Vacation Rental Insurance Pennsylvania: Coverage for Landlords

Renting out your property in Pennsylvania can be profitable, but standard homeowners insurance won’t protect your rental income or guest-related liabilities. That’s where vacation rental insurance Pennsylvania comes in-it fills the gaps that traditional policies leave wide open.

We at Eric L. Ash Insurance Agency help landlords understand exactly what coverage they need. Read on to learn what protects your investment and how to choose the right policy for your situation.

Why Vacation Rental Insurance Matters in Pennsylvania

Pennsylvania landlords often assume their standard homeowners policy covers vacation rental activity. It doesn’t. Most homeowners policies explicitly exclude rental income protection and liability claims from short-term guests, leaving you exposed to significant financial risk. When a guest gets injured on your property or causes damage, your homeowners insurance won’t pay for their medical bills or legal defense. Similarly, if a guest cancels last-minute and you lose that week’s rental income, standard coverage won’t reimburse you. Vacation rental insurance fills these exact gaps by providing liability coverage starting at $1 million per occurrence and loss of income protection that homeowners policies simply don’t offer.

Your Liability Exposure Is Real and Growing

Short-term rentals in Pennsylvania create liability scenarios that traditional policies were never designed to handle. High guest turnover means more people on your property, more potential accidents, and more opportunities for someone to file a claim. A guest could slip on your stairs, suffer food poisoning from your kitchen, or injure themselves using an amenity like a hot tub or kayak. Each of these situations can result in medical expenses, legal costs, and settlement payments that quickly exceed $50,000. Vacation rental insurance covers these guest injury claims and your legal defense costs, protecting your personal assets from judgments. Without it, you’re personally liable for any damages a court awards.

Property Damage From Guests Requires Specialized Coverage

Guests treat rental properties differently than they treat their own homes. Water damage from broken pipes or overflowing appliances ranks among the most common and costly claims for rental properties. Vandalism, broken furniture, damaged appliances, and theft happen regularly in short-term rentals but fall outside standard homeowners coverage when guests cause them through negligence or intentional acts. Vacation rental insurance protects your building and furnishings from these guest-caused damages, covering repair or replacement costs without forcing you to absorb the loss yourself. Some policies even include protection against bed bugs and fleas (which can shut down your rental for weeks and cost thousands in extermination and lost bookings).

Why Standard Coverage Falls Short

Your homeowners policy was written for owner-occupied homes, not investment properties with constant guest traffic. Insurance companies know the difference between a family living in a home and a host running a vacation rental operation with constant guest turnover. A guest injury claim, a theft during turnover, or water damage from a guest’s negligence all fall into coverage gaps that leave you unprotected. Vacation rental insurance addresses these specific risks and fills the holes that standard policies create. The next step is understanding exactly what coverage options exist and how to match them to your property’s needs.

