Small Business Commercial Auto: Affordable Auto Insurance

Running a small business means managing countless expenses. Your vehicles are essential to operations, but the wrong insurance choice can drain your budget or leave you exposed to serious liability.

We at Eric L. Ash Insurance Agency help small business owners find commercial auto coverage that actually fits their finances. This guide shows you how to secure affordable protection without cutting corners on what matters.

Why Your Business Vehicles Need Commercial Coverage

Personal auto insurance won’t cover your business vehicles, and operating without proper commercial auto coverage exposes you to financial ruin. Most states legally require liability coverage for any vehicle used for business purposes, whether you own it, lease it, or occasionally use a personal vehicle for work. Citations for operating without commercial auto insurance result in fines ranging from hundreds to thousands of dollars, depending on your state, plus potential license suspension and vehicle impoundment. More importantly, if an accident occurs and you lack coverage, you become personally liable for medical bills, property damage, lost wages, and legal fees-costs that can easily exceed six figures and bankrupt a small operation.

The Real Cost of an Uninsured Accident

A single accident involving your business vehicle can destroy your finances. If your driver injures someone, medical expenses for spinal injuries, brain trauma, or permanent disability often exceed $100,000. Property damage claims add up fast: rear-ending another vehicle, hitting a storefront, or damaging commercial equipment can easily cost $20,000 to $50,000 in repairs and liability. Without commercial auto coverage, you pay these costs from your business bank account or personal assets. Courts can garnish your wages, seize equipment, and force you to liquidate inventory to settle judgments. Litigation funding in auto liability cases has also become common, meaning third-party financiers back lawsuits against drivers and businesses, pushing settlements into seven figures. One accident without insurance typically ends small businesses.

