Vacation Rental Landlord Insurance Essentials for Property Owners

Owning a vacation rental can be profitable, but it exposes you to risks that standard homeowners insurance simply doesn’t cover. Guest injuries, property damage, and lost income from cancellations are real threats that require specialized protection.

At Eric L. Ash Insurance Agency, we’ve seen too many property owners learn this lesson the hard way. This guide walks you through vacation rental landlord insurance essentials so you can protect your investment properly.

What Vacation Rental Insurance Actually Protects

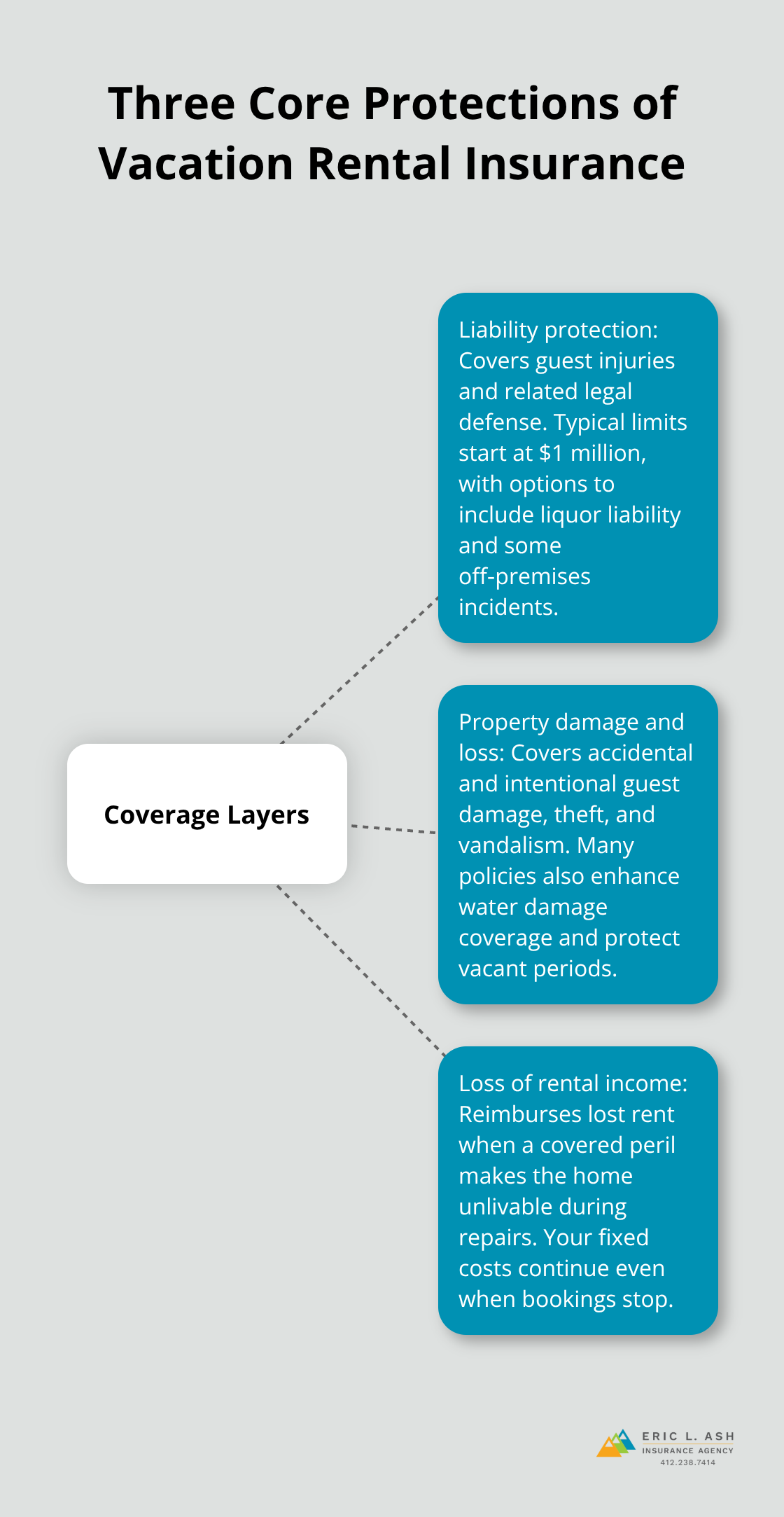

Vacation rental insurance covers three critical areas that standard homeowners policies explicitly exclude. The first is liability protection when a guest gets injured on your property. If someone slips on your deck, gets food poisoning, or claims you caused them harm, a guest injury claim can result in significant legal defense costs and settlements. Vacation rental liability coverage typically starts at $1 million in commercial general liability limits, though you should verify this protects off-premises situations and includes liquor liability if you provide alcohol to guests. The second protection is property damage and loss coverage for your building, systems, and furnishings. Water damage from a guest’s negligence can cost $20,000 to $50,000 if it affects multiple floors, according to industry data. Your policy should cover accidental damage by guests, intentional damage by guests, theft, and vandalism without artificial caps on payouts. Many policies also include enhanced water damage coverage and protection during vacancy periods, which matters if you need to close temporarily for repairs.

The third layer is loss of rental income protection. If a covered peril like fire or severe water damage makes your property unlivable, this coverage reimburses you for the rental income you would have earned during the repair period. This matters tremendously because your mortgage, property taxes, and maintenance costs don’t pause while you’re fixing storm damage.

