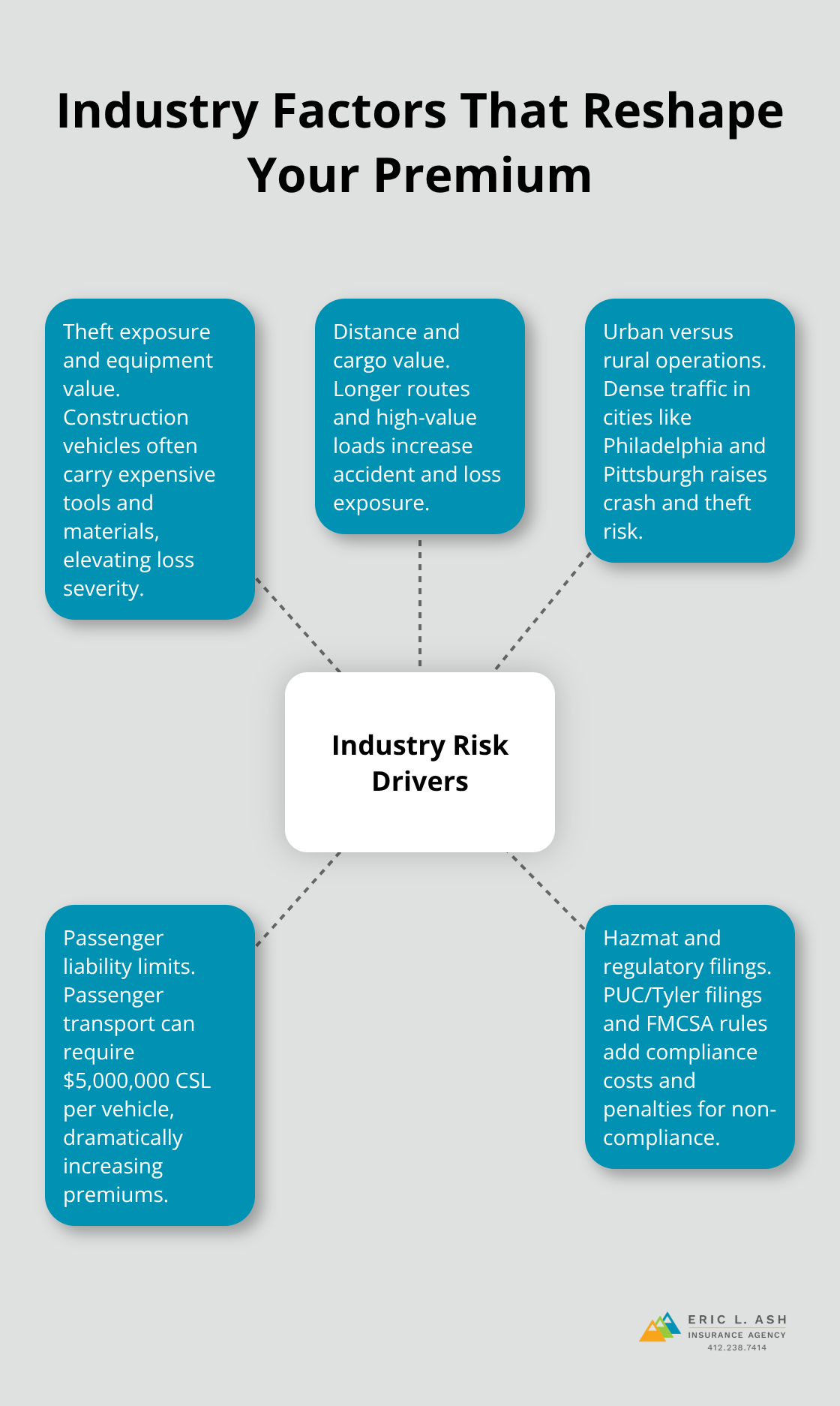

Construction and Delivery Services Face Higher Theft and Distance Risk

Construction companies and delivery services operate under dramatically different risk profiles than rideshare fleets or hazmat carriers, and insurers price accordingly. Construction vehicles face higher theft risk, operate in unpredictable environments, and often carry expensive equipment or materials. A contractor’s pickup used for local jobs costs less than one making long-haul deliveries across multiple states, because distance multiplied by cargo value and accident exposure drives premiums upward. Delivery services in urban centers like Philadelphia and Pittsburgh pay substantially more than rural operations due to traffic density and accident frequency in those areas.

Fleet Size Multiplies Your Total Costs

The gap between a single-vehicle operation and a fleet of five delivery trucks isn’t just additive-it’s multiplicative. Larger fleets attract higher total premiums even if per-vehicle discounts apply. A contractor managing one pickup pays far less than one operating ten vehicles, though the per-vehicle rate may drop slightly with volume.