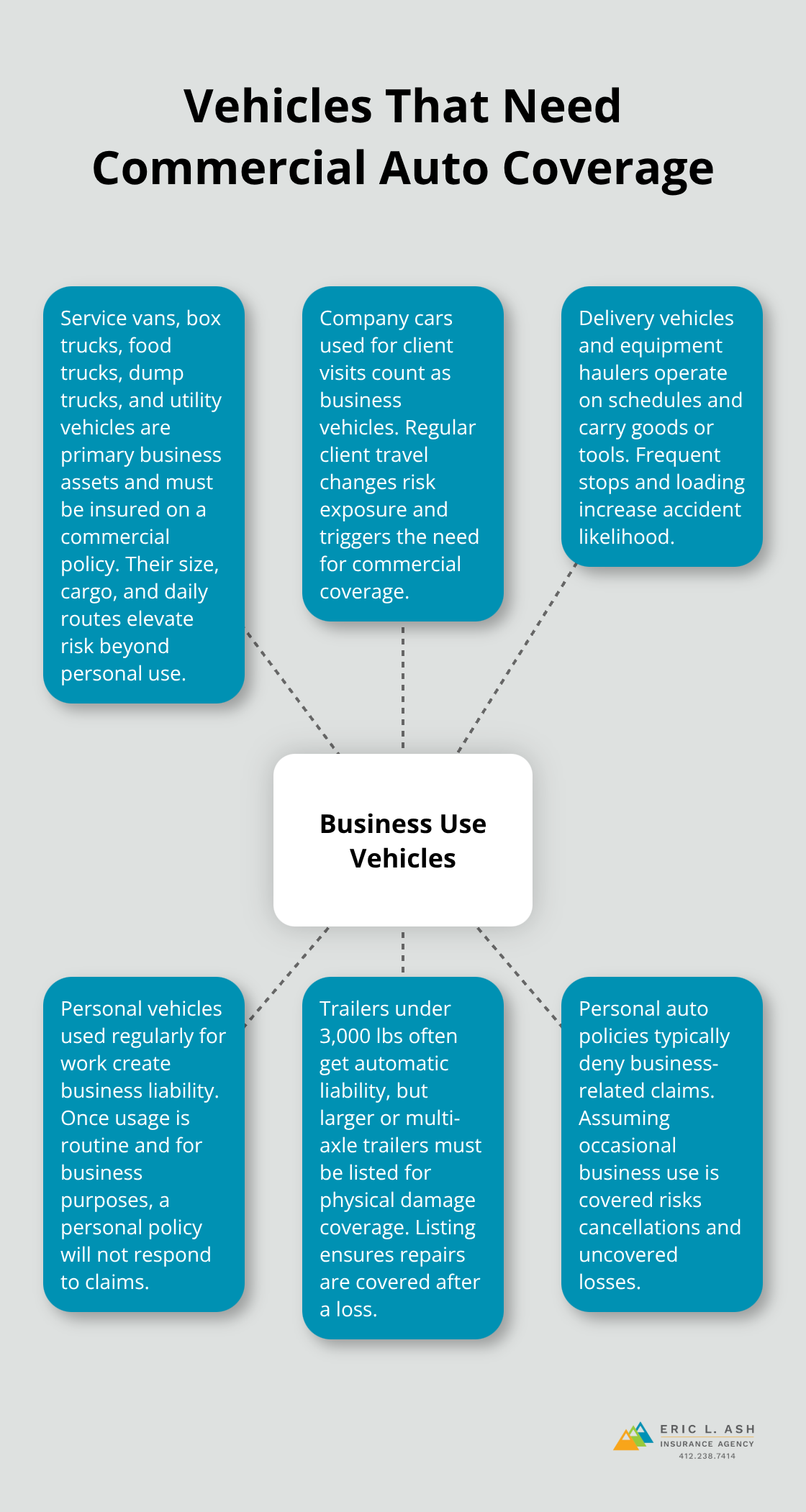

What Vehicles Actually Need Commercial Coverage

Service vans, box trucks, food trucks, dump trucks, utility vehicles, and any vehicle regularly used for business operations require commercial auto insurance. This includes company cars used to visit clients, delivery vehicles, vehicles hauling equipment or materials, and even personal vehicles if you use them for regular business activities. Trailers under 3,000 pounds receive automatic liability coverage under most commercial policies, but trailers larger than 3,000 pounds or multi-axle trailers must be specifically listed on your policy to receive physical damage coverage.

Many small business owners mistakenly assume their personal auto policy covers occasional business use-it doesn’t, and filing a claim for business-related accidents often results in denial and policy cancellation. The distinction is clear: if the vehicle serves a business purpose beyond commuting to a single workplace, you need commercial auto insurance.

Why Personal Policies Fall Short

Your personal auto policy explicitly excludes business use. Insurance companies investigate claims carefully, and they deny coverage when they discover business activity. This denial leaves you uninsured at the exact moment you need protection most. The insurer may also cancel your entire personal policy for misrepresenting the vehicle’s use, leaving you scrambling to find coverage elsewhere. State regulators and insurers take this seriously because business vehicles operate at higher risk than personal commuter cars. Your personal policy simply wasn’t priced or designed to handle the exposure that comes with business operations.

How to Determine Your Coverage Needs

Start by listing every vehicle your business operates or controls. Include company-owned vehicles, leased equipment, and personal vehicles your employees drive for work. Next, identify how each vehicle is used: local deliveries, long-distance hauling, client visits, equipment transport, or service calls all carry different risk profiles. Vehicles with higher mileage, longer routes, or multiple drivers typically cost more to insure because they face greater exposure. Your industry also matters-construction fleets, food service vehicles, and delivery operations all present distinct risks that affect pricing and available coverage options. Once you understand your fleet’s composition and usage patterns, you can work with an independent agent to select the right commercial auto policy.