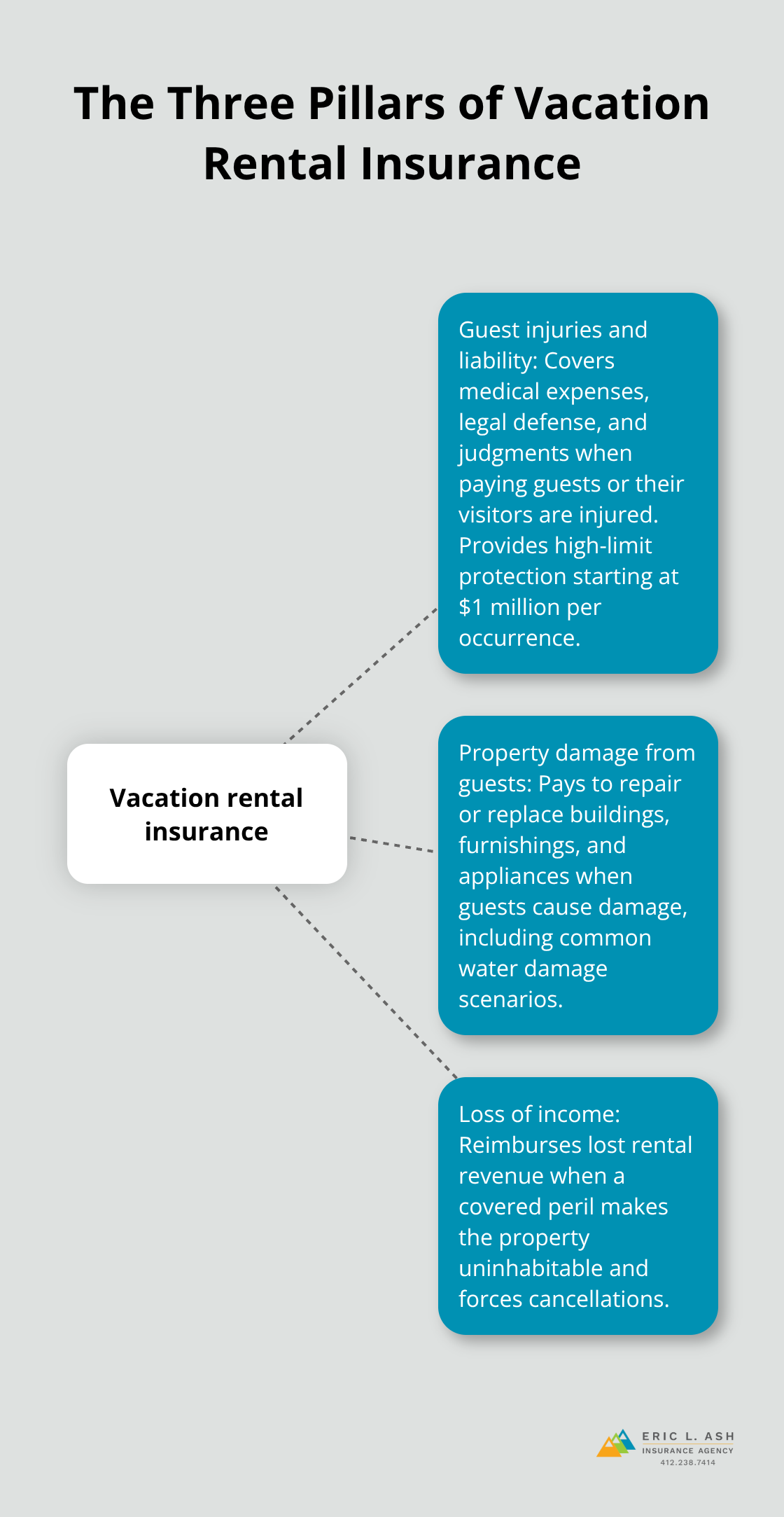

What Your Vacation Rental Insurance Actually Covers

Vacation rental insurance in Pennsylvania protects three critical areas that your standard homeowners policy ignores: guest injuries and liability, property damage caused by guests, and lost rental income when a covered event forces you to cancel bookings.

Guest Injury Claims Create Substantial Liability Exposure

A guest slips on your stairs and breaks their arm, demanding $75,000 in medical bills and pain and suffering. Your policy’s liability coverage defends you in court and pays the judgment up to your selected limit, typically starting at $1 million per occurrence. Strangers constantly move through your property in short-term rentals, which creates significant liability exposure. A guest falls off a ladder while adjusting the ceiling fan, a visitor slips on your pool deck, someone gets food poisoning from your kitchen, or a guest injures themselves on your hot tub or kayak equipment. Each scenario triggers medical expenses, potential lawsuits, and settlement demands that standard homeowners policies explicitly exclude when the injured party is a paying guest or someone in a guest’s party. Vacation rental liability coverage handles your legal defense costs and damage awards, protecting your personal savings and future earnings from a judgment. Pennsylvania courts award substantial damages in liability cases, making this protection non-negotiable for any property generating rental income.

Property Damage From Guest Negligence Happens Constantly

That same guest spills red wine on your furniture, breaks your kitchen table, and damages the rental’s appliances through careless use. Your property damage coverage reimburses you for repairs or replacement without forcing you to absorb the cost. Guests treat rental homes differently than their own spaces, which leads to frequent damage claims. Water damage from broken pipes, overflowing washing machines, and burst appliances ranks among the most frequent and expensive claims for rental properties. Guests cause vandalism, damage furniture during turnover, break appliances through misuse, and sometimes steal items. Your vacation rental policy covers guest-caused damages to your building, furnishings, appliances, and personal property used in the rental operation. Some policies add specialized protection for bed bugs and fleas, which can shut down your rental for weeks and cost thousands in extermination fees and lost bookings.

