Smart Guide to Short Term Rental Insurance for Pennsylvania Hosts

Running a short-term rental in Pennsylvania opens doors to steady income, but it also exposes you to risks that standard homeowners insurance won’t cover. Your regular policy explicitly excludes commercial activity like guest rentals, leaving you vulnerable to liability claims and property damage costs.

At Eric L. Ash Insurance Agency, we’ve seen hosts face unexpected gaps in coverage that cost them thousands. The right short-term rental insurance fills those gaps and protects both your property and your income stream.

What Your Short-Term Rental Insurance Actually Protects

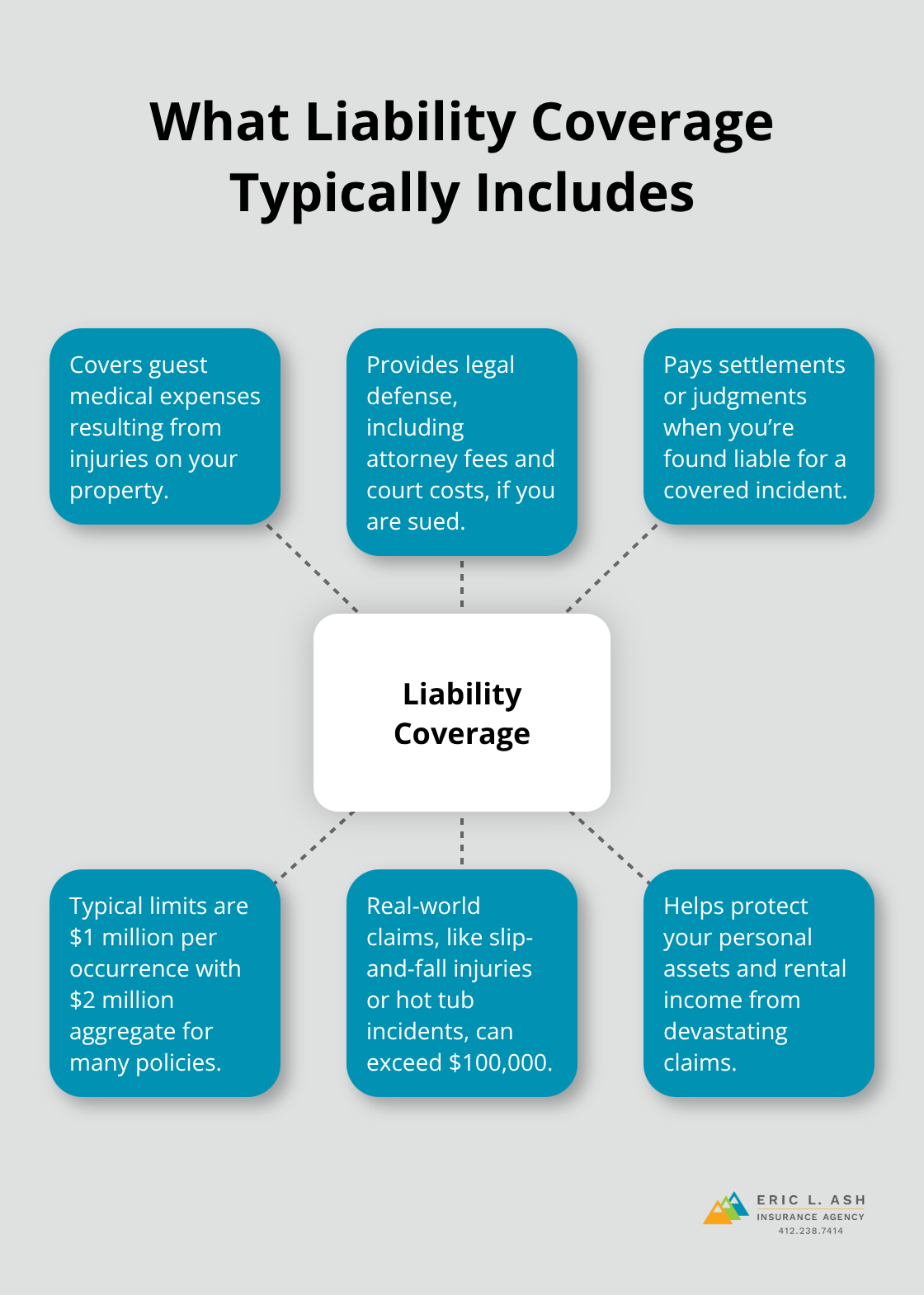

Liability Protection Shields You From Guest-Related Claims

Liability protection defends you when a guest suffers an injury on your property or causes damage to someone else’s belongings. Most policies offer $1 million in coverage per occurrence, with standard limits including $2 million aggregate, which matters because a single slip-and-fall claim or a guest’s visitor injured in your hot tub can easily exceed $100,000 in medical costs and legal fees. This coverage pays for medical expenses, legal defense, and settlement costs that would otherwise come directly from your pocket.

Without it, you face personal financial exposure that can devastate your rental income and personal assets.

Property Damage Coverage Protects Your Physical Investment

Property damage and loss coverage reimburses you for damage to your furnishings, appliances, and structural elements caused by covered perils like water damage from burst pipes, fire, storms, and vandalism. Water damage from broken pipes and appliance leaks represents the most expensive type of property damage for rental properties, so this