Vacation Rental Insurance Quotes: How to Compare Policies

Running a vacation rental means juggling multiple risks at once. Without the right insurance, a single guest injury or property damage claim could wipe out your profits for the year.

We at Eric L. Ash Insurance Agency help property owners in Pennsylvania find vacation rental insurance quotes that actually match their needs. This guide walks you through comparing policies so you can protect your business without overpaying.

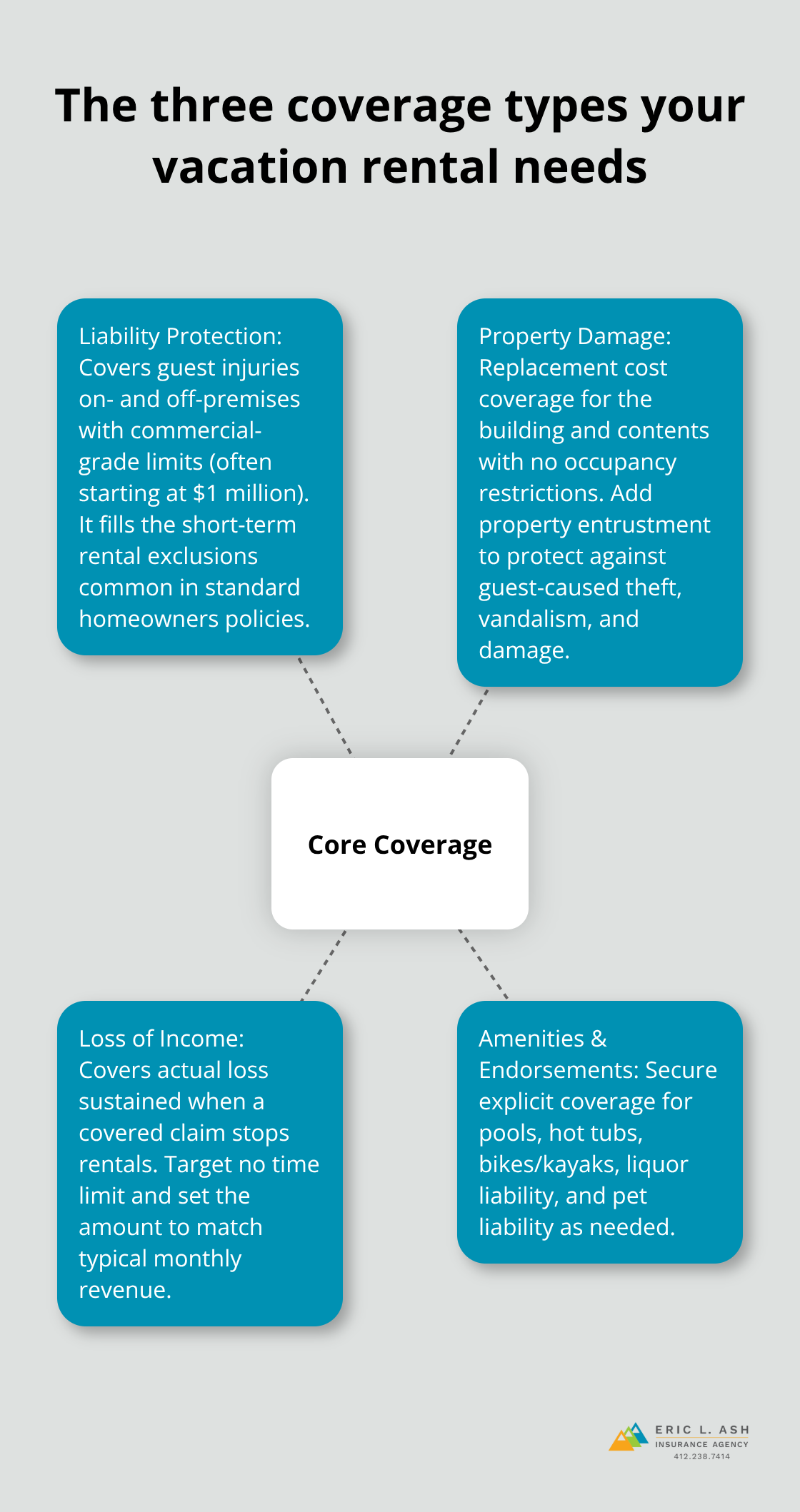

The Three Coverage Types Your Vacation Rental Actually Needs

Liability Protection Stops Guest Injuries From Destroying Your Business

Guest injuries happen more often than most property owners expect. A single slip-and-fall accident on your deck or a guest injured in your hot tub can result in medical bills exceeding $100,000. Standard homeowners policies exclude short-term rental activity, which means you have zero coverage if someone gets hurt during a paid stay. Commercial General Liability coverage starting at $1 million with both on- and off-premises protection forms the baseline for any vacation rental operation.