Loss of Income Coverage Protects Your Cash Flow

A severe storm damages your roof mid-season, making the property uninhabitable for two weeks. Your loss of income coverage reimburses you for the rental income you would have earned during those two weeks of vacancy. Loss of income coverage compensates you when a covered peril makes your property temporarily uninhabitable. A fire, severe storm damage, or water damage forces you to cancel bookings for repairs. Your policy reimburses you for the rental income you would have earned during that vacancy period, helping you maintain cash flow while the property gets restored. This protection matters because even a two-week closure can cost you thousands in lost bookings, and longer repairs can devastate your annual revenue projections.

These three coverage pillars address the real financial threats that Pennsylvania vacation rental operators face daily, and they’re completely absent from homeowners insurance. Understanding what each coverage type protects is only half the battle-the other half involves selecting the right limits and deductibles for your specific property and guest volume. That’s where the decision-making process becomes critical.

How to Choose the Right Vacation Rental Insurance

Start With Liability Coverage That Protects Your Assets

Select liability coverage of at least $1 million per occurrence. This minimum threshold protects Pennsylvania vacation rental operators because guest injury claims escalate quickly. A slip and fall with a broken hip costs $50,000 in medical expenses alone, plus legal defense costs and pain and suffering damages. Pennsylvania courts award substantial settlements in liability cases, so $1 million provides genuine protection without forcing you to choose between your personal assets and a judgment.

If your property has high-risk amenities like a hot tub, swimming pool, or kayak equipment, consider $2 million in liability coverage. The premium difference between $1 million and $2 million typically runs $200 to $400 annually-a modest investment given the exposure.

