Vacation Rental Property Insurance: Guarding Your Investment

Owning a vacation rental property in Pennsylvania comes with unique risks that standard homeowners insurance simply doesn’t cover. Guest injuries, property damage from frequent turnover, and liability claims can quickly drain your profits.

Vacation rental property insurance fills those gaps and protects what you’ve built. We at Eric L. Ash Insurance Agency help property owners understand their coverage options and find the right policy for their specific situation.

Why Your Homeowners Policy Won’t Protect Your Rental

Standard Homeowners Insurance Excludes Rental Activity

Your standard homeowners insurance policy was designed for one thing: protecting a house where you live. The moment you start renting it out to guests, even for just a few nights, that policy becomes nearly worthless. Most homeowners policies explicitly exclude short-term rental activity, and many insurers will outright deny claims if they discover you operate a vacation rental. This isn’t a gray area or a technicality you can work around. It’s a hard line that separates residential coverage from commercial activity.

Guest Liability Exposes You to Massive Claims

Standard homeowners policies cap liability coverage at around $100,000 to $300,000, which sounds like protection until a guest gets seriously injured on your property. A slip on wet stairs, a fall from a deck, or a pool accident can easily generate medical bills and legal settlements that exceed these limits. Pennsylvania courts have awarded substantial damages in premises liability cases, and a single incident can wipe out years of rental income. What makes this worse is that your homeowners policy doesn’t account for the constant stream of strangers moving through your property. Each guest represents a new liability exposure that traditional policies never contemplated. Your insurer expects you to know the people in your home. With vacation rentals, you don’t.

Property Damage Accelerates With Frequent Turnover

Short-term rental properties experience dramatically higher rates of damage compared to long-term rentals or owner-occupied homes. Guest turnover means constant wear on appliances, flooring, and furnishings. A family checks out Friday morning and a different family checks in Friday afternoon. That’s 365 potential turnover events per year if your property books solid. Each transition creates opportunities for damage: broken dishes, stained furniture, damaged door locks, and wear on plumbing fixtures.

Water damage from burst pipes or appliance leaks historically ranks as the most expensive property damage claim in rental situations, and frequent guest use accelerates the failure of water-using equipment. Standard homeowners policies do cover some water damage, but they exclude damage from lack of maintenance or gradual wear-exactly what accumulates in high-turnover rental properties. Furnishings in vacation rentals wear out three to five times faster than in owner-occupied homes, yet standard policies treat them no differently than permanent home fixtures. Your $15,000 furniture investment depreciates rapidly under guest use, but your homeowners policy won’t replace it at current replacement cost when damage occurs.

Why Vacation Rental Insurance Fills the Gaps

The coverage gaps in standard homeowners policies create real financial exposure for Pennsylvania property owners. Vacation rental insurance addresses these gaps with protections specifically designed for short-term rental operations. The right policy covers liability claims from guest injuries, property damage from frequent turnover, and loss of rental income when your property becomes uninhabitable. Understanding what vacation rental insurance actually covers helps you make informed decisions about protecting your investment.

