Student Driver Car Insurance: A Beginner’s Guide

Getting your student behind the wheel is exciting, but student driver car insurance adds a layer of complexity that catches many families off guard. Insurance costs for young drivers can spike dramatically, and without the right information, you might overpay significantly.

At Eric L. Ash Insurance Agency, we’ve helped Pennsylvania families navigate this process. This guide walks you through what you need to know to find affordable coverage and help your student build safer driving habits.

Why Student Drivers Cost More to Insure

A student driver represents a specific insurance category that triggers higher premiums across the board. Insurance companies define a student driver as someone under 25 who is learning to drive or has limited driving experience, typically someone who recently obtained their license or is still operating under a learner’s permit. The age matters significantly because statistics show that drivers aged 16 to 19 have higher crash rates than drivers aged 20 and older, according to data from the National Highway Traffic Safety Administration. This isn’t about judgment-it’s raw math. Insurance companies price based on risk, and inexperienced drivers statistically cause more accidents. When you add a student to your policy, your premiums jump substantially. The increase depends on your student’s age, the vehicle they’ll drive, and Pennsylvania’s specific insurance requirements. A 16-year-old will typically cost more to insure than a 19-year-old with two years of driving experience.

The Real Cost of Inexperience

Your student’s age and driving history are the two factors that matter most when calculating their insurance rate. A 16-year-old with a fresh learner’s permit will pay significantly more than an 18-year-old who has been driving safely for two years. Rates drop measurably each year of safe driving until age 25, when insurance companies treat drivers as fully mature from a risk perspective. This means your student’s insurance costs will naturally decrease if they maintain a clean driving record-no accidents, no traffic violations. The vehicle choice also influences the final premium. Pickup trucks, minivans, and small SUVs typically cost less to insure than sports cars or luxury vehicles, partly because they have strong safety records and lower replacement costs if damaged. If your student doesn’t own a car yet and will drive a family vehicle with permission, that car’s safety features and value matter to your insurer. A newer vehicle with advanced safety technology may actually cost less to insure than an older model, despite the newer car’s higher market value.

How Adding a Student Changes Your Policy

When you add your student to your existing auto policy, your total premium increases, but it’s often cheaper than purchasing a separate policy for them. The exact savings depend on whether your household has other violations or accidents on record. If you have a clean driving history, adding your student to your policy makes financial sense. However, if you’ve had recent tickets or accidents, your student might actually qualify for lower rates on their own separate policy, since their premium won’t be bundled with your driving record. This is where shopping around becomes essential. Get quotes from multiple insurers-both for adding your student to your existing policy and for a standalone policy in their name. The difference can be hundreds of dollars annually. Some families find that one insurer offers better rates for bundling while another charges less for a separate policy. As an independent agency, we shop multiple carriers to help Pennsylvania families compare these exact scenarios and find the approach that saves them the most money.