Match Property Damage Coverage to Current Replacement Costs

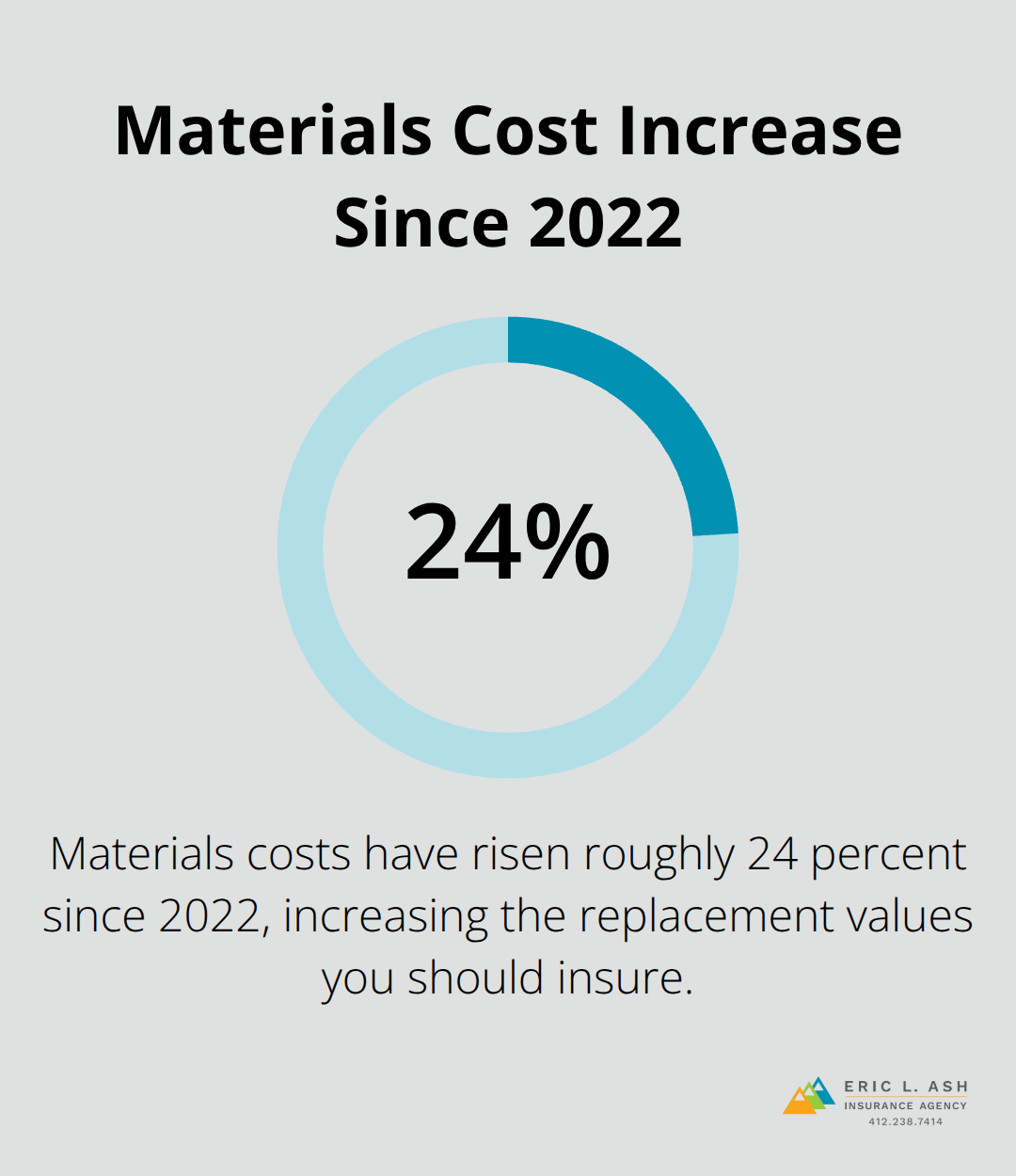

Property damage coverage should reflect your actual rebuild costs and replacement value of furnishings. Materials costs have risen roughly 24 percent since 2022, so your coverage limits need to match current replacement prices. If your property would cost $350,000 to rebuild, select a dwelling coverage limit at or above that figure.

Underinsuring creates coinsurance penalties where the insurance company pays only a fraction of your claim. This penalty can cost you thousands when you need coverage most. Calculate your rebuild costs carefully and update them every two to three years as material prices shift.

Set Loss of Income Coverage Based on Your Monthly Revenue

Loss of income coverage should equal your average monthly rental revenue multiplied by three to six months, depending on your risk tolerance. If you earn $4,000 monthly, select $12,000 to $24,000 in loss of income protection. This covers extended closures from major damage while you manage repairs without destroying your annual cash flow projections.

A two-week closure from storm damage or water damage can cost you thousands in lost bookings. Longer repairs from fires or structural damage can devastate your annual revenue. Loss of income coverage bridges that gap and keeps your business stable during recovery.

Balance Deductibles Against Out-of-Pocket Risk

Deductibles directly impact your premium costs, but selecting too high a deductible creates financial strain when claims occur. A $1,000 deductible is standard for Pennsylvania vacation rentals and balances affordability with manageable out-of-pocket costs. Raising it to $2,500 or $5,000 saves premium dollars but forces you to absorb substantial costs when water damage or guest damage claims happen.

Consider your cash reserves when selecting a deductible. If you have limited savings, a lower deductible protects you from unexpected expenses. If you maintain substantial reserves, a higher deductible can reduce your annual premium while keeping your financial risk manageable.