coverage directly protects your largest investment. The valuation method matters significantly-replacement cost value policies pay what repairs actually cost, while actual cash value policies deduct depreciation and leave you short. You should always select replacement cost value coverage to avoid substantial out-of-pocket expenses when damage occurs.

Loss of Rent Coverage Maintains Your Cash Flow

Additional living expenses coverage, sometimes called loss of rent, reimburses you for lost rental income when a covered claim makes your property uninhabitable. If a fire forces you to close for three months, this coverage pays the income you would have earned during that period, protecting your cash flow when you need it most. Loss of rent coverage typically pays actual rental income lost with no time limit up to your chosen amount, which differs from homeowners policies that cover temporary living expenses only. This distinction proves critical for hosts who depend on rental income to cover mortgage payments or property expenses.

Tailoring Coverage to Match Your Property’s Needs

A $1 million liability limit protects you adequately for most Pennsylvania properties, though larger homes with pools or hot tubs warrant higher limits. Steadily and other Pennsylvania insurers offer these coverages for rental periods as short as one night, and policies can be tailored to include specific risks or limited coverages based on your property’s needs and your budget. The key is verifying that your chosen policy covers the specific exposures your rental creates, because gaps in coverage leave you personally liable for costs that specialized insurance would otherwise handle. An independent agent can help you assess which coverage options match your property type and guest volume.

