Short Term Landlord Insurance: Protecting Holiday Rentals

Holiday rental properties operate differently than traditional homes, which means standard insurance won’t cut it. We at Eric L. Ash Insurance Agency see firsthand how short-term landlord insurance fills critical gaps that leave owners vulnerable.

Guest turnover, liability exposure, and income loss are real risks that standard homeowners policies simply don’t cover. The right protection keeps your investment safe.

Why Your Holiday Rental Faces Risks Standard Insurance Won’t Cover

Standard Policies Don’t Account for Short-Term Rental Operations

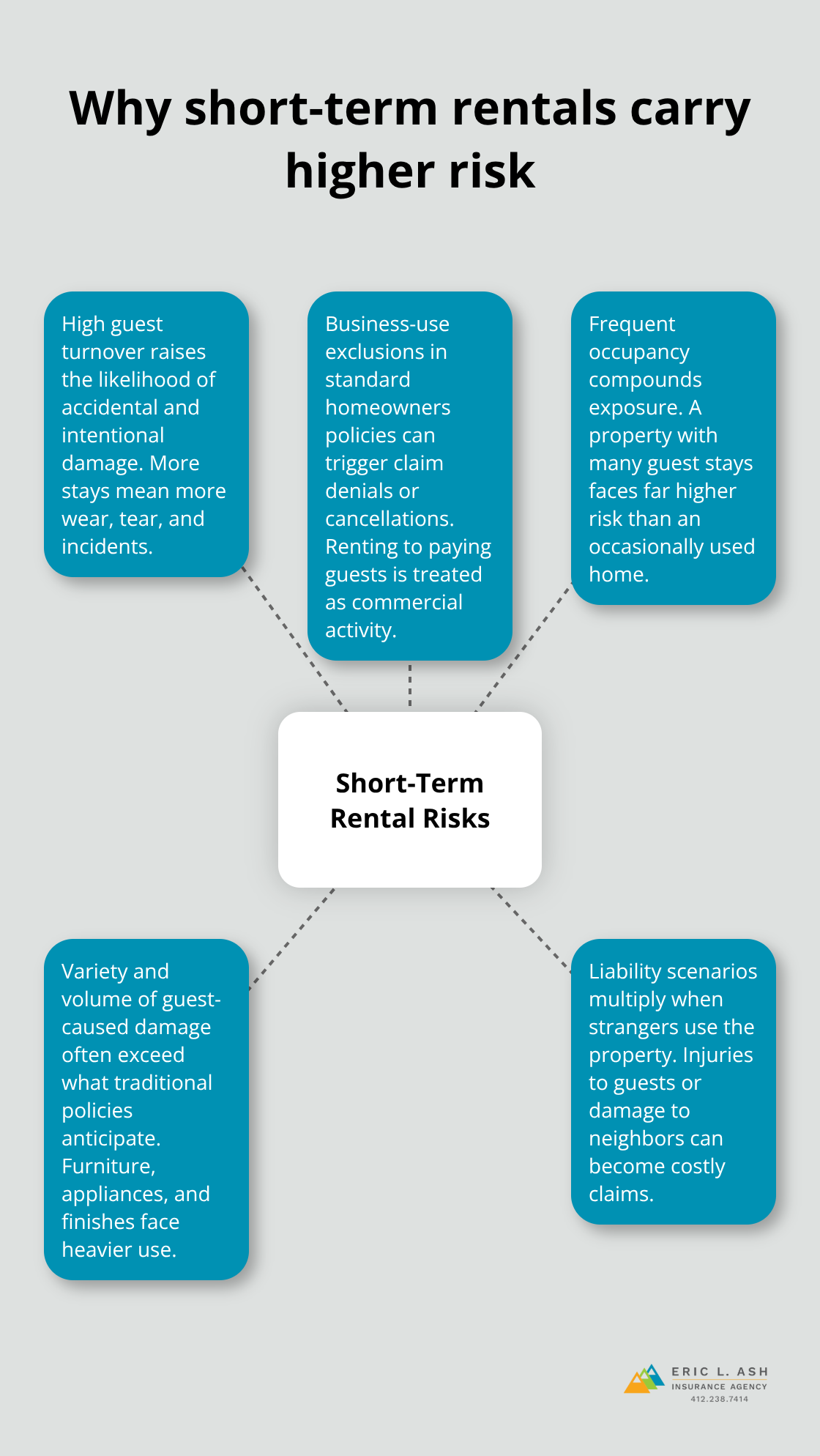

Short-term rental properties operate in a fundamentally different risk environment than owner-occupied homes, and standard homeowners policies were never designed to handle this reality. When guests rotate through your property every few days or weeks, the exposure to property damage increases dramatically. A guest-caused hole in drywall, broken furniture, or damaged appliances happens far more often in a short-term rental than in a traditional home.