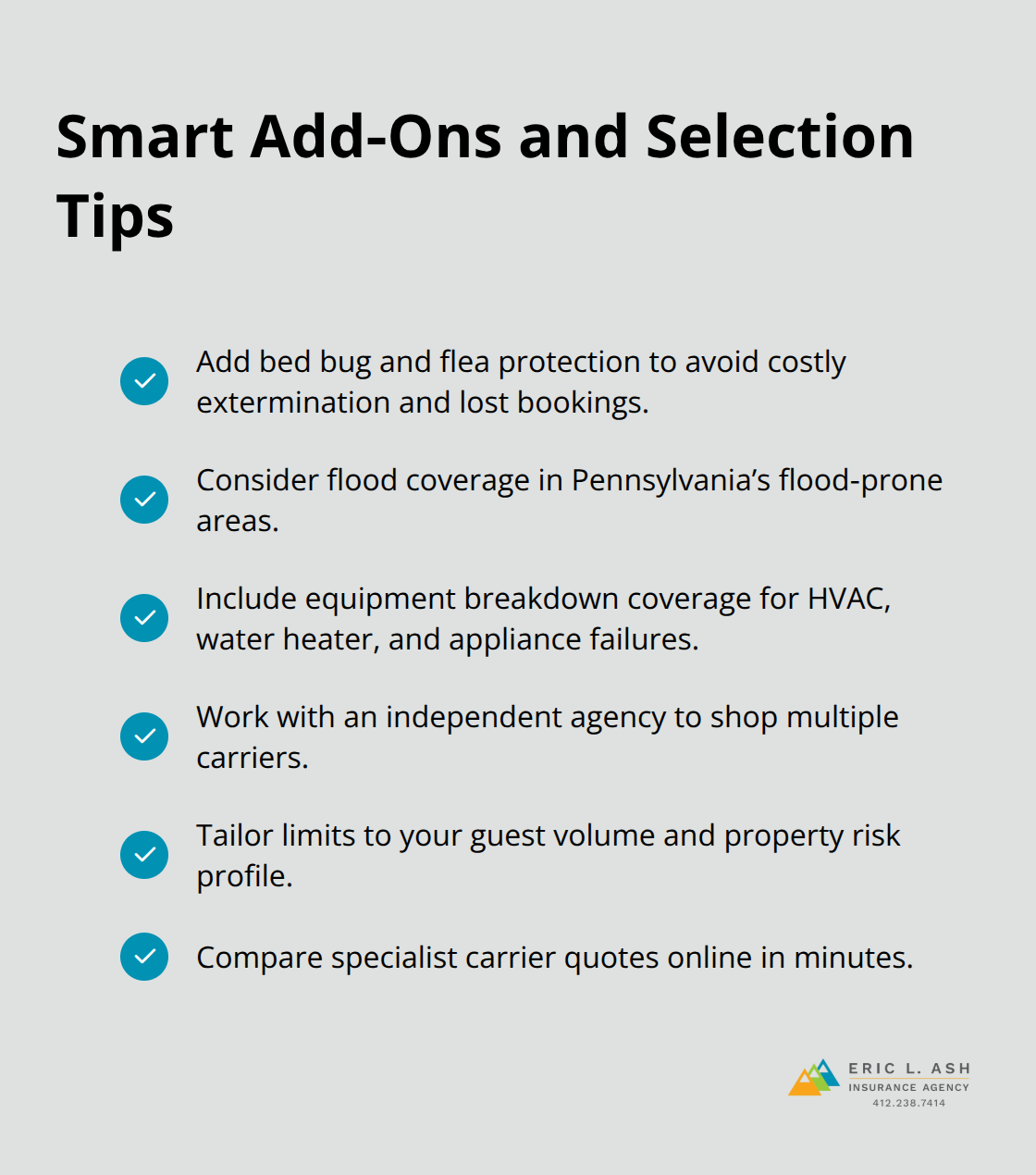

Add Optional Coverages That Address Your Specific Risks

Optional add-ons address risks that standard vacation rental policies don’t cover. Bed bug and flea protection costs $50 to $100 annually but can save thousands in extermination and lost bookings if an infestation occurs. Flood coverage protects your property in Pennsylvania’s flood-prone areas where standard policies exclude water damage from rising water. Equipment breakdown coverage reimburses you for sudden mechanical failures of your HVAC system, water heater, or appliances.

Work with an independent agency that shops multiple carriers to find policies tailored to your guest volume, property characteristics, and risk profile. An agent who understands Pennsylvania’s rental regulations and common claims patterns will identify coverage gaps you might miss and recommend add-ons worth considering. The quote process typically takes minutes online, so comparing actual rates from carriers that specialize in vacation rentals gives you concrete pricing rather than guessing at costs. Your policy should reflect your specific property and operation, not a generic template that leaves you under protected.

Final Thoughts

Vacation rental insurance Pennsylvania protects your investment where standard homeowners policies leave you completely exposed. Guest injuries, property damage, and lost rental income represent real financial threats that can cost you tens of thousands of dollars without proper coverage. A $1 million liability limit, property damage coverage matching your rebuild costs, and loss of income protection covering three to six months of revenue form the foundation of solid protection for Pennsylvania landlords.

The next step is getting quotes from carriers that specialize in vacation rentals rather than trying to force your property into a standard homeowners policy. Specialized carriers understand the unique risks of short-term rental operations and price coverage accordingly. The quote process takes minutes online, and comparing actual rates from multiple carriers gives you concrete pricing and coverage options tailored to your specific property.

We at Eric L. Ash Insurance Agency work with Pennsylvania landlords to build vacation rental coverage that actually protects their operations. Contact us at ericlashagency.com to discuss your vacation rental insurance needs and get a quote that reflects your actual exposure.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.