What Vacation Rental Insurance Actually Protects

Liability Coverage Shields You From Guest Injuries

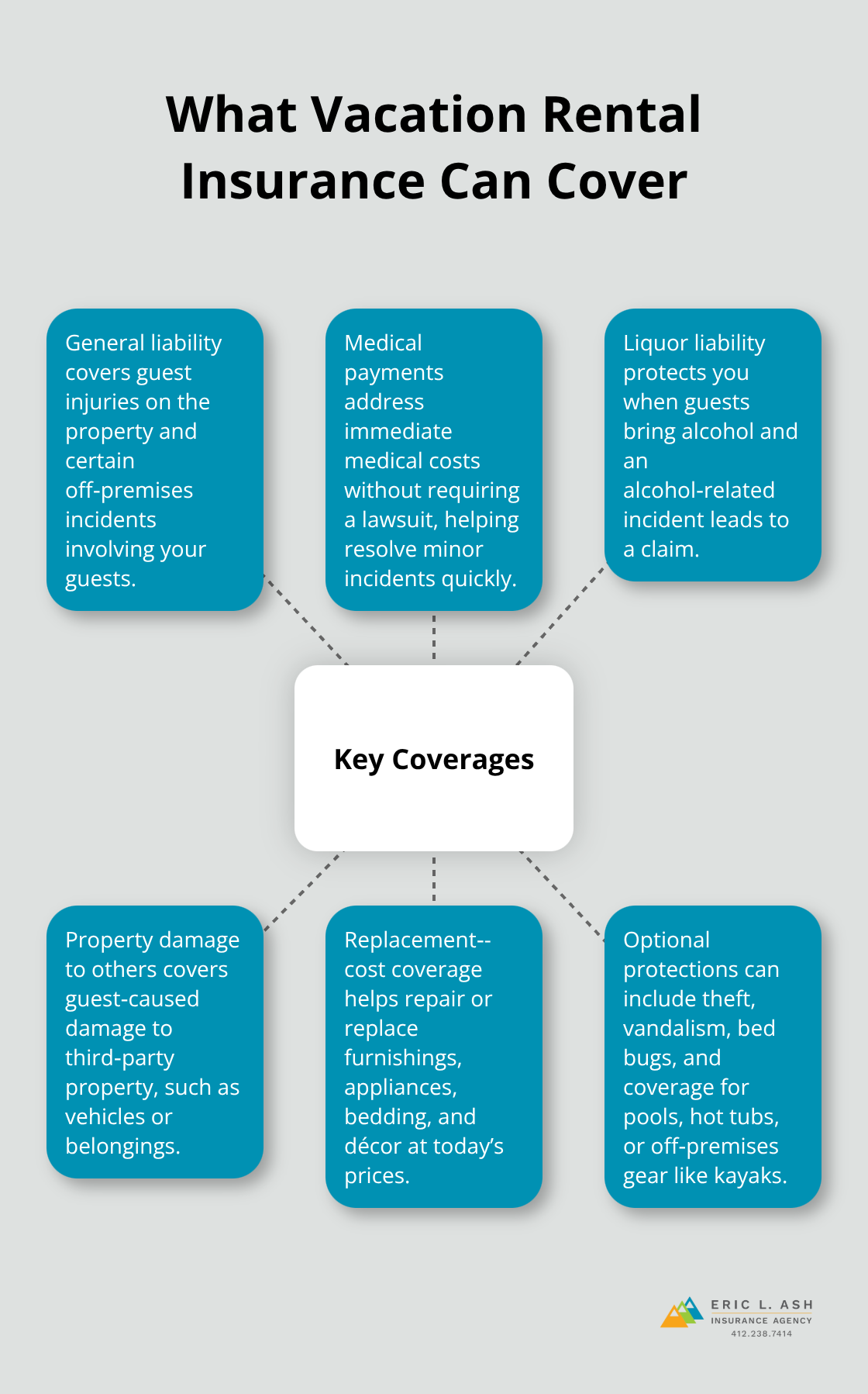

Vacation rental insurance protects you when someone gets injured on your property and sues. A visitor slips on your deck, a child drowns in your pool, or a guest suffers food poisoning from your kitchen-these situations generate medical bills, legal defense costs, and settlement payments that can reach six figures. Vacation rental insurance typically starts with general liability coverage, which addresses both on-premises injuries and off-premises incidents involving your guests. Pennsylvania courts have consistently awarded substantial damages in premises liability cases, making robust coverage essential.

Your policy should include liquor liability coverage if you allow guests to bring alcohol, since alcohol-related incidents are commonly excluded from standard homeowners policies. Medical payments coverage, separate from liability, covers immediate medical expenses for guest injuries without requiring a lawsuit, which often resolves minor incidents faster and cheaper than litigation. Property damage coverage within your liability section protects you if a guest damages someone else’s property-for example, a guest’s car gets hit in your driveway or someone’s belongings get damaged during their stay.

Choosing the Right Liability Limits for Your Property

Most carriers offer $300,000 to $1 million in liability limits, and the right amount depends on your property’s guest capacity and amenities. A small cabin with two bedrooms needs less liability coverage than a six-bedroom house with a pool, hot tub, and fire pit. Higher-capacity properties with more guests and amenities create greater exposure to injury claims, which justifies higher liability limits.

Property Damage Coverage Protects Your Furnishings and Equipment

Water damage from burst pipes or appliance failures ranks as the most expensive claim type in short-term rentals, and your vacation rental policy covers these incidents with replacement-cost coverage rather than depreciated value. Furnishings and equipment coverage protects your furniture investment, kitchen appliances, bedding, and décor at current replacement cost, which matters because guest use accelerates wear significantly. Some policies include theft and vandalism coverage for guest-caused damage, bed bug and flea protection covering extermination costs and lost revenue during treatment, and coverage for amenities like pools, hot tubs, and off-premises equipment such as kayaks or bicycles.

