Rental Property Coverage PA: Comprehensive Protection for Your Vacation Rental

Renting out your home in Pennsylvania can generate steady income, but standard homeowners insurance won’t protect your investment. Most policies explicitly exclude rental activity, leaving you exposed to significant financial risk.

We at Eric L. Ash Insurance Agency see this problem regularly. You need rental property coverage PA that’s specifically designed for your situation, whether you’re running a short-term vacation rental or managing long-term tenants.

Why Standard Homeowners Insurance Won’t Cover Your Rental Property

Coverage Gaps When You Rent Out Your Home

Standard homeowners insurance in Pennsylvania explicitly excludes rental activity, and insurers take this seriously. If you rent out your property-whether for a week or a year-your policy will not cover damage, theft, or liability claims. Most insurers will either deny your claim outright or cancel your policy once they discover you operate a rental. This isn’t a gray area. The Insurance Services Office, which drafts standard policy language used across the industry, classifies rental properties as commercial activities that fall outside homeowners coverage. Your insurer doesn’t care if you rent occasionally or full-time; the exclusion applies either way.

Guest Liability Exposure and Financial Risk

When a guest gets injured on your rental property, your homeowners policy will not defend you. If a fire damages the structure while tenants occupy it, you remain uninsured. If someone steals from the property or causes intentional damage, you absorb the loss yourself. One common scenario involves a guest slipping on a wet floor and filing a lawsuit for medical bills and pain-and-suffering damages. Homeowners liability coverage simply does not apply to rental operations. You could face a significant judgment with no insurer backing your defense-a financial hit that most property owners cannot absorb without serious consequences.

Policy Cancellation if Insurers Discover Rental Activity

Insurance companies monitor claims and property usage patterns closely. If you file a claim related to rental activity-say, water damage that occurred while guests stayed on the property-the insurer investigates your policy’s actual use versus what you stated at application. They review your mortgage documents, property tax records, and even online rental listings to verify whether rental activity exists. Once discovered, most insurers issue a cancellation notice with 30 days to find new coverage. In Pennsylvania, this cancellation gets reported to the state’s insurance database, making it harder to obtain standard homeowners coverage elsewhere (some insurers will offer a grace period to switch to a landlord or short-term rental policy, but others simply terminate).

Rental property insurance in Pennsylvania addresses these exposures directly with coverage designed for commercial use, loss of income protection, and guest-related liabilities that homeowners policies explicitly exclude. Understanding what landlord and rental property insurance actually covers helps you make an informed decision about protecting your investment.