Finding the Lowest Rates Without Sacrificing Coverage

Get Multiple Quotes to Expose Price Gaps

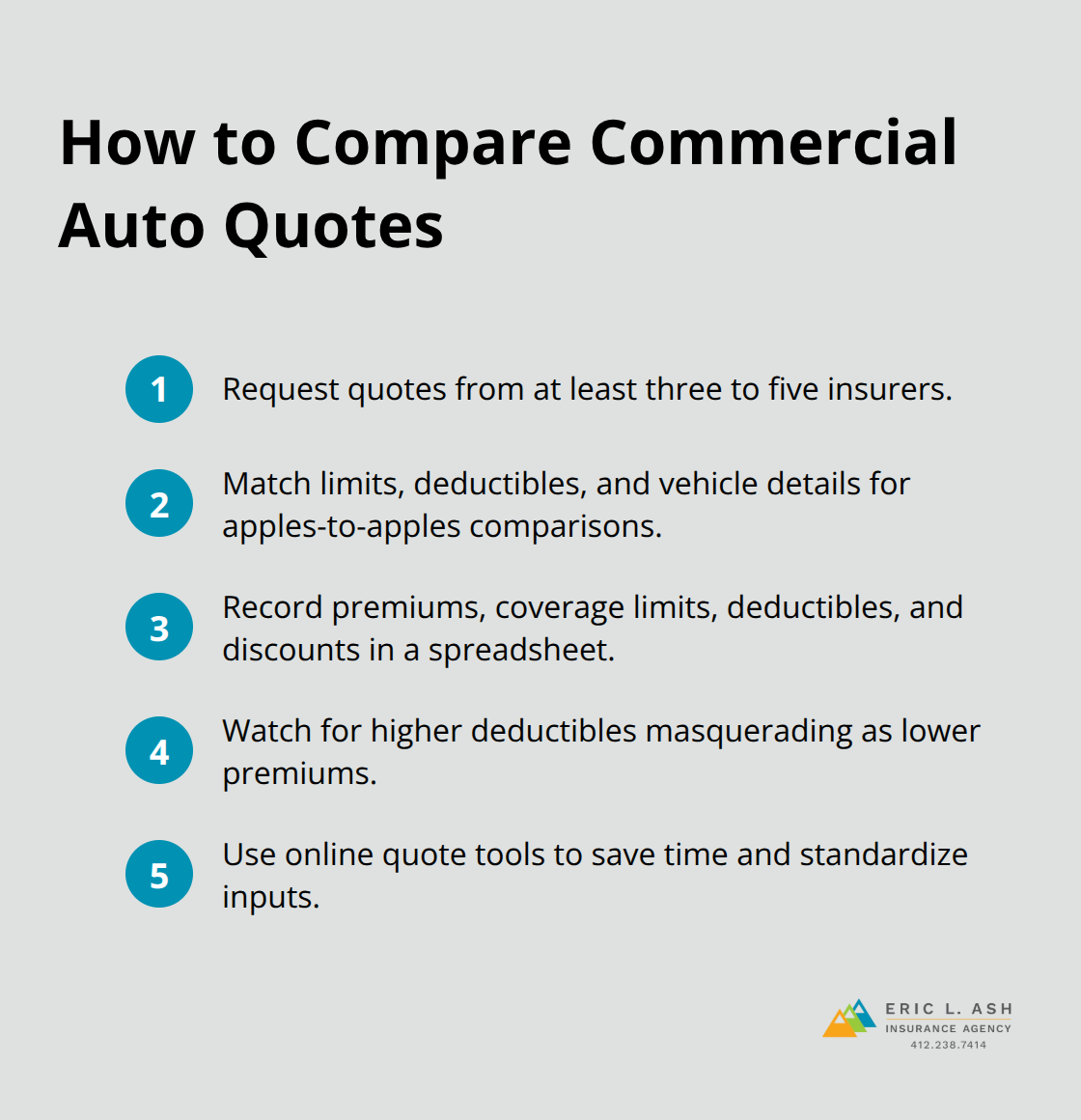

Getting multiple quotes is non-negotiable if you want affordable commercial auto insurance. Most small business owners request one quote, assume that’s the market rate, and move forward-a costly mistake. Commercial auto rates vary dramatically between carriers because each insurer weighs risk differently. One carrier might charge $1,200 annually for a service van with one driver, while another charges $1,800 for identical coverage. The only way to find competitive pricing is to request quotes from at least three to five different insurers. This takes 30 minutes of your time and can save you hundreds of dollars per year.

Many carriers now offer online quote tools that let you input your fleet details once and see rates immediately, removing the excuse of inconvenience. When you gather quotes, make sure you compare apples to apples-same coverage limits, same deductibles, same vehicle types. A quote that looks cheaper because it has a $2,500 deductible instead of $1,000 isn’t actually cheaper if an accident forces you to pay more out of pocket. Track each quote in a spreadsheet with the carrier name, premium, coverage limits, deductible amounts, and any discounts applied. This comparison document becomes your negotiating tool.

Stack Discounts on Top of Bundle Savings

Bundling your commercial auto policy with other business insurance cuts premiums significantly. If you carry general liability, property insurance, or workers’ compensation, adding commercial auto to the same carrier typically saves 10 to 25 percent on your total premium. Carriers offer bundle discounts because they want to consolidate your business and reduce their acquisition costs. A small business paying $800 for general liability and $1,500 for commercial auto separately might pay $1,900 total when bundled with one insurer instead of $2,300 with separate carriers. The math is straightforward: bundling works.