Why Standard Homeowners Policies Exclude Rental Activity

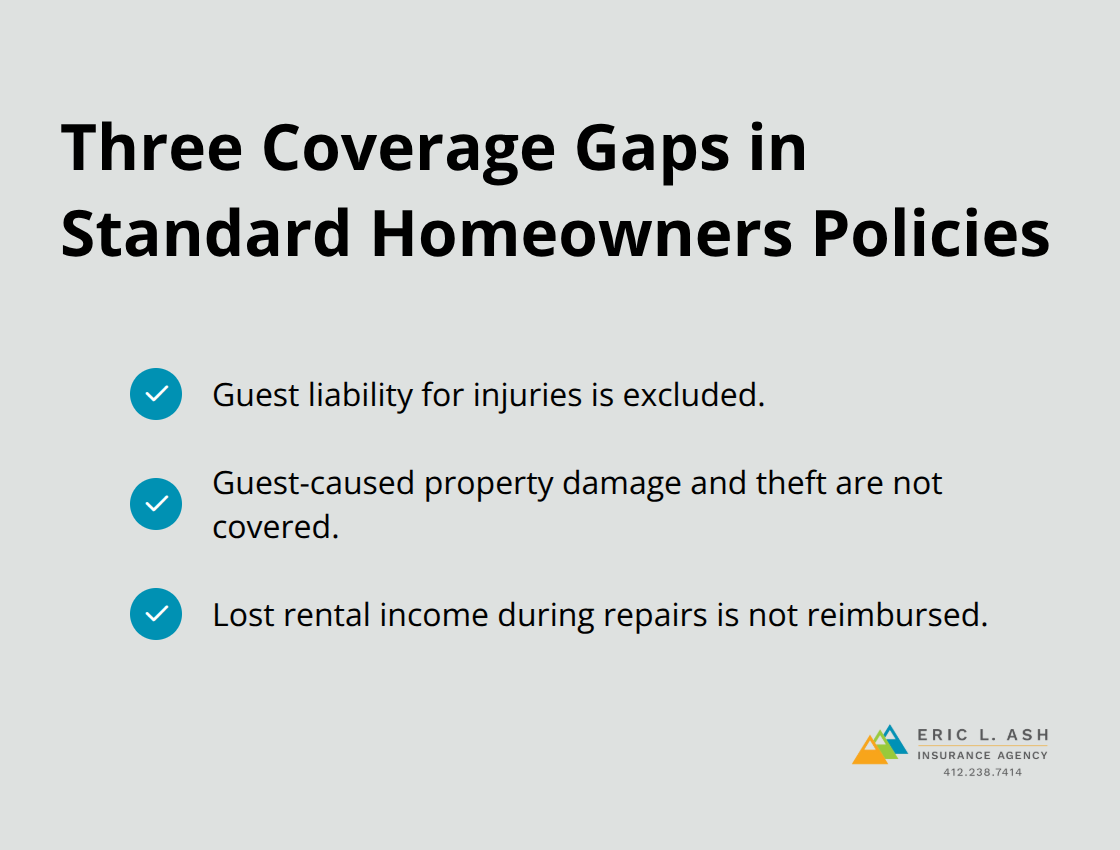

Your homeowners insurance policy contains explicit language that excludes rental activity, and this exclusion exists for a fundamental reason: your insurer priced that policy assuming your home remains your primary residence. When you start accepting guests and collecting rental income, you fundamentally change the risk profile of the property in ways your standard homeowners policy was never designed to handle. Homeowners insurance is designed for owner-occupied properties, not for business use. This means filing a claim related to your rental operation can result in a denial, and some insurers may even cancel your policy once they discover you operate a short-term rental. The financial exposure here is real and immediate-you lose coverage precisely when you need it most.

Guest Liability Falls Outside Standard Coverage

Guest liability represents a specific blind spot in standard homeowners policies. Your regular policy covers you if a family member’s friend slips on your stairs, but it explicitly excludes injuries to paying guests and their visitors. A guest who sustains a serious injury in your rental can pursue a claim against you personally, and without proper coverage, you become personally liable for medical bills, lost wages, and pain-and-suffering damages. Standard homeowners policies also ignore the unique exposures that come with short-term rentals-damage caused by guests who treat your property differently than long-term tenants would, theft of your furnishings and amenities, or property damage from parties and gatherings.

Lost Rental Income Receives Zero Protection

Your homeowners policy provides loss of use coverage for your own temporary housing needs if your home becomes uninhabitable, but it provides zero protection for lost rental income. If a fire makes your property unrentable for two months, your homeowners policy covers your hotel costs while you find alternative housing, but it won’t reimburse the thousands in rental income you forfeit. This gap forces you to absorb that income loss entirely from your own pocket, even though the loss resulted from a covered peril.

Specialized Insurance Closes the Coverage Gaps

Specialized short-term rental insurance closes all three gaps-it extends liability protection to guests, covers guest-related property damage and your furnishings, and replaces lost rental income when covered claims force a shutdown. Understanding these gaps helps you recognize why your current homeowners policy leaves you vulnerable, and it points directly to the solution: coverage specifically designed for the risks that short-term rental hosts actually face.

The next step involves selecting the right policy for your Pennsylvania property, which requires assessing your specific situation and comparing what different carriers offer.