What Rental Property Insurance Actually Protects

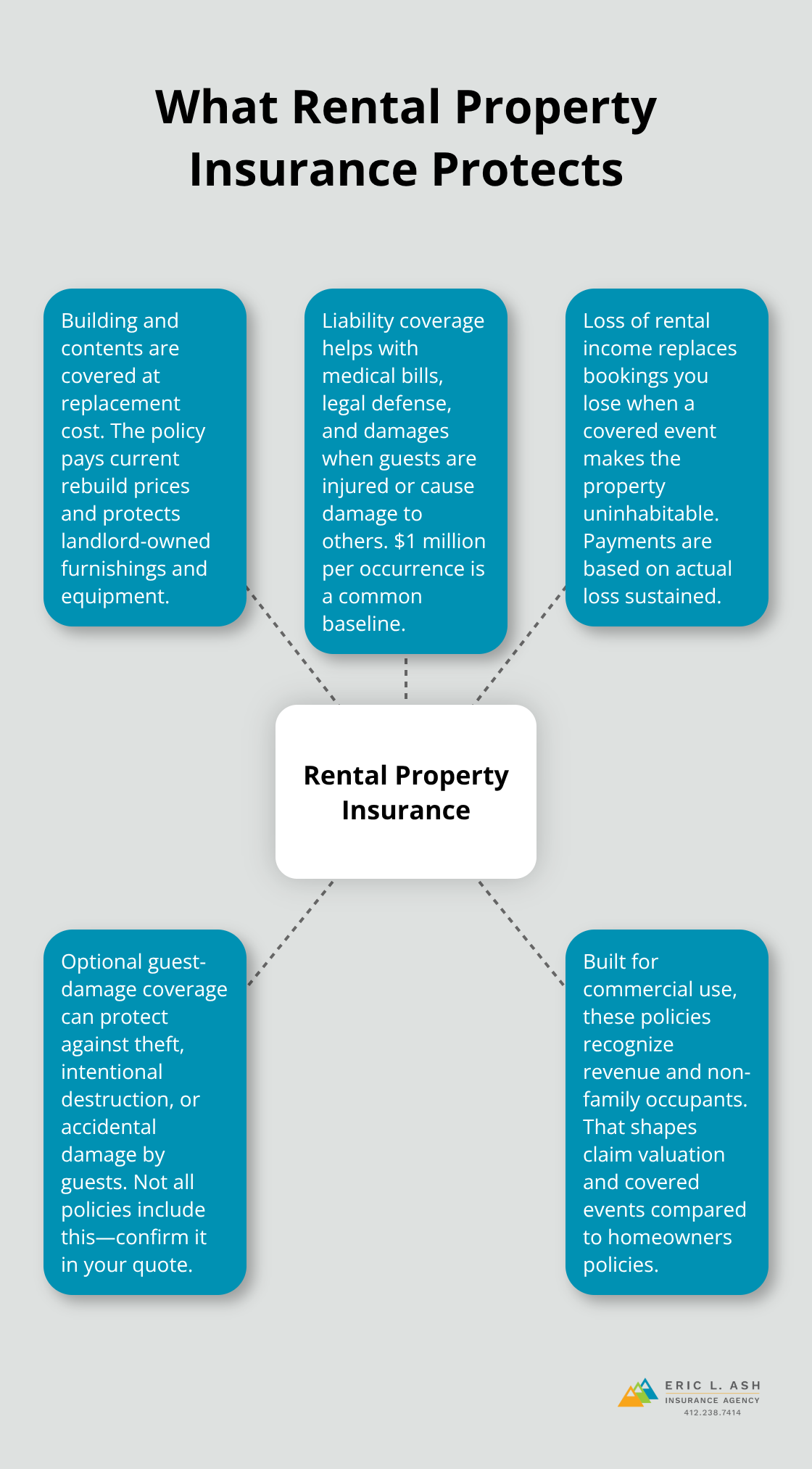

Rental property insurance in Pennsylvania fills the gaps that homeowners policies intentionally leave open. The coverage is built for commercial use, meaning it protects your building, contents, liability exposure, and income stream when guests or tenants occupy your property. Unlike standard homeowners insurance, rental policies acknowledge that your property generates revenue and that people other than family members will live there or visit temporarily. This fundamental difference shapes every aspect of the coverage, from how claims are valued to what events trigger payment. Rental property insurance costs more than homeowners coverage, but that premium buys protection that actually applies when you need it.

Building and Contents Protection at Replacement Cost

Your rental property policy covers structural damage from fire, wind, theft, and vandalism at replacement cost, meaning the insurer pays what it costs to rebuild or repair today, not the depreciated value. If a fire destroys the roof and second floor, the policy reimburses the full cost of new materials and labor to restore the structure to pre-loss condition.

Contents coverage protects your landlord-owned furnishings, appliances, and equipment inside the rental unit. Replacement cost matters significantly in Pennsylvania, where construction costs have risen steadily. A 2,000-square-foot vacation rental that cost $150,000 to build ten years ago might cost $220,000 to rebuild today.

You must set your coverage limits to reflect current replacement values, not the original purchase price or what you paid for improvements years ago. Review your coverage limits annually and adjust them upward if you’ve added appliances, updated kitchens, or installed new systems. Underinsurance is common and leaves you paying the difference out of pocket when a loss occurs.

Liability Coverage When Guests Are Injured or Property Is Damaged

General liability coverage on a rental property typically starts at $1 million per occurrence and covers medical bills, legal defense, and damages when a guest gets hurt on your property or causes damage elsewhere. If a guest slips on stairs and breaks their leg, your liability coverage pays their medical expenses and any court judgment up to your policy limit. If a guest damages a neighbor’s fence or vehicle while staying at your rental, that coverage applies too.

Pennsylvania courts award substantial damages in injury cases, particularly when negligence is clear. Slip-and-fall settlements in Pennsylvania typically range from $125,000 to $175,000, though cases involving permanent injury can exceed these amounts significantly when medical costs, lost wages, and pain-and-suffering are included. One million dollars in liability coverage is the industry standard for a reason, and it’s the minimum we recommend for any rental property in Pennsylvania. Some policies also include coverage for damage caused by guests to your own property, protecting against theft, intentional destruction, or accidental damage that guests cause. This guest-damage coverage is not universal, so verify it’s included in your quote.

Income Protection When Covered Events Prevent Rentals

Loss of rental income coverage reimburses you for bookings you lose when a covered event makes your property uninhabitable. If a fire damages the kitchen and you must cancel reservations for three months while repairs are completed, this coverage pays the rental income you would have earned during that period. The payment is based on actual loss sustained, calculated from your booking history and nightly rates.

Pennsylvania rental properties generate between $200 and $500 per night on average depending on location and season, according to vacation rental platform data. A three-month loss of income could represent $18,000 to $45,000 in uncovered expenses without this protection. Some policies limit the payout period, but the best rental policies pay actual loss sustained with no time limit, as long as the property remains uninhabitable due to the covered claim. This coverage protects your cash flow and prevents you from taking on debt to cover mortgage and property tax payments while the property sits empty during repairs.

The specific coverages available to you depend on your property type, location within Pennsylvania, and the carriers you work with. Short-term vacation rentals and long-term tenant properties often qualify for different policy structures and optional add-ons, which is why finding the right coverage requires understanding what options exist in your market.