However, bundling only makes sense if the bundled rate is genuinely competitive. Get separate quotes first, then ask carriers what they’ll charge for a complete bundle. If one insurer’s bundled rate is significantly higher than competitors’ individual rates, walk away. Some small business owners also neglect to ask about specific discounts that stack on top of bundled pricing. Safety training discounts, paperless billing discounts, autopay discounts, and claims-free discounts often reduce premiums by another 5 to 15 percent.

Make Driver Safety Your Competitive Advantage

Implement a driver safety program-even a simple one with monthly safety meetings and clear vehicle maintenance standards-and you qualify for additional savings. Clean driving records for all your drivers matter enormously. A single at-fault accident or moving violation on an employee’s record can raise your premium by 10 to 30 percent, so make driver qualification standards part of your hiring process and monitor records annually. As an independent agency, we work with multiple top-rated insurance providers to identify which ones offer the best discounts for your specific safety practices and driver profiles. This approach helps small business owners access rates that reflect their actual risk, not just industry averages.

Your next step involves understanding what coverage options actually protect your fleet and which ones you can safely skip.

What Coverage Actually Protects Your Fleet

Liability Coverage: Your First Line of Defense

Liability coverage forms the foundation of commercial auto insurance, and it’s the only coverage most states legally require. This coverage pays for medical expenses and property damage when your driver causes an accident-it protects the other person, not your vehicle. State minimum liability limits vary widely. Some states require as little as $15,000 in bodily injury coverage per person, while others demand $50,000 or more. These minimums are dangerously low for small businesses. A single serious injury claim can exceed $100,000 in medical costs alone, and if your coverage limit is only $25,000, you personally owe the remaining $75,000. Courts can garnish your business income for years to satisfy a judgment.

Carry at least $100,000 per person and $300,000 per accident in bodily injury liability, plus $100,000 in property damage liability. These higher limits cost only slightly more than minimums but protect your business assets from catastrophic claims. If you operate multiple vehicles or employ drivers, the additional premium for adequate liability limits pays for itself through protection.

Collision and Comprehensive: Protecting Your Own Vehicles

Collision and comprehensive coverage protect your own vehicles, not third parties. Collision pays for repairs when your vehicle hits another car, object, or structure-regardless of fault. Comprehensive covers non-collision damage like theft, vandalism, weather, and animal strikes. Many small business owners skip comprehensive because they think their vehicles are low-risk, but this miscalculation often backfires. A food truck damaged by hail, a service van hit while parked, or equipment stolen from an unlocked vehicle represents lost revenue and repair costs you must absorb. The question isn’t whether damage will occur-it’s when.

Your deductible choice matters enormously for affordability. A $1,000 deductible costs significantly more than a $2,500 deductible, but only if you can actually afford to pay $2,500 out of pocket after an accident. Many small businesses choose deductibles they cannot afford, which defeats the purpose of having insurance.