Passenger Transport Demands the Highest Coverage Limits

Passenger transport and rideshare operations face the steepest rate increases because human liability exposure dwarfs property damage concerns. A rideshare driver carrying passengers faces fundamentally different risk than a contractor hauling materials, and Pennsylvania’s minimum liability requirements reflect this reality. For passenger carriers, the state requires Pennsylvania’s minimum liability requirements for passenger carriers of $5,000,000 combined single limit per accident per vehicle-a requirement that drives premiums dramatically higher for larger operations.

Hazmat and Specialized Cargo Add Regulatory Complexity

Specialized cargo and hazmat transport introduces regulatory complexity beyond basic liability. These carriers must file binding evidence of insurance with the Pennsylvania Public Utility Commission through Tyler Insurance Filings within 60 days or face application dismissal. Cargo insurance minimums sit at 5,000 per accident, but actual cargo values often demand higher limits. Carriers hauling hazardous materials face additional federal Motor Carrier Safety Administration requirements tied to their USDOT number, and non-compliance creates both premium penalties and operational shutdowns.

Your industry determines your baseline cost, and regulatory requirements add mandatory layers that generic policies cannot cover. Shopping for carriers experienced in your specific sector matters far more than finding the cheapest quote, because an underinsured rideshare operation or a cargo hauler without proper FMCSA compliance faces catastrophic financial exposure when incidents occur. The strategies that work for one industry may leave another dangerously exposed, which is why the next section focuses on concrete steps you can take to lower costs without sacrificing the protection your operation actually needs.

How to Cut Your Commercial Vehicle Insurance Costs

The strategies that actually work to lower your premiums fall into two camps: reducing your risk profile so insurers charge you less, and shopping aggressively to find carriers willing to compete for your business. Most Pennsylvania business owners focus only on the second part and miss the first entirely, which means they leave money on the table year after year. The real savings come from combining both approaches simultaneously.

Build a Strong Safety Record to Qualify for Lower Rates

Your driver records and fleet safety practices form the foundation of lower rates because they directly address what insurers fear most: claims. A single accident or violation spikes your premium immediately, but a clean driving history compounds discounts over multiple years. Bodily injury loss costs rose 9.2 percent from 2023 to 2024, which means insurers scrutinize driver behavior more carefully than ever. Formal fleet safety programs with documented driver training show carriers you take prevention seriously, and that commitment translates into measurable rate reductions.

Use Technology and Policies to Demonstrate Risk Management

A contractor or delivery service that tracks mileage, enforces seatbelt use, and monitors speeding through telematics systems qualifies for discounts that can offset the cost of the technology within months. Distracted driving policies carry equal weight because 25 percent of employees report crashes or collisions while driving for work due to mobile-device distractions, according to the Travelers Risk Index. Enforcing a no-phone policy and providing hands-free solutions demonstrates risk management that insurers reward with lower quotes. The investment in safety infrastructure pays dividends immediately when you shop for renewal quotes, because carriers see documented evidence that your operation runs tighter than your competitors.

Adjust Your Deductible Based on Your Claim History

Raising your deductible from $500 to $1,000 or $1,500 lowers your monthly premium substantially, but only if your fleet’s claim frequency supports that trade-off. A delivery service with multiple minor incidents annually should not pursue higher deductibles, while a contractor with a clean five-year record can safely absorb larger out-of-pocket costs per claim.

Shop Multiple Carriers and Bundle Your Policies

Shopping multiple carriers annually is non-negotiable because rates shift constantly based on loss trends and competitive positioning. A quote from three carriers often reveals $2,000 to $4,000 in annual savings, and bundling your commercial auto policy with general liability or property coverage multiplies discounts further. An independent agent can leverage relationships with dozens of carriers to shop multiple markets and deliver competitive rates tailored to your specific operation, whether you work with a local agency or request quotes directly from insurers online.

Final Thoughts

Your commercial vehicle insurance rates reflect decisions you make every day about how you operate your business. Vehicle type, driver records, mileage, and safety practices shape what you pay, while your industry and location add additional cost layers that vary dramatically between carriers. The real opportunity lies in recognizing that shopping multiple insurers reveals $2,000 to $4,000 in annual savings, since carriers price identical risk differently based on their claims experience and underwriting appetite.

Start by reviewing your current coverage and driver records to spot quick wins that reduce your risk profile. Implement telematics or formal safety programs if you haven’t already, because these investments signal to insurers that you manage your operation with care and lower your commercial vehicle insurance rates accordingly. Then request quotes from at least three carriers and compare coverage levels alongside premiums to find the best fit for your specific operation.

We at Eric L. Ash Insurance Agency work with dozens of carriers to shop multiple markets and deliver competitive rates tailored to your business. Whether you operate a single vehicle or manage a fleet, our team handles the complexity so you can focus on running your business. Contact us today to discuss your coverage needs and get a quote that reflects the true value of your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.