If your property includes amenities like pools, hot tubs, bikes, or kayaks, you need explicit amenities liability coverage because standard policies often exclude injuries tied to guest-use items. Liquor liability matters too-if you provide alcohol or allow guests to drink on your property, alcohol-related injury claims fall outside typical homeowners coverage and require a specific endorsement.

Property Damage Coverage Protects Your Building and Contents

Property damage coverage protects the actual building and your belongings inside it. Look for Build and Contents Coverage using new-for-old replacement cost with no occupancy restrictions, including periods when the property sits vacant between guests. This matters because many standard landlord policies deny claims if the home is unoccupied, yet vacation rentals frequently have gaps between bookings.

Property entrustment coverage is the piece most hosts overlook-it protects against theft, vandalism, and damage caused by guests themselves, which standard policies often exclude. This endorsement fills a critical gap that leaves many property owners exposed.

Loss of Income Protection Covers Your Revenue When Claims Strike

Loss of income protection is non-negotiable if hosting represents meaningful revenue. Business Revenue Protection should cover actual loss sustained if a covered claim prevents you from renting, with no time limit and coverage up to your chosen amount. A guest causes severe water damage requiring a month of repairs-without loss of income coverage, you absorb that entire month’s lost bookings out of pocket.

When comparing quotes, verify the income protection cap aligns with your typical monthly rental revenue, not just your best month. This alignment ensures you won’t face a shortfall when you need the coverage most. Understanding these three pillars prepares you to evaluate quotes effectively and spot which carriers offer the protection your specific property demands.