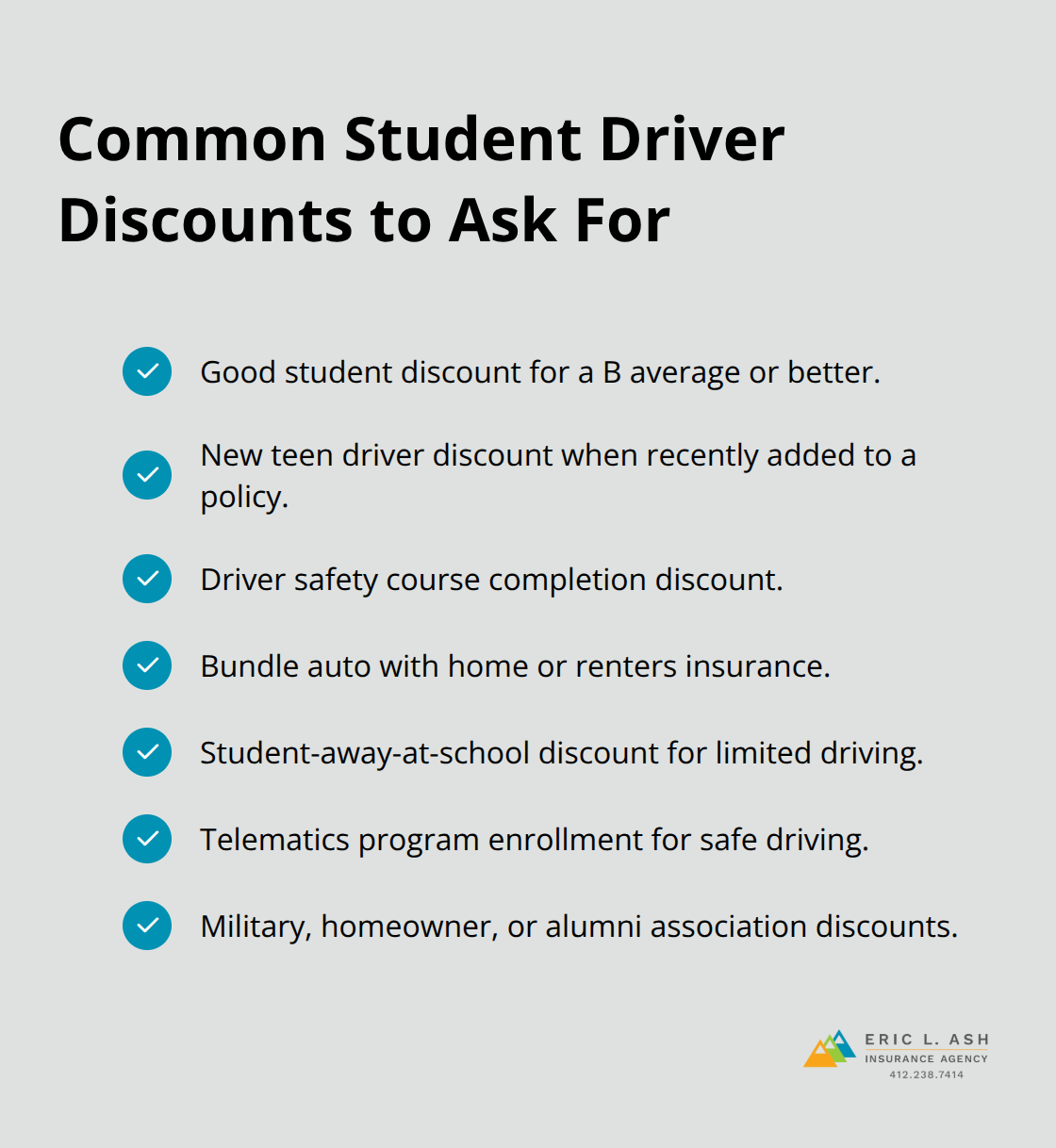

Discounts That Lower Student Driver Costs

Student drivers qualify for several discounts that can meaningfully reduce what you pay. The good student discount applies to full-time students who maintain at least a B average or better-this discount is available in most states and can lower your premium. Some insurers offer discounts when you add a new teenage driver to your policy within the past year. If your student completes a qualifying driver safety course, you may qualify for an additional discount. Bundling auto insurance with home, renters, or other policies can save you money. These discounts stack, so a student with good grades who completes a safety course and bundles policies can see substantial savings compared to the base rate. The key is asking your insurer about every discount your student qualifies for-many families miss savings simply because they don’t ask.

Safe Driving Programs and Monitoring

Many insurers now offer telematics programs that monitor your student’s driving habits and reward safe behavior with discounts. These programs can reward up to 30% for safe driving and provide real-time feedback to help your student improve. The programs track acceleration, braking, speed, and time of day your student drives, then translate that data into actionable insights. Your student sees exactly where they need to improve, and you get visibility into their driving patterns. Not all states offer these programs, but they’re becoming increasingly common. If your insurer offers one, enrollment typically costs nothing and can pay for itself within months through the discount alone. This approach addresses the core reason student drivers cost more-their inexperience-by creating incentives for safer habits from day one. The next step in controlling costs involves understanding which coverage options your student actually needs and how to avoid overpaying for protection you don’t require.