Standard homeowners policies explicitly exclude active business use, meaning short-term rental activity is treated as a commercial operation and can lead to claim denial or policy cancellation without proper coverage. The frequency of occupancy matters enormously-a property with 50 guest stays per year faces exponentially higher risk than a home with two family vacations annually.

Guest-Caused Damage Overwhelms Traditional Coverage

Property owners who rent their homes to paying guests quickly discover that standard policies leave them exposed. Short-term rental property damage claims fall outside what traditional homeowners insurance covers. Standard policies simply don’t account for the volume and variety of damage that paying guests inflict on a property.

We at Eric L. Ash Insurance Agency work with property owners across Pennsylvania who’ve learned this lesson after a claim was denied because their policy didn’t cover paying guests. The financial impact of even a few denied claims can exceed what owners would have paid for proper short-term rental coverage.

Liability Exposure Multiplies with Commercial Activity

Liability exposure with short-term rentals operates on a different scale than traditional homeownership. A guest injured on your property, a visitor to a guest who slips on the deck, or damage caused by your guests to a neighbor’s property all create liability scenarios that standard policies either exclude or severely limit. When someone pays to stay at your property, insurers view the relationship as commercial, which changes their willingness to defend claims.

Income Loss Creates a Hidden Financial Gap

Loss of rental income presents a third major gap that most property owners overlook. If a covered event like a fire or hurricane makes your property uninhabitable, standard homeowners insurance won’t replace the income you would have earned from guest bookings during the repair period. For properties generating significant monthly rental revenue, this gap can mean thousands in uncompensated losses while contractors rebuild your home.

Short-term landlord insurance addresses these three exposures directly: it covers guest-caused property damage, provides liability protection for the rental activity itself, and includes loss-of-income coverage to protect your cash flow when a covered event interrupts bookings. Understanding what these policies actually cover helps you determine whether your current protection is sufficient.

What Short-Term Landlord Insurance Actually Covers

Guest-Caused Property Damage Coverage

Short-term landlord insurance fills three distinct coverage gaps that standard homeowners policies leave wide open, and understanding exactly what you’re buying matters far more than chasing the lowest premium. Property damage coverage protects against guest-caused destruction, whether intentional or negligent, covering everything from broken windows and damaged furniture to holes punched in walls and spilled liquids on flooring. Unlike standard policies that treat paying guests as a reason to deny claims, short-term rental policies explicitly include guest-caused damage, with replacement-cost valuation paying to replace items at current market prices rather than depreciated values.

Liability Protection for Rental Operations

Liability coverage under these policies typically starts at $1 million and protects you when a guest suffers an injury at your property or when your guests damage a neighbor’s home. This coverage extends to situations standard homeowners policies would exclude, such as a guest who falls in the shower and sues, or a guest’s child who damages the fence next door. The liability component addresses the commercial nature of your rental operation, which standard policies simply refuse to cover.

Loss-of-Income and Additional Protections

Loss-of-income protection reimburses you for rental revenue lost when a covered event like fire, storm, or burst pipes makes the property uninhabitable during repairs, directly addressing the cash-flow crisis that property owners face when bookings must be canceled. Many short-term rental policies also include amenities liability coverage for pools, hot tubs, bikes, and kayaks, which standard policies often exclude or underrate. Bed bug and flea protection has become increasingly standard, covering extermination costs and lost revenue from canceled bookings.

Understanding Premium Costs and Deductible Options

For an average-sized Florida home, annual short-term rental insurance typically costs about $2,000 to $3,000, though premiums vary significantly based on occupancy rate, guest turnover patterns, seasonal booking spikes, and whether your property includes high-risk amenities. Higher-value properties or those with extensive amenities cost substantially more. Deductible selection dramatically affects both premium and out-of-pocket exposure: a $1,000 deductible reduces your annual cost but means paying $1,000 for every claim, while a $2,500 to $5,000 deductible lowers premiums but requires maintaining cash reserves for emergencies.