How to Get and Compare Vacation Rental Insurance Quotes

Document Your Property and Operations First

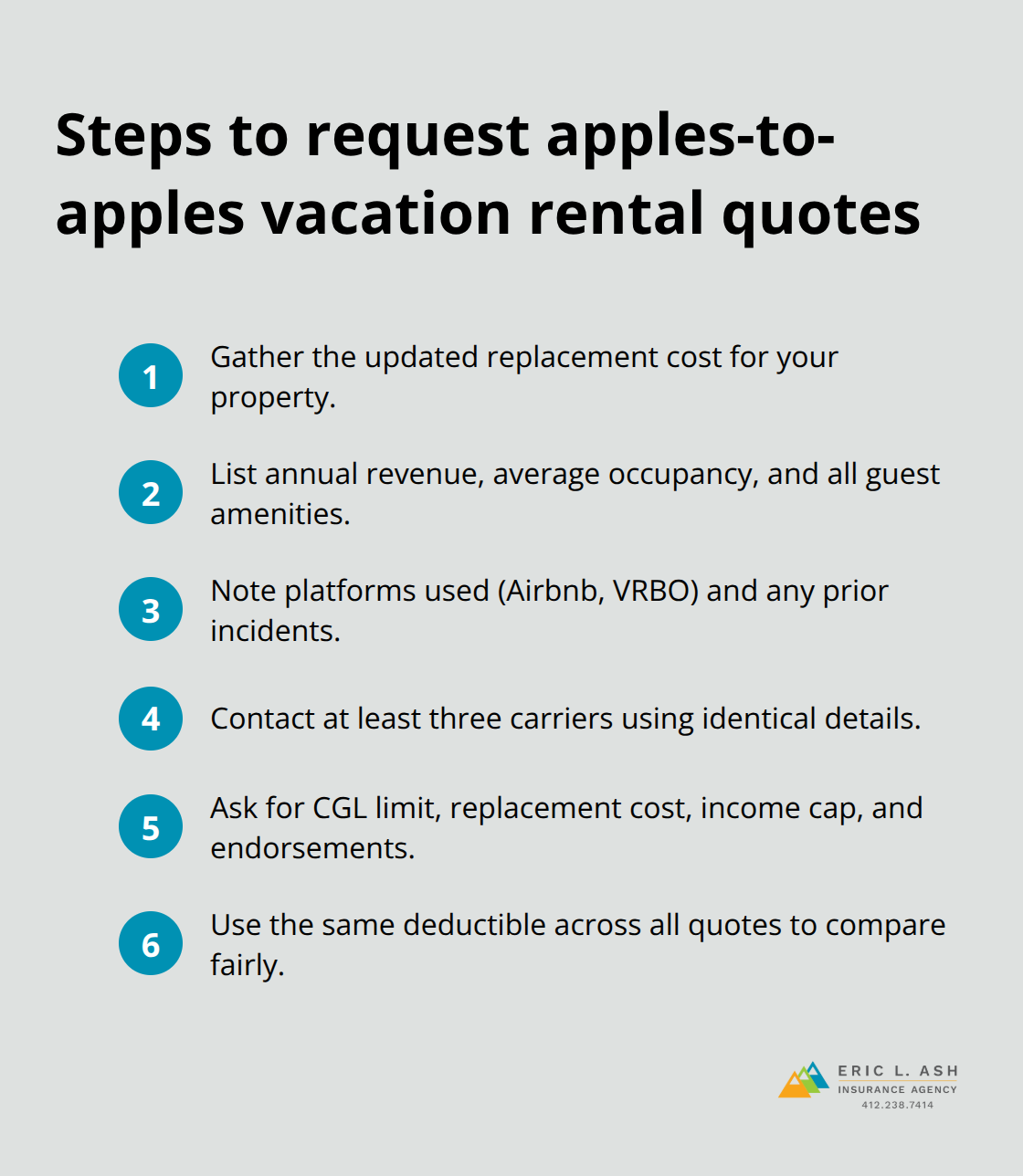

You need accurate information before contacting carriers. List your property’s replacement cost, not what you paid for it years ago-construction costs in Pennsylvania have climbed significantly, and underestimating this number means underinsuring your building. Write down your annual rental revenue, monthly average occupancy rate, and the specific amenities you offer. If you rent through Airbnb, VRBO, or both, note that detail because some carriers price differently based on platform risk profiles. Document any guest incidents from the past year, even minor ones, because underwriters will ask and omissions can void coverage later. Gather information about your local regulations too-Philadelphia’s two-tier licensing system, Pittsburgh’s inspection requirements, or the Pocono region’s occupancy limits all affect your risk profile and should influence the coverage limits you request.

Request Quotes Using Consistent Information

When you reach out to the Eric L. Ash Agency, specify that you need vacation rental coverage, not landlord insurance or standard homeowners protection. Many agents default to cheaper options that exclude short-term rental activity entirely. Ask each carrier for their Commercial General Liability limit, property replacement cost coverage, loss of income protection cap, and any specific endorsements for amenities or pet liability. Request quotes for the same deductible across all three carriers-say $2,500-so you compare apples to apples. We offer dedicated vacation rental policies that typically respond faster and more accurately than agents trying to cobble together coverage from standard products. As an independent agency we shop multiple carriers simultaneously, which saves you time and ensures you don’t miss competitive options in the market.

Compare Coverage Details, Not Just the Premium

Line up the quotes and create a simple spreadsheet comparing liability limits per occurrence, property damage caps, loss of income maximums, and deductibles. A $300 annual premium sounds great until you realize it caps liability at $500,000 when your property exposure demands $1 million. Check whether each policy covers your property during vacant periods-this matters enormously for vacation rentals with booking gaps. Verify that amenities coverage includes off-premises items if you provide kayaks or bikes guests take away from your property. Look at the loss of income coverage carefully; some policies limit payouts to 90 days or cap them at a percentage of annual revenue rather than actual loss sustained. Pennsylvania hosts managing multiple properties should ask about portfolio discounts, which can reduce premiums 10 to 20 percent when you insure several rentals with one carrier. The cheapest quote rarely delivers the best protection, and the most expensive quote often includes coverage you don’t need-your goal is finding the middle ground where premium and protection align with your actual operational risk.

Once you’ve narrowed your options to the top two or three carriers, you’re ready to evaluate the mistakes that trip up most property owners during the final selection process.