How to Find the Right Coverage at the Right Price

Get Quotes from Multiple Insurers

Shopping for student driver insurance demands a systematic approach, and most families make costly mistakes by accepting the first quote they receive. Start by obtaining quotes from at least three different insurers, and specifically request quotes for two scenarios: adding your student to your existing policy and purchasing a separate policy in their name. The price difference between these approaches often surprises families. Bundling auto with home insurance can save over $950, and adding other coverages like renters or RV policies yields even more savings. However, this assumes your household qualifies for the bundling discount at that particular insurer.

Your situation might differ significantly. A student with a clean record added to a parent’s policy with violations might actually pay less on a standalone policy. When you request quotes, provide identical information to each insurer: your student’s age, driving history, the vehicle they’ll use, and your desired coverage limits.

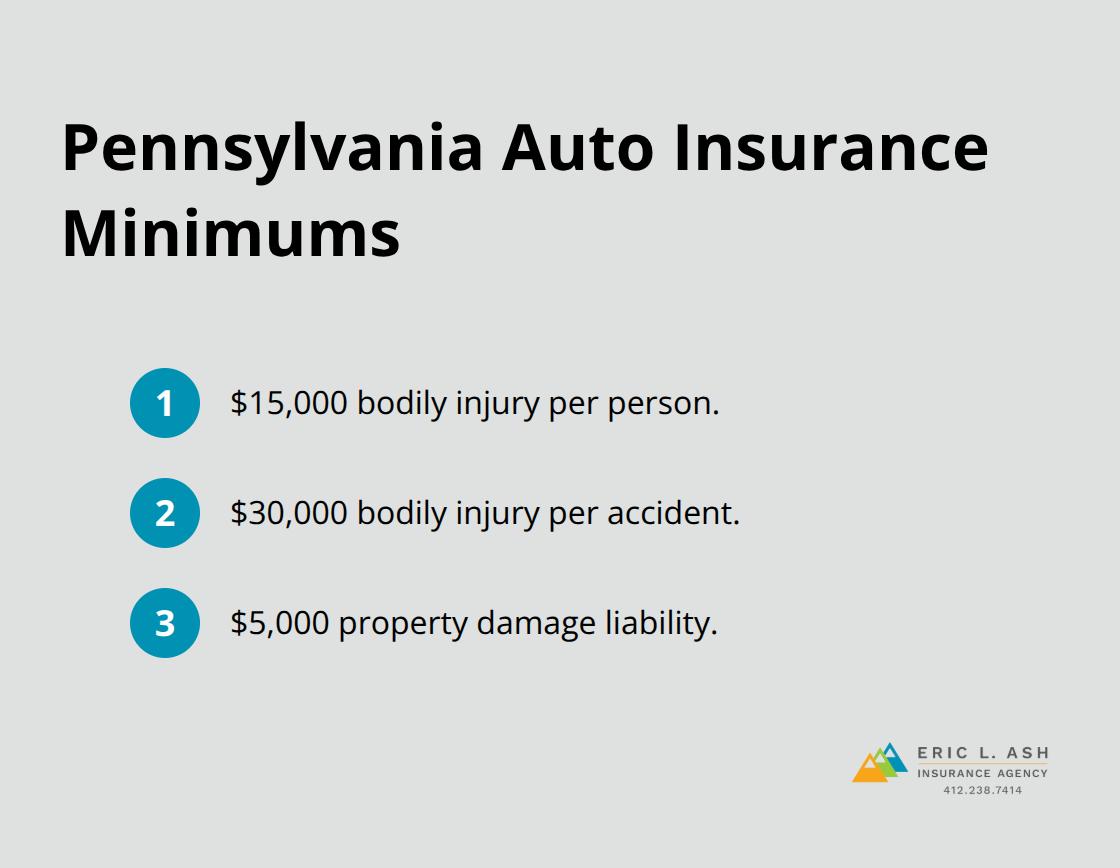

Understand Pennsylvania’s Minimum Requirements

Pennsylvania requires minimum liability coverage of $15,000 for injury or death to one person, $30,000 for injury or death to multiple people, and $5,000 for property damage. Many families stop at these minimums, but that’s genuinely a mistake. Medical bills from a serious accident far exceed these limits, and a lawsuit can follow.

Try coverage limits of at least $100,000 per person and $300,000 per accident to protect your family’s assets. Higher limits add minimal cost when you’re getting quotes anyway.