Loss-of-Income Coverage Protects Your Cash Flow

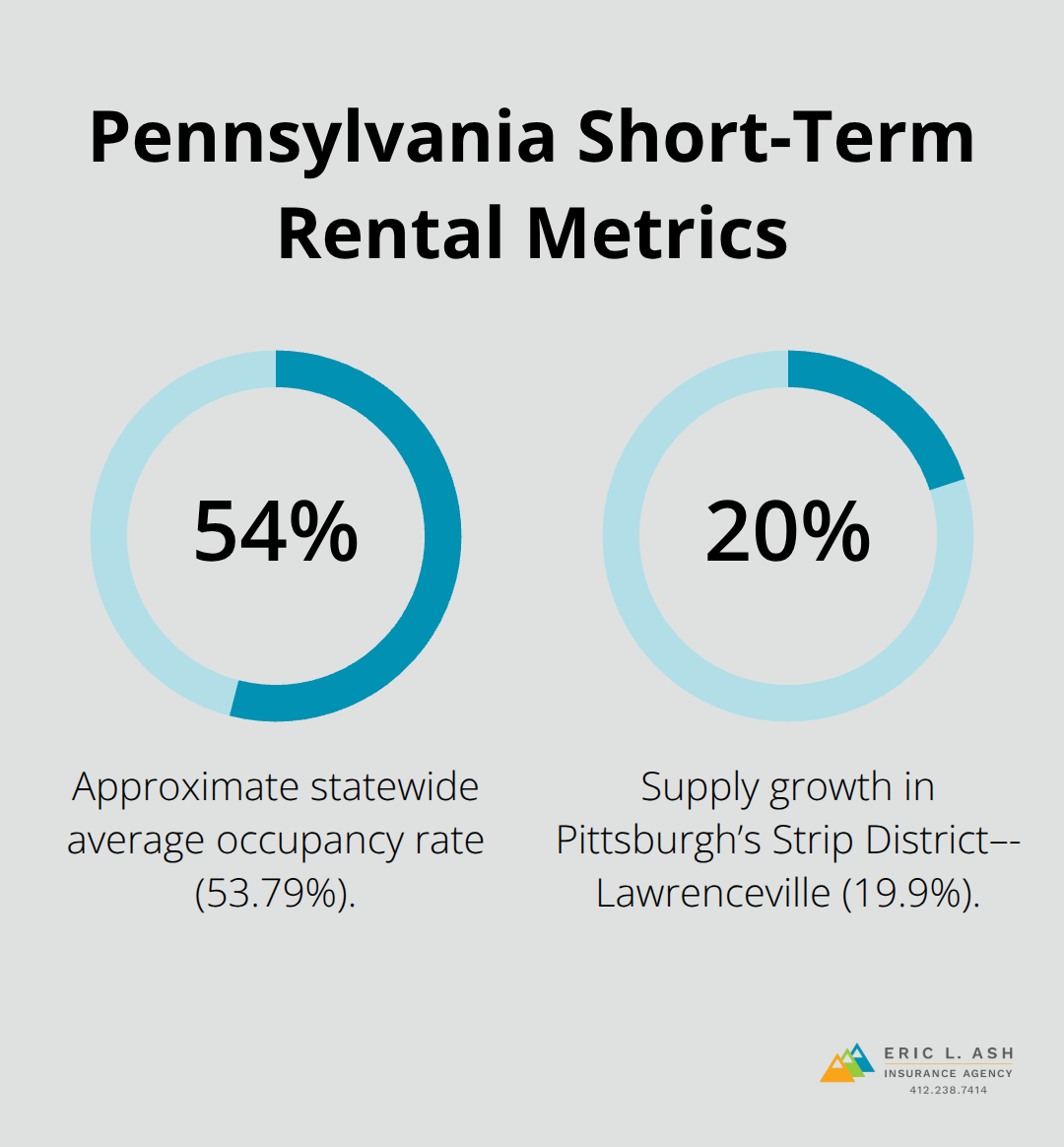

Loss-of-rental-income coverage reimburses you when a covered peril makes your property uninhabitable-a kitchen fire, major water damage, or structural damage prevents guest bookings until repairs complete. This coverage pays your actual lost revenue with no time limit in many policies, which protects your cash flow during recovery. Pennsylvania’s short-term rental market shows average daily rates ranging from $127 in Philadelphia to $342 in the Poconos, with average annual revenue around $41,490 statewide, so your loss-of-income limit should reflect your property’s actual earning potential.