Three Ways Hosts Sabotage Their Own Coverage

Most property owners waste time comparing vacation rental quotes only to pick the wrong policy. The culprit isn’t complicated underwriting or confusing policy language-it’s three preventable mistakes that cost hosts thousands in uncompensated losses. The cheapest premium rarely delivers adequate protection, coverage gaps hide in plain sight, and outdated quotes become worthless the moment your business changes. Pennsylvania hosts managing properties across Philadelphia, Pittsburgh, the Pocono region, and beyond face compounding risk when they ignore these traps, especially given the state’s patchwork municipal regulations that can shift your exposure overnight.

Price-Focused Shopping Destroys Adequate Protection

Price-focused shopping destroys more vacation rental operations than any other decision error. A host sees a $400 annual quote and selects it over a $650 option without comparing what each policy actually covers. That $250 savings vanishes the moment a guest suffers a serious injury and the cheaper policy’s $500,000 liability cap proves catastrophically insufficient. Proper Insurance’s commercial-grade policies, backed by Lloyd’s of London, command higher premiums than bare-bones options, but they deliver $1 million liability minimums and business revenue protection without occupancy restrictions-the features that actually matter when claims happen.

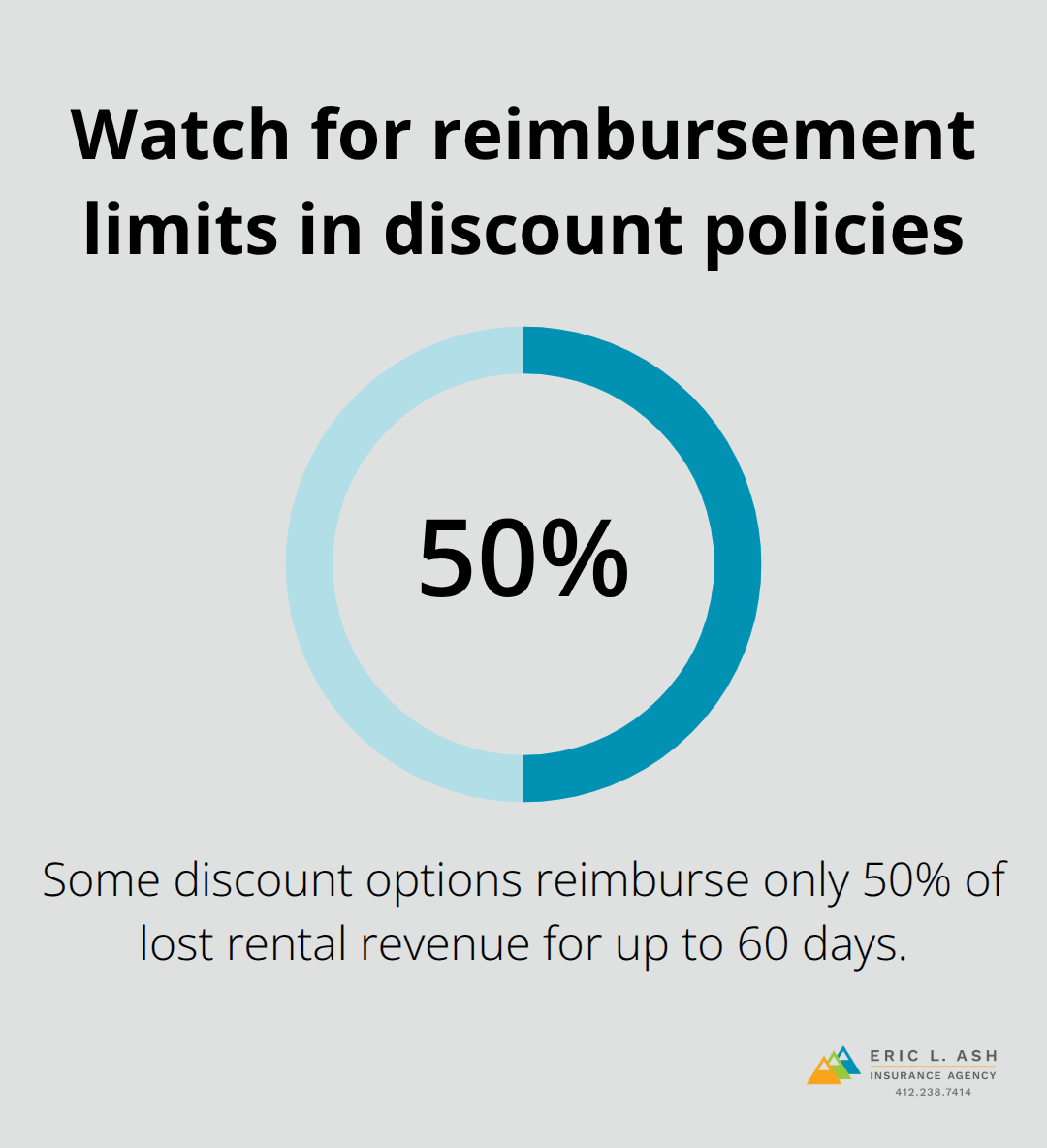

Request specific numbers from each carrier: ask what their liability cap is per occurrence, what they’ll pay if you lose a month of bookings to a water damage claim, and whether they cover your property during the two-week gaps when guests check out and new arrivals haven’t arrived. A policy costing $100 more annually but covering actual loss of income with no time limit outperforms a discount option that reimburses only 50 percent of lost revenue for up to 60 days.

Coverage Gaps Hide in Plain Sight

Exclusions outline what your insurance policy does not cover. You’ll compare three quotes, see that all three mention liability protection, and assume they’re equivalent-then a guest’s dog bites someone and you discover only one policy includes pet liability, while the other two exclude it outright. Property entrustment coverage, which protects against guest-caused damage and theft, appears in comprehensive policies but vanishes entirely from stripped-down offerings.

Amenities coverage for pools, hot tubs, and off-premises items like kayaks varies wildly: some carriers include it automatically, others require expensive endorsements, and a few exclude it completely. Before selecting any policy, create a checklist of your specific exposures-do you provide alcohol, own a hot tub, offer bikes to guests, rent in Philadelphia where zoning violations carry steep penalties, or operate in Pittsburgh where the new Rental Permit Program adds compliance costs? Match that checklist against each quote’s actual coverage language, not the marketing summary.