Guest Liability Needs Real Limits

Your liability limits should match your asset value and guest volume. If you host multiple guests weekly across a four-bedroom home, $1 million feels safer than $300,000. Consider adding umbrella insurance on top of your base policy to extend liability protection and cover squatter-related eviction costs or bed bug infestations, which standard coverage often excludes.

Property Coverage Must Be Replacement Value, Not Actual Cash Value

Replacement value policies pay what it costs to rebuild or replace items today, not what you paid five years ago. Actual cash value subtracts depreciation, leaving you short when you file a claim. Ask your agent explicitly whether your policy covers intentional guest damage, per-claim dollar limits on specific items, and whether limits exist on how often you can rent per year.

Loss of Income Timing Matters

Loss of rent coverage typically begins after a waiting period (often 14 to 30 days after the covered loss occurs). Some policies cap the payout period at 12 months. Confirm these terms with your carrier so you understand how long you’re protected and whether the daily limit matches your actual nightly rate. Standalone vacation rental policies tend to offer broader terms than endorsements added to homeowners policies, especially if you rent year-round.

The specifics of what your policy covers directly affect how well you can recover from a guest-related incident. Next, you’ll need to understand why your current homeowners insurance won’t cut it-and what gaps you’re actually facing.

Why Your Homeowners Policy Won’t Cover Your Vacation Rental

Standard homeowners insurance explicitly excludes rental activity, and most carriers will deny your claim or cancel your policy if they discover you host paying guests. Your homeowners insurer views vacation rental operations as a commercial business, not residential occupancy. When you sign a homeowners policy, you affirm that you occupy the property as your primary residence or occasional personal-use property. The moment you list your home on Airbnb or Vrbo, that contract breaks.