Stack Discounts to Maximize Savings

The discounts available to student drivers are substantial, and most families capture only a fraction of what they qualify for. A good student discount applies when your student maintains at least a B average and typically saves 10 to 15 percent on premiums. Some insurers offer an additional new teen driver discount when you add a teenage driver to your policy within the past year. If your student completes a driver safety course, you qualify for another discount. If your student attends school away from home and drives only occasionally, a student-away-at-school discount applies. If you have military service, homeownership, or alumni association membership, those generate additional discounts.

Stacking these discounts compounds the savings. A student with a B average who completes a safety course and qualifies for an alumni discount could reduce their base rate by 30 percent or more. When comparing quotes, ask each insurer to itemize every discount applied and every discount your student doesn’t yet qualify for but could earn.

Consider Telematics Programs for Additional Savings

Some insurers offer telematics programs that reward safe driving with up to 30 percent discounts, though these programs vary by state and insurer. These monitoring systems track acceleration, braking, speed, and time of day your student drives, then translate that data into actionable insights. Your student sees exactly where they need to improve, and you get visibility into their driving patterns.

Enrollment typically costs nothing and can pay for itself within months through the discount alone.

The key insight most families miss: the lowest quote from one insurer might not remain the lowest after you stack discounts at another insurer. Request quotes with all available discounts applied before you compare final prices. Once you’ve identified the most affordable option, the next step involves understanding how your student’s actual driving behavior influences their long-term costs and what actions they can take to keep premiums low.