How to Choose the Right Rental Insurance for Your Pennsylvania Property

Match Your Policy to Your Rental Model

The insurance you select depends entirely on how you operate your rental. Short-term vacation rentals and long-term tenant properties have fundamentally different risk profiles, which means they require different policy structures. A short-term rental exposes you to transient guests, frequent turnover, and concentrated liability from multiple occupants in a short window. Long-term tenant properties spread risk across fewer people over an extended period, reducing certain exposures while creating others like tenant-related disputes. The policy you buy must match your actual rental model, not a generic version that tries to cover both.

Short-term rental policies typically include coverage for loss of bookings, guest damage, and amenities liability that long-term policies exclude. Long-term landlord policies emphasize tenant-related exposures and often include optional crime coverage for theft by occupants. Proper Insurance has built short-term rental policies specifically for Airbnb and Vrbo hosts, covering bed bug liability, squatter protection, and revenue loss from canceled bookings. If you operate a long-term rental, Distinguished offers specialized landlord programs for two to 100 units with equipment breakdown coverage and ordinance upgrades that address aging Pennsylvania buildings. Mixing these policy types or selecting a generic commercial policy wastes money and leaves you exposed.

Shop Multiple Carriers for Competitive Rates

Shopping multiple carriers is not optional if you want competitive rates. Pennsylvania landlord insurance premiums vary significantly by location, property type, and condition, and obtaining quotes from a single carrier leaves you paying inflated prices. Independent agents like Gibbel Insurance access multiple carriers and tailor coverage across different underwriters to find the best combination of price and protection. As a veteran-owned, independent insurance agency in Pennsylvania, Eric L. Ash Insurance Agency leverages relationships with dozens of carriers to shop multiple markets and deliver competitive rates backed by responsive local service.

When you request quotes, have your property details ready: the property address and municipality (since Pennsylvania municipalities impose different regulations), the building square footage and age, the number of units, whether you occupy the property yourself, your target rental platform, and your desired coverage limits. Quotes cannot be bound online; a licensed agent must confirm final policy terms after underwriting, so expect the process to take 24 to 48 hours for a complete quote. Avoid sharing your information with multiple brokers simultaneously, as each inquiry may trigger a credit inquiry and multiple quotes can confuse your comparison. Instead, work with a single agent who can present options from multiple carriers in a structured format.

Understand Pricing and Tax Deductions

The best rental property policies in Pennsylvania cost between 1.5 and 3 percent of your property’s insurable value annually, depending on the property type and location. A $200,000 vacation rental might cost $3,000 to $6,000 per year in premiums, while a $500,000 multi-unit building could cost $7,500 to $15,000. These costs are tax-deductible as business expenses if your rental generates income, so factor that into your decision.

Navigate Pennsylvania’s Local Regulations

Working with a local agent who understands Pennsylvania’s decentralized rental regulations saves you from costly compliance mistakes. Pennsylvania does not define short-term rentals statewide, so Philadelphia, Pittsburgh, the Poconos, and Lancaster County each impose different requirements for licensing, occupancy limits, and tax collection. An agent familiar with your specific municipality can confirm whether your rental complies with local zoning and safety codes, which affects both your insurability and your policy limits. If your property is in a historic district or an area with HOA restrictions, a local agent identifies these issues before you buy coverage that won’t apply.

Pennsylvania’s hotel occupancy tax is 6 percent statewide, but counties add their own lodging taxes, bringing total rates to 7 to 9 percent in most areas. Philadelphia’s combined tax burden reaches 14.5 percent, which means a $10,000 booking generates $1,450 in taxes you must remit. An agent with local expertise ensures your loss of income coverage reflects your actual after-tax revenue, not gross bookings. They also confirm whether your insurer will issue a quote for your property type in your specific location, since some carriers exclude certain Pennsylvania municipalities or property conditions.

Verify Safety Requirements Before Applying

Short-term rental insurers in Pennsylvania typically require smoke detectors, carbon monoxide alarms, and fire extinguishers to bind coverage. A local agent verifies these requirements upfront and helps you understand what upgrades your property needs before applying for a quote.

Final Thoughts

Your rental property in Pennsylvania generates income only when proper coverage protects it. Standard homeowners insurance excludes rental activity entirely, leaving you exposed to guest injuries, property damage, and lost bookings that can devastate your finances. Rental property coverage PA addresses these gaps with policies built specifically for how you operate your property, whether you run a short-term vacation rental or manage long-term tenants.

The right policy matches your rental model and reflects Pennsylvania’s local regulations. Short-term rentals need guest damage protection and loss of bookings coverage, while long-term properties need tenant-related liability and equipment breakdown protection for aging systems. An independent agent familiar with your specific municipality confirms compliance with local codes and ensures your coverage limits reflect actual replacement costs and after-tax rental income.

We at Eric L. Ash Insurance Agency work with multiple carriers to deliver competitive rates tailored to your property type and location. Contact us today for a quote and protect your rental investment with coverage that actually applies when you file a claim.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.