What Happens When You File a Claim Without Disclosure

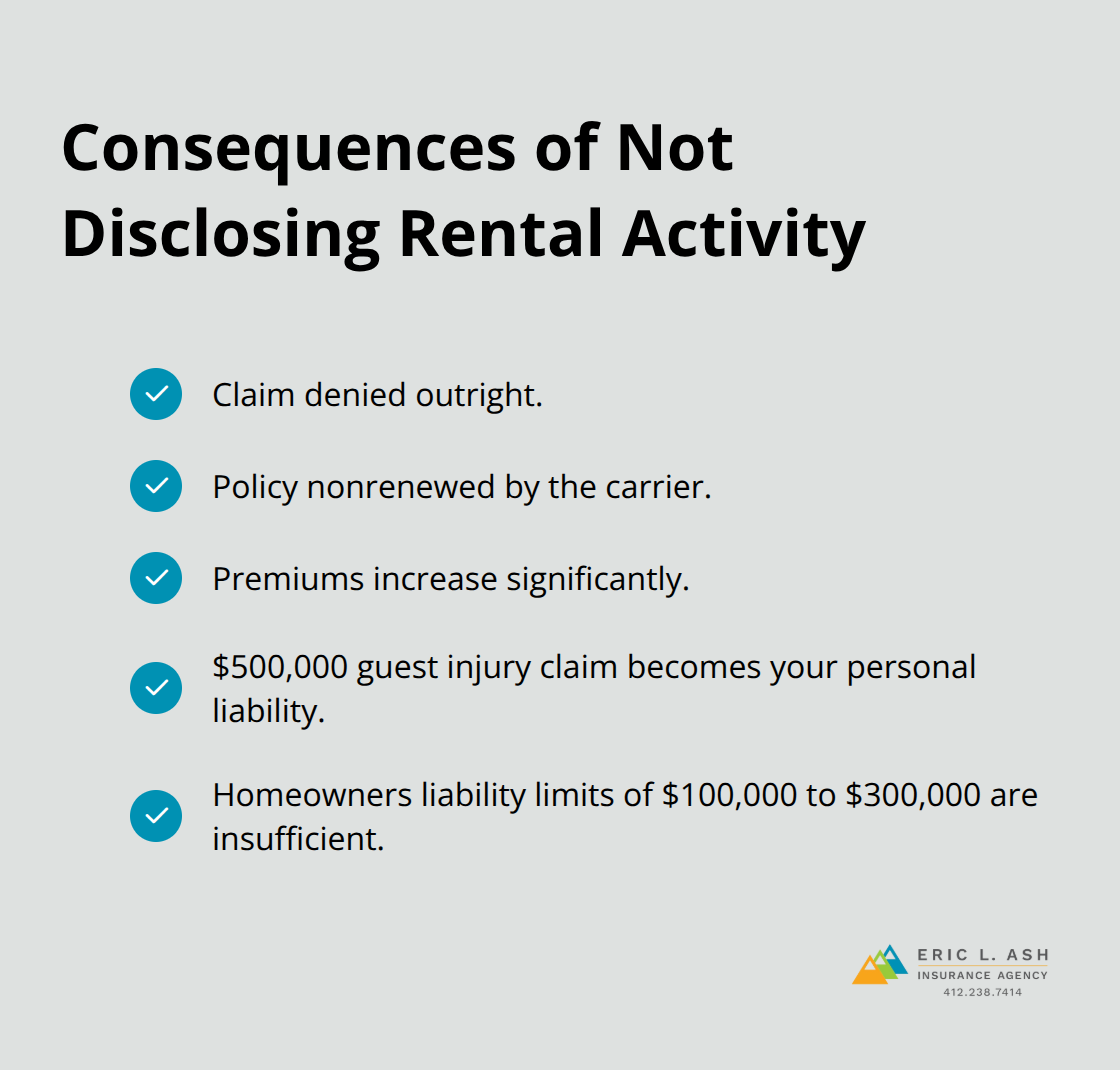

If you file a claim without disclosing rental activity, the insurer can deny coverage entirely, refuse to renew your policy, or raise your premiums significantly when they discover the truth. This isn’t a gray area-policy exclusions make it explicit. A guest injury claim that would cost $500,000 to defend and settle becomes your personal liability if your homeowners policy has excluded business operations.

The liability limits on a homeowners policy (typically $100,000 to $300,000) won’t protect you against a serious guest injury lawsuit. Commercial general liability coverage for vacation rentals starts at $1 million, and that’s the minimum we recommend for any property that hosts multiple guests annually.

The Coverage Gaps That Matter Most

Your homeowners policy also doesn’t cover intentional or malicious damage by guests, theft of furnishings, or loss of rental income when the property becomes uninhabitable. Water damage from a guest’s negligence, fire from a guest’s cooking accident, or vandalism during a party all fall outside standard homeowners coverage because they tie to rental operations, not personal residence use. The coverage gaps widen further when you factor in vacancy periods, property entrustment (guest damage to your belongings), and bed bug infestations-all common vacation rental risks that homeowners policies either exclude or cap at unrealistic limits.

Endorsements vs. Standalone Policies: The Cost and Coverage Trade-Off

If you operate a short-term rental property without proper vacation rental insurance and experience a significant loss, you’ll discover that your homeowners premium provides zero protection. Standalone vacation rental policies or home sharing endorsements close these gaps by explicitly covering guest-caused damage, liability arising from paying guests, and loss of income during repairs. The cost difference is real-standalone STR insurance typically runs $600 to $1,500 annually depending on property value and occupancy, but that investment protects your entire business model. Endorsements added to homeowners policies cost $200 to $600 per year and work for properties rented fewer than 180 days annually, though they still offer narrower liability limits and more exclusions than standalone policies.