Tailoring Coverage to Your Specific Operation

The real protection comes from policies that accommodate your specific operation, which means documenting your occupancy rate, guest turnover frequency, seasonal patterns, and offered amenities before shopping for coverage. Obtaining quotes from at least three insurers and requesting written details on coverage limits, deductibles, and exclusions prevents vague marketing summaries from obscuring what you actually purchase. Comparing deductibles and identifying coverage gaps by reading actual policy sections-ensuring guest-damage covers intentional and negligent acts, verifying amenity coverage, and confirming loss-of-income protection during vacancies-separates adequate protection from inadequate policies. Requesting a sample policy document (not just a quote) allows you to review actual terms, exclusions, and conditions before committing to any carrier.

How to Choose the Right Short-Term Rental Coverage

Document Your Property’s Specific Operation

Start your search by documenting exactly how your property operates. Occupancy rate, guest turnover frequency, seasonal patterns, and specific amenities drive both coverage needs and premium costs, so vague estimates waste time and money. A property renting 40 weeks annually with five-day average stays faces different risks than a property renting 20 weeks with two-week stays. Properties with pools, hot tubs, or bikes need explicit amenities liability coverage, since standard short-term rental policies often exclude or underrate these exposures.

Obtain Written Quotes from Multiple Carriers

Once you understand your operation, obtain written quotes from at least three carriers and require detailed breakdowns of coverage limits, deductibles, and exclusions rather than accepting vague marketing summaries. Request actual sample policy documents, not just quote summaries, so you can read the real terms before committing. Many property owners skip this step and later discover coverage gaps that cost thousands when claims arise.

Compare Liability Limits and Deductible Options

Liability coverage typically starts at $1 million but varies substantially across carriers. Some offer $2 million or higher limits, which matters if your property attracts high-traffic guest volume or sits in densely populated areas near downtown locations where liability exposure runs higher. Deductible selection directly affects both your annual premium and out-of-pocket costs for each claim. A $1,000 deductible reduces annual premiums but means paying $1,000 for every guest-damage claim, while a $2,500 to $5,000 deductible lowers premiums but requires maintaining cash reserves for emergency repairs.

The math differs for each property: high-occupancy rentals with frequent small claims benefit from lower deductibles, while seasonal properties with fewer bookings might accept higher deductibles to cut annual costs. Property damage coverage should use replacement-cost valuation, paying current market prices rather than depreciated values, and guest-caused damage coverage must explicitly include both intentional and negligent acts.

Identify Coverage Gaps Before You Commit

Read the actual policy language for loss-of-income coverage, verifying it protects revenue during vacant periods and covers repairs after covered events. Florida properties face hurricane season income risk, making loss-of-income protection genuinely important rather than optional. Bed bug and flea protection has become standard in most short-term rental policies, typically covering extermination costs and lost revenue from canceled bookings, so confirm this protection exists in your quotes.

Amenities liability deserves specific attention: pools, hot tubs, bikes, and kayaks create distinct liability exposures that many standard policies exclude entirely. An independent agency with access to multiple A-rated carriers can tailor coverage to your specific rental model more effectively than online quote tools that force properties into standardized categories. We at Eric L. Ash Insurance Agency leverage relationships with dozens of carriers to shop multiple markets and help property owners across Pennsylvania compare actual policy terms and identify which carriers best match their operation, rather than settling for the lowest premium on an inadequate policy.

Final Thoughts

Short-term landlord insurance protects your investment in ways standard homeowners policies simply cannot. The gaps are real, the financial consequences are substantial, and waiting until after a claim denial to address coverage leaves you exposed to losses that proper insurance would have prevented. Property owners who operate holiday rentals without dedicated short-term landlord insurance are gambling with their income and their property, betting that guest damage, liability claims, and income interruptions won’t happen to them.

Standard policies exclude paying guests by design because insurers built homeowners coverage around owner-occupied residences, not commercial rental operations. When you rent your property to strangers for short stays, you fundamentally change the risk profile, and your insurance needs to reflect that reality. The difference between adequate protection and inadequate coverage often comes down to whether you took time to read actual policy documents and compare what carriers actually offer rather than accepting the first quote that arrived in your inbox.

We at Eric L. Ash Insurance Agency shop multiple markets across Pennsylvania to find carriers that understand short-term rental operations and offer coverage tailored to your specific property, occupancy patterns, and amenities. Start by documenting your operation, obtain written quotes from multiple carriers, and request actual policy documents so you can read the terms yourself. Contact us to discuss your specific rental operation and explore coverage options that protect both your property and your income stream.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.