Higher-value properties in markets like State College, where average daily rates hit $290, need correspondingly higher income protection limits. Deductibles typically range from $500 to $2,500, and choosing a higher deductible lowers your premium but increases your out-of-pocket cost after a claim. The trade-off works best when you have cash reserves to cover the deductible and when your property generates enough income to justify premium savings.

The specific protections your policy offers depend on the carrier and the endorsements you select. Comparing what different insurers cover-and what they exclude-reveals significant differences in how well each policy actually protects your investment.

How to Choose the Right Vacation Rental Insurance for Your Pennsylvania Property

Calculate Your Actual Replacement Costs

Walk through your rental property and price out what it would cost to replace everything if a fire destroyed it completely. Document your furniture, appliances, electronics, kitchen equipment, bedding, and décor with photos and current retail prices. This exercise reveals the true value you need to protect, not a generic estimate that leaves gaps when you file a claim.

Pennsylvania vacation rental properties average annual revenues between $28,459 in Philadelphia and $58,774 in the Poconos according to Airbtics’ 2025 market data. Your loss-of-income coverage should reflect your specific property’s earning potential, not a number pulled from thin air. If your property books at a $212 average daily rate with 53.79% occupancy statewide, you protect roughly $41,490 in annual revenue. A property in State College with a $290 daily rate needs significantly higher income protection limits than a Philadelphia property at $127 per night.

Match Liability Coverage to Your Guest Capacity and Amenities

Your property’s guest capacity and amenities directly influence liability exposure. A two-bedroom cabin with no pool needs less liability coverage than a six-bedroom house with a hot tub and fire pit where eight guests gather nightly. Properties in higher-traffic urban markets like Pittsburgh’s Strip District-Lawrenceville, which show 19.9% supply growth, experience more guest incidents, so maintaining strong general liability and medical payments coverage matters more as your market becomes more competitive and guest turnover accelerates.

Request Detailed Quotes From Multiple Insurers

Contact multiple insurers and request detailed quotes that show exactly what each policy covers and excludes. Ask specifically about bed bug and flea protection, theft by guests, and coverage for off-premises amenities like kayaks or bicycles if your property offers them. Proper Insurance, endorsed by VRBO, offers commercial general liability starting at $1 million with no occupancy restrictions and covers bed bugs, squatters protection, and liquor liability as standard features.

Choose Your Deductible Based on Cash Reserves

Your deductible choice significantly impacts your premium and claim costs. A $500 deductible costs more monthly but saves money if you file claims; a $2,500 deductible cuts your premium substantially but requires cash reserves to cover that amount out of pocket after a loss. Choose the higher deductible only if you have adequate emergency funds and your property generates enough income to absorb the extra expense.

Verify Coverage Requirements for Extended Stays

Request certificates of insurance from any renter or guest who books extended stays, and verify that your policy requires guests to carry their own liability insurance for high-value rentals where someone else’s negligence could damage your property. Vacation rental insurance is specifically designed to protect your property, income, and liability risks when you work with an independent insurance agency throughout Pennsylvania to compare quotes across multiple carriers and identify which policy actually protects your specific property rather than offering generic coverage that leaves gaps.

Final Thoughts

Protecting your Pennsylvania vacation rental property requires more than hoping your homeowners policy covers guest injuries or property damage. The gaps are real, the financial exposure is substantial, and the right vacation rental property insurance fills those gaps with protections specifically designed for short-term rental operations. You need liability coverage that accounts for constant guest turnover, property damage protection that replaces furnishings at current cost rather than depreciated value, and loss-of-income coverage that reflects your property’s actual earning potential in Pennsylvania’s diverse rental markets.

Calculate your replacement costs by walking through your property and pricing everything you would need to replace after a total loss. Match your liability limits to your guest capacity and amenities, not to a generic number that may leave you underinsured. Request detailed quotes from multiple carriers and compare what each policy actually covers and excludes, paying special attention to bed bug protection, guest theft coverage, and amenities like pools or hot tubs that increase your liability exposure.

Your deductible choice matters more than most property owners realize, since a higher deductible cuts your premium but requires cash reserves to cover that amount out of pocket after a claim. Working with a local insurance agency gives you access to multiple carriers and someone who understands Pennsylvania’s rental market variations (properties in Philadelphia face different risks than properties in the Poconos or State College). Contact Eric L. Ash Insurance Agency to discuss your specific property and receive quotes that actually protect your investment.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.