Uninsured Motorist Coverage: Filling the Gap

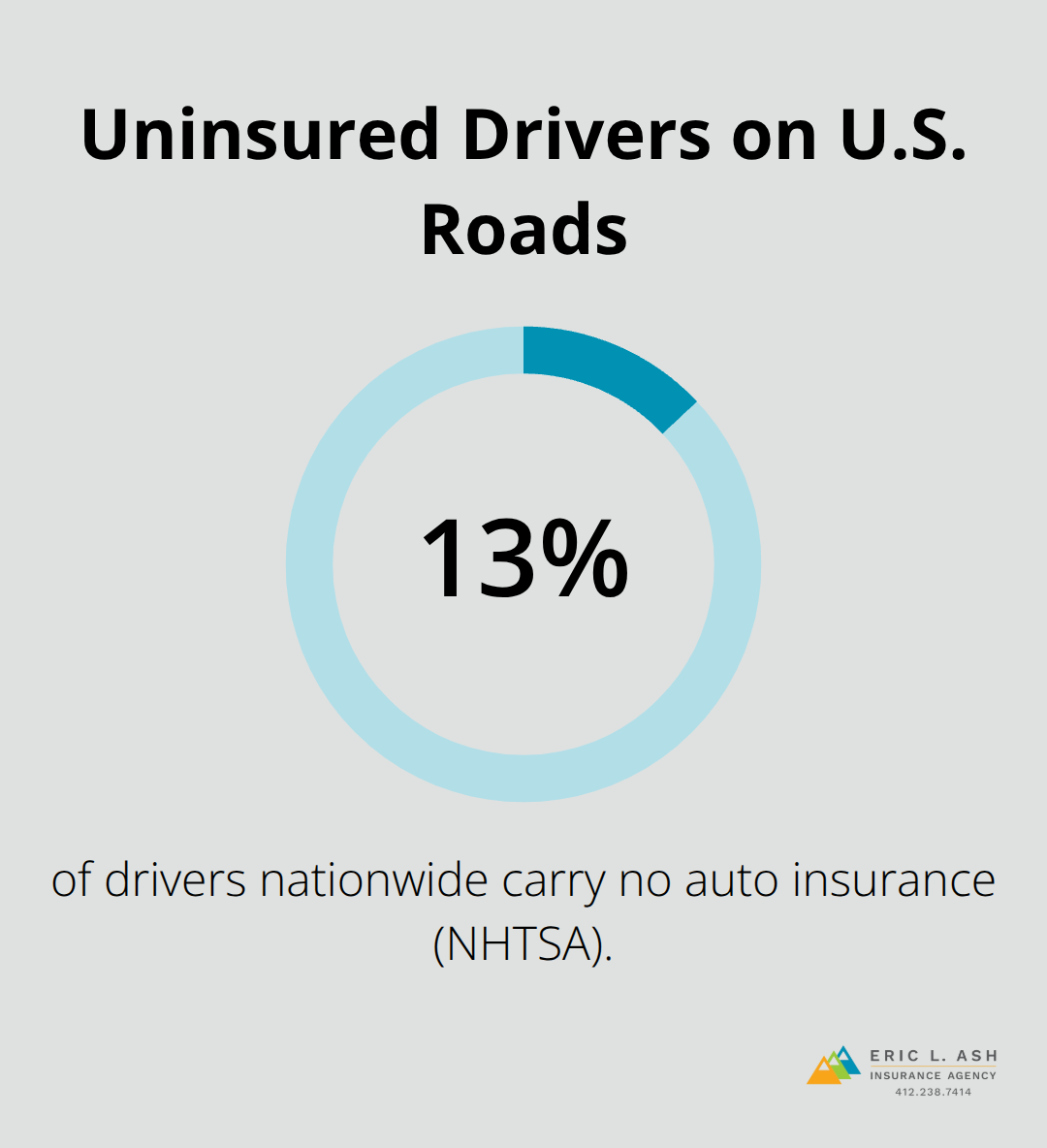

Uninsured motorist coverage protects you when another driver lacks adequate insurance or hits you and flees. According to the National Highway Traffic Safety Administration, roughly 13 percent of drivers nationwide carry no auto insurance, and in some states that number exceeds 20 percent. If an uninsured driver injures your employee or damages your vehicle, your uninsured motorist coverage steps in to cover medical expenses and repairs up to your policy limits.

This coverage is inexpensive-typically $50 to $150 annually depending on your limits-and it fills a critical gap that liability coverage cannot address. Skipping uninsured motorist protection is a false economy that leaves your fleet vulnerable to the growing number of uninsured drivers on the road.

Final Thoughts

Affordable small business commercial auto insurance requires three concrete actions: comparing multiple quotes, bundling policies strategically, and implementing driver safety practices that reduce your actual risk. Most small business owners overpay because they accept the first quote they receive or fail to ask about discounts that stack on top of bundled rates. The carriers you choose matter less than the effort you invest in shopping around and understanding your coverage needs.

Start by listing your vehicles and how you use them, then request quotes from at least three carriers with identical liability limits, deductibles, and coverage options. Ask each carrier what they’ll charge if you bundle commercial auto with general liability, property, or workers’ compensation, and track these numbers in a spreadsheet so you can see exactly where you save money. Once you’ve identified your lowest competitive rate, ask that carrier about safety training discounts, paperless billing discounts, and claims-free discounts that might apply to your business.

We at Eric L. Ash Insurance Agency work with multiple carriers to find competitive rates and tailored coverage for Pennsylvania small businesses. Contact us at ericlashagency.com to request a quote and compare your options for small business commercial auto protection.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.