Selecting the Right Coverage for Your Pennsylvania Rental

Calculate Your Property’s True Replacement Cost

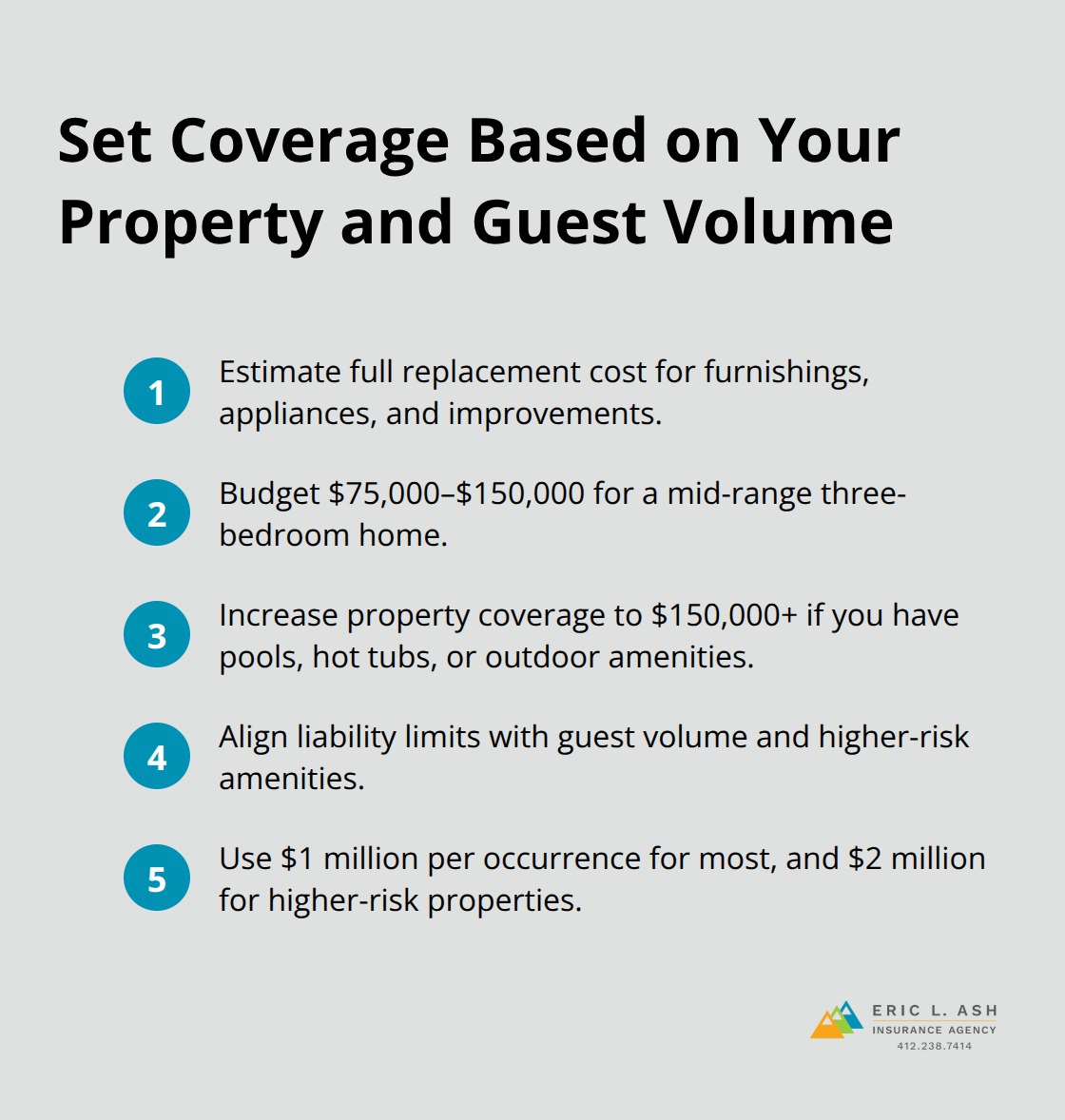

Matching coverage limits to your actual property risk starts with calculating what it would cost to fully replace your furnishings, appliances, and structural improvements if a total loss occurred. A three-bedroom home in the Poconos with mid-range furnishings typically requires $75,000 to $150,000 in property coverage, while a fully equipped property with outdoor amenities like hot tubs or pools warrants $150,000 or higher. Your guest volume matters equally-properties hosting 30 guests monthly face different liability exposures than those hosting 5 guests monthly, and your coverage limits should reflect this frequency.