When Standalone Coverage Becomes Non-Negotiable

If you rent your property year-round or operate multiple units, a standalone vacation rental policy is the only option that won’t leave you exposed. The distinction matters because your mortgage lender also expects appropriate coverage, and an undisclosed rental operation can trigger a policy violation that affects your ability to refinance or sell the property later. Your lender won’t accept a homeowners policy as proof of coverage for a rental property-they’ll require documentation that your insurance specifically addresses the commercial nature of your operation.

Understanding these gaps sets you up to make an informed decision about which type of coverage actually fits your rental model and risk profile.

How to Choose the Right Vacation Rental Insurance Policy

Choosing vacation rental insurance requires matching your coverage to three concrete factors: your property’s physical characteristics, how often guests occupy it, and what assets you need to protect. Start by documenting your property type, number of bedrooms, square footage, and replacement cost. A 2,000-square-foot three-bedroom home in Pennsylvania costs significantly more to rebuild than a one-bedroom condo, and your coverage limits must reflect that reality. Next, calculate your actual guest volume over a 12-month period.

Assess Your Property Type and Guest Volume

If you rent fewer than 180 days annually, a home sharing endorsement on your existing homeowners policy might work and will cost $200 to $600 per year. If you rent 180 days or more, or operate year-round, standalone vacation rental insurance is mandatory because endorsements cap occupancy and often exclude intentional guest damage or bed bug coverage that standalone policies include. The 180-day threshold isn’t arbitrary-it marks the point where rental activity shifts from occasional to primary business operation, and your insurance must reflect that distinction.

Calculate your expected annual rental income and compare that number against potential loss scenarios. If you generate $40,000 in annual rental revenue but your property sits vacant for 60 days during repairs after a water damage claim, loss of income coverage becomes essential, not optional. Your policy should reimburse lost rental income for at least 12 months following a covered loss.

Compare Liability Limits and Deductibles

Standard commercial general liability starts at $1 million, which protects you against guest injury claims up to that amount. If you host large parties or serve alcohol, request explicit confirmation that your policy includes liquor liability coverage, which many basic policies exclude. Property damage deductibles typically range from $500 to $2,500 per claim, and higher deductibles lower your premium but increase your out-of-pocket costs when damage occurs.

Choose your deductible based on your financial position. If you can absorb a $2,500 claim without stress, that deductible saves you money annually. If a $1,000 claim would strain your cash flow, stick with a $500 deductible even if premiums cost slightly more. Replacement value coverage is non-negotiable; actual cash value policies depreciate your belongings and leave you underfunded when you file claims. Request replacement cost explicitly in writing from your agent.

Evaluate Additional Endorsements and Add-Ons

Additional endorsements and riders close specific gaps in your base policy. Bed bug coverage costs $50 to $150 annually and protects against infestation claims, which standard policies exclude. Squatter protection covers eviction-related legal fees and lost rent if an unauthorized occupant claims tenancy rights. High-value item riders protect furnishings, appliances, or art worth more than standard per-item limits.

Professional cleaning staff liability covers injuries or property damage caused by your hired cleaners. Evaluate which riders match your actual operational risks-if you never hire outside cleaning crews, that rider wastes money, but if you employ housekeeping staff, it’s essential. The cost of these add-ons (typically $50 to $300 annually per rider) should align with the specific risks your rental operation faces.

Final Thoughts

Vacation rental landlord insurance protects your investment where homeowners policies leave you exposed. A single guest injury or water damage claim can cost tens of thousands of dollars out of your pocket if you carry the wrong coverage type. The gaps between standard homeowner protection and what your rental operation actually needs are too large to ignore.

Calculate your annual rental days and property replacement cost, then contact an insurance agent who specializes in vacation rental coverage. Ask specifically about commercial general liability limits, replacement value coverage, loss of income protection, and which endorsements match your operational risks. Request quotes from multiple carriers so you can compare liability limits, deductibles, and annual premiums side by side.

We at Eric L. Ash Insurance Agency work with property owners across Pennsylvania who operate vacation rentals on platforms like Airbnb and Vrbo. Our team understands the specific risks vacation rental owners face and can help you avoid the gaps that leave owners exposed. Contact Eric L. Ash Insurance Agency to get proper coverage in place with a consultation and quote tailored to your property and guest volume.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.