Building Better Rates Through Grades and Safe Driving

How Good Grades Lower Your Student’s Premium

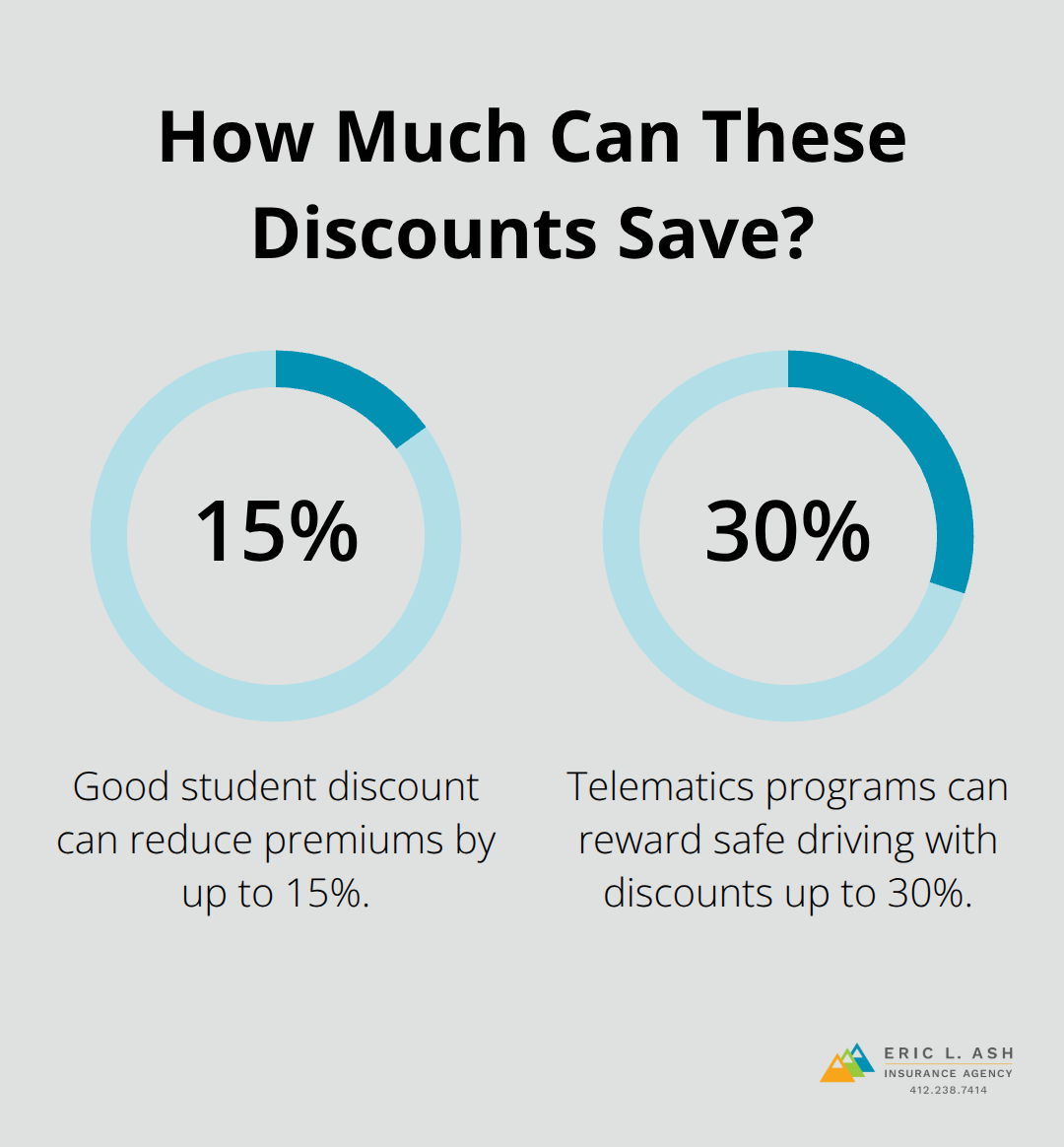

Your student’s grades matter more than most families realize. A B average qualifies your student for a good student discount that can reduce premiums by 5% to 15%, making it one of the easiest discounts to earn. The discount applies to full-time students under 25 who maintain that threshold, and it costs nothing except maintaining decent academic performance. What surprises most families is that this discount persists across multiple insurers, making it genuinely portable if you switch coverage later.

The math is straightforward: a student paying $2,000 annually saves $100 to $300 just by keeping a B average. That’s real money that compounds year after year. Some insurers bundle this with a new teen driver discount when you add a teenager to your policy within the past year, stacking savings on top of the grade-based reduction. Verify with your insurer that your student qualifies and that the discount actually appears on your bill. Insurers don’t always automatically activate discounts, so requesting confirmation ensures you capture what you’ve earned.

Safe Driving Programs That Reward Good Behavior

Telematics programs represent the most aggressive approach to lowering rates through behavior change. These monitoring systems reward safe driving with up to 30 percent discounts (though availability varies by state and insurer) and track acceleration, braking, speed, and time of day your student drives. Enrollment costs nothing, and your student receives real-time feedback showing exactly where their driving needs improvement.

A 16-year-old who completes a telematics program for six months often qualifies for a substantial rate reduction starting immediately, and the discount typically persists even after the monitoring period ends. The data from these programs proves invaluable: your student sees the connection between smooth acceleration, moderate speeds, and lower insurance costs in tangible terms. This transparency motivates safer habits far more effectively than lectures about responsibility.

How a Clean Driving Record Compounds Your Savings

A clean driving record compounds these savings significantly. Each year without accidents or traffic violations allows your premium to drop measurably until age 25, when insurance companies treat drivers as fully experienced. One accident or speeding ticket can erase years of safe driving discounts and trigger a rate increase lasting three to five years.

This means a single poor decision at age 17 costs your family thousands in elevated premiums through age 22. Your student’s actual driving behavior directly controls whether they pay $1,800 or $2,400 annually for the same coverage. The incentive structure is powerful: maintaining a clean record translates directly into lower costs that accumulate over time.

Final Thoughts

Student driver car insurance doesn’t have to drain your family budget. Shop multiple insurers for both bundled and standalone policies, stack every discount your student qualifies for, and enroll in a telematics program if your insurer offers one. A student with good grades, a clean driving record, and safe driving habits will see their premiums drop measurably each year until age 25.

Your student’s first year of driving sets the tone for years to come. One accident or traffic violation can cost thousands in elevated premiums, while maintaining a clean record compounds savings annually. Pennsylvania requires proof of insurance at vehicle registration, and driving uninsured carries penalties including fines, license suspension, and registration suspension.

Contact Eric L. Ash Insurance Agency to get quotes for your student driver and find which discounts apply to your situation. We shop multiple carriers to find the rates and coverage that fit your family’s specific needs. Your first conversation costs nothing, and the savings often exceed what you’d find shopping alone.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.