For liability, the industry standard of $1 million per occurrence works for most Pennsylvania rentals, but properties with pools, hot tubs, or accommodations for large groups should carry $2 million.

Set Deductibles and Loss of Rent Coverage to Match Your Financial Situation

Deductibles represent your out-of-pocket responsibility when claims occur, and selecting a $1,000 deductible saves roughly 15–20% on premiums compared to a $500 deductible, though this only makes sense if you can absorb that cost without financial strain. Loss of rent coverage should equal your average monthly rental income multiplied by the number of months you reasonably estimate your property could remain uninhabitable-if you earn $4,000 monthly and want protection for three months of closure, you need $12,000 in loss of rent coverage minimum. This calculation protects your income stream when covered events force temporary shutdowns.

Compare Quotes From Multiple Carriers With Identical Coverage Specifications

Steadily, Proper Insurance, and Erie Insurance each offer different coverage combinations and price points across Pennsylvania, so comparing quotes from multiple carriers reveals meaningful differences in both cost and what’s actually covered. Request quotes with identical coverage limits and deductibles from at least three carriers, then examine what each policy actually covers beyond the base liability and property protection-some policies include amenities coverage for bikes or kayaks while others exclude them, some cover bed bug and flea liability while others don’t, and some include squatters protection if a guest refuses to leave. Water damage from broken pipes and appliance leaks represents the most expensive property damage claim type for rental properties, so verify that your policy covers both and doesn’t impose limitations on coverage during vacancy periods. Ask each carrier whether your policy covers guest personal property damage, because a guest who damages their own laptop or camera during their stay shouldn’t create liability for you, yet some policies create confusion on this point.

Understand Premium Variation Across Pennsylvania Regions

Premium costs vary substantially-a basic policy might run $600–$800 annually while comprehensive coverage with higher limits can reach $1,500–$2,500 depending on your property location, size, and guest volume. Pennsylvania regions like Philadelphia and Pittsburgh often command higher premiums than rural areas due to higher replacement costs and claim frequency, though this varies by specific neighborhood. An independent insurance agency can obtain quotes from dozens of carriers simultaneously, saving you hours of individual research and revealing options you wouldn’t find by shopping directly with insurers online.

Review Policy Documents and Identify Coverage Gaps

Before binding any policy, read the actual policy document rather than relying on marketing summaries, because exclusions buried in the fine print can eliminate coverage you thought you had. Ask your agent which perils aren’t covered-most policies exclude flood, earthquake, and acts of war, and if your property sits in a flood zone or faces other specific risks, you’ll need separate riders or policies to address those gaps.

Final Thoughts

Standard homeowners insurance leaves Pennsylvania short-term rental hosts exposed to three critical gaps: guest liability claims, property damage from rental activity, and lost income when your property becomes uninhabitable. These gaps exist because your homeowners policy was priced for owner-occupied homes, not income-generating rental operations. A single guest injury or fire that forces a three-month closure can cost you tens of thousands in medical claims, legal fees, and lost rental income that your standard policy won’t cover.

Specialized short-term rental insurance solves these gaps directly by extending liability protection to guests and their visitors, covering property damage caused by rental activity, and reimbursing lost rental income when covered claims force temporary shutdowns. The right policy matches your property’s replacement cost, reflects your guest volume, and includes coverage for the specific exposures your rental creates-whether that’s amenities like hot tubs or the risk of guest damage to your furnishings. You need to calculate your property’s true replacement cost and set liability limits that reflect your guest volume and amenities.

We at Eric L. Ash Insurance Agency work with dozens of carriers to shop multiple markets and deliver competitive rates tailored to your specific rental situation. As a veteran-owned, independent agency serving Pennsylvania, we specialize in short-term rental insurance and can help you assess your property’s actual risk profile and find coverage that protects both your investment and your income stream. Contact us today to compare quotes and close the coverage gaps that leave you vulnerable.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.