Outdated Quotes Create False Confidence

Outdated quotes become worse than useless because they create false confidence. You request quotes in January, select a policy in February, and operate all year without revisiting your coverage-then you add a second property, increase your guest count from 20 to 40 bookings monthly, or discover that Pittsburgh’s enforcement of its rental permit program has accelerated. Your original quote assumed single-property operations and moderate occupancy; neither assumption still holds.

Loss of income caps that seemed adequate at 20 bookings per month leave you dramatically underinsured at 40. Some carriers offer portfolio discounts when you add properties, potentially saving 10 to 20 percent on premiums, but you’ll never access that savings if you don’t request updated quotes. Changes in your business-adding amenities, scaling to multiple properties, shifting platforms from Airbnb to VRBO, or relocating to a municipality with stricter regulations-all warrant fresh quotes.

Request new quotes annually even if nothing changes, because carrier appetite for vacation rental business fluctuates and competitors regularly adjust rates and coverage terms. An independent agency that shops multiple carriers can monitor these shifts and alert you when your coverage needs adjustment, eliminating the burden of tracking policy adequacy yourself.

Final Thoughts

Comparing vacation rental insurance quotes comes down to three core principles: prioritize coverage over price, verify that each policy addresses your specific property risks, and refresh your quotes whenever your business changes. The cheapest option rarely protects you adequately, and gaps in coverage often hide in policy language until a claim forces you to find them too late. A $1 million liability limit with business revenue protection and property entrustment coverage outperforms a discount policy that caps liability at $500,000 and excludes guest-caused damage, even if the premium costs more annually.

Your next step is straightforward: gather your property details, occupancy rates, and local regulatory requirements, then request quotes from at least three carriers using identical information. Create a spreadsheet comparing liability limits, property damage caps, loss of income maximums, and deductibles across all three options. Verify that each policy explicitly covers short-term rental activity on your platform and includes endorsements for your specific amenities.

We at Eric L. Ash Insurance Agency shop multiple carriers simultaneously, which means you receive competitive vacation rental insurance quotes without spending hours on the phone with individual insurers. Our agents know which carriers respond fastest to claims, which ones offer portfolio discounts for multiple properties, and which policies actually deliver the protection you need when incidents occur. Contact Eric L. Ash Insurance Agency to request quotes tailored